Executive Summary

- The US economy remains resilient with strong consumer spending, and a tight labour market.

- Inflation is declining, with expectations of a gradual easing of monetary policy starting with a 25bps Fed interest rate