Lira Focus

The lira has been on a relentless downward path in 2025, shedding almost 15% since the start of the year. With US rates still dominating global flows, can Turkey’s improving fundamentals and easing inflation narrative stabilise USDTRY in the months ahead?

Restoring Stability

The lira’s long decline has been shaped by a mix of structural weaknesses and shifting global cycles, but the landscape now looks much calmer than the turmoil of the spring. The arrest of Istanbul Mayor Ekrem İmamoğlu in March sparked sharp volatility, forcing emergency policy tightening and a rapid depletion of reserves. Since then, however, financial indicators have largely normalised: gross reserves have been rebuilt, the BIST 100 equity index has recovered its losses, and investor sentiment has steadied as policymakers moved decisively to restore confidence. By mid-August, the currency still faces downward pressure, yet the environment is considerably more constructive for investors than just a few months ago.

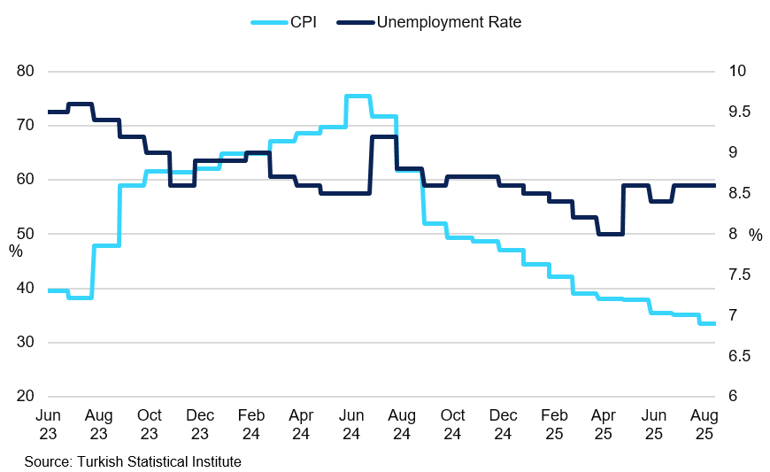

One of the developments supporting stability has been the steady fall in inflation. After peaking near 75% in mid-2024, annual consumer price growth slowed to 33.52% in July 2025, with forecasts pointing to a further decline toward 24% by the end of the year. The central bank’s projection range stands at 19–29%, broadly in line with survey medians. For an economy repeatedly challenged by inflationary surges, the recent slowdown provides relief for households and businesses and lowers immediate pressures on financial stability.

Turkey Inflation and Unemployment

Turkey's CPI has dropped to mid-30s.

With inflation easing, the central bank has resumed its easing cycle. After raising rates aggressively in March to stabilise markets, policymakers cut the benchmark policy rate by 300bps to 43% in July, surprising observers who had expected a more cautious move. Further reductions are anticipated in the coming months, with market consensus pointing to around 36% by year-end. The trajectory reflects confidence that disinflation will continue, but it also raises the question of whether real rates will remain sufficient to anchor expectations and provide support for the lira. Turkey has often struggled to strike the right balance between growth and stability, and investors will be alert to any signs that renewed monetary loosening risks reigniting inflation or straining external financing conditions.

One reason the lira’s near-term outlook looks more stable is the improvement in external balances. Turkey’s current account deficit is projected at just 1.5% of GDP this year, a far more manageable level than the large gaps that frequently left the economy vulnerable to external shocks in the past. A moderate deficit implies limited external financing needs, reducing reliance on volatile capital inflows and lowering the risk of sudden stop crises. This progress has been reflected in sovereign risk pricing: five-year credit default swaps, a barometer of investor concern over Turkey’s ability to meet its obligations, have retreated steadily after spiking during the March turmoil. At around 265bps in mid-August, CDS spreads remain well below past peaks, signalling that investors now view Turkey as much less fragile.

ade Pressures and Growth Trends

The trade environment presents both obstacles and openings for Turkey. On 7 August, the US lifted its baseline tariff on Turkish goods from 10% to 15%, while separate levies remain in place, including a 25% tariff on imported cars and auto parts and a 25% universal tariff on steel and aluminium. These measures create headwinds for some of Turkey’s core export sectors, particularly automotive and metals, though the overall impact is contained given that the US accounts for only 5–6% of Turkish exports and most trade is conducted under the EU Customs Union. While higher US tariffs present a challenge, their overall effect on Turkey’s external position should remain limited, especially given the country’s heavier reliance on EU markets and scope to capture share in sectors such as textiles where competitors face steeper barriers.

Growth dynamics are mixed but not alarming. Turkey’s GDP is expected to expand by 2.8% this year, slower than 2024’s 3.2% but still resilient given the monetary tightening earlier in the year and subdued global demand. Industrial production has held up better than expected, rising 8.3% in June, though forward-looking indicators point to softness: the manufacturing PMI fell to 45.9 in July, signalling ongoing contraction in the sector. A slower pace of growth is not entirely unwelcome, as it helps consolidate disinflation, though policymakers will be eager to avoid a sharper slowdown that could undercut employment and domestic demand.

Our TRY/USD Outlook

Where do we see USD/TRY?

Looking at the lira’s trajectory over the next three months, the most likely scenario is continued gradual depreciation, but within a more orderly and predictable range than in past years. We place USDTRY in the low 41 by the end of September. This reflects the expectation of further rate cuts and modest trade pressures, but also acknowledges the improved backdrop of lower inflation, a narrower current account deficit and firmer investor sentiment. In short, the lira is expected to weaken, but in a controlled fashion that is far less destabilising than the sharp selloffs that defined earlier episodes.

Risks remain, and investors cannot ignore them. Domestic politics will continue to cast a long shadow: the March crisis was a reminder of how quickly political events can unsettle markets. Global risk appetite, too, is a key variable. Emerging-market currencies remain vulnerable to shifts in US yields or global geopolitical shocks, and Turkey’s relatively thin buffers could be tested again if sentiment turns. Finally, the central bank’s delicate balancing act between supporting growth and maintaining credibility will determine whether the lira’s gradual weakening path remains intact.

Overall, however, the outlook is relatively positive for investors. Turkey has emerged from its spring crisis with improved macroeconomic indicators, a more stable external position and recovering policy credibility. Inflation is easing, monetary policy is moving in a more conventional direction, and trade diversification helps cushion tariff shocks. These dynamics suggest that while the lira is likely to continue softening in the coming quarter, it will do so in a more measured way, providing a far more predictable environment for investors. For a currency that has spent years synonymous with volatility, that alone marks a meaningful step forward.

Desk Comments

GBP

The BoE cut the target rate by 25bps to 4% as expected, with the vote split proving noticeably more hawkish than anticipated. A 2-5-2 split (50bp cut – 25bp cut – hold) had been forecast, but the actual 1-4-4 division indicates that members remain concerned about inflation risks. Sterling rose following the release.

However, a leading indicator for UK CPI, which successfully predicted last year’s rebound, now points to a renewed slowdown in price growth. This should ease inflation concerns sufficiently to soften the hawkish stance. Simultaneously, forward-looking data suggests the UK economy will continue to weaken, further strengthening the dovish members’ case for additional policy easing.

Although the market is currently paring back expectations for BoE rate cuts this year and into next, that trend may reverse as inflation moderates and hawkish resistance begins to fade.

EUR

The eurozone economy showed signs of regaining momentum in July, with PMI data exceeding expectations. Inflation remained steady at 2% YoY, slightly above the anticipated decline to 1.9%.

On 27 July, the EU and US agreed a trade deal imposing a 15% tariff on most EU imports, including cars and car parts, which had previously faced tariffs of up to 27.5%. However, the effects of these tariffs were not entirely beneficial, with sectors such as pharmaceuticals seeing an increase from 0% to the new 15% rate. A notable aspect of the agreement is the EU’s pledge to purchase $750 billion worth of US energy products, equating to $250 billion annually during Trump’s presidency.

USD

The USD has been on the back foot recently, driven by speculation surrounding the next Fed Chair, the latest economic data, and ongoing trade negotiations.

Trump has seized every opportunity to criticise Powell for not cutting interest rates sooner. A vacancy has emerged on the Fed’s Board of Governors following Adriana Kugler’s resignation - an opening Trump views as an early chance to influence Fed leadership by appointing someone who could potentially replace Powell when his term ends next year. The appointment is expected to be dovish on rates, leading markets to price in further cuts in the short term.

Last month’s labour market data came in lower than expected, with significant downward revisions to previous releases, underscoring a clear cooling trend. The substantial misses in recent non-farm payroll (NFP) figures may signal deeper underlying weakness in the labour market than markets are currently pricing in.

On the geopolitical front, Trump’s positive discussions with Zelensky have raised hopes for a potential ceasefire. The prospect of a diplomatic breakthrough has contributed to a risk-on sentiment in markets and added to USD weakness.

US Labour Market

Investors watch closely for signs of cooling in jobs data.

Technical Analysis

EURUSD

EURUSD failed to sustain a break above the 1.1800 level, reversing its uptrend and retreating to test trendline support around 1.1650. Continued USD strength pushed the pair lower, where it found clustered support near 1.1400. The next key support zone lies between 1.1162 and 1.1184, marked by the 38.2% Fibonacci retracement and the 200-day moving average. Renewed speculation over the next Fed Chair, combined with weaker U.S. labour market data, has supported a rebound in EURUSD, reopening the path toward 1.1800. A break above that level could see further upside toward 1.1912, followed by the psychologically important 1.2000 handle.

GBPUSD

GBPUSD broke to the downside of the upward channel, testing the 100-day moving average and the December 2024 lows at 1.3135. To resume the uptrend, a break above 1.3588 is crucial, which would open the door to retesting the previous highs at 1.3789. A sustained move above 1.3789 would pave the way for a push toward the key 1.4000 level.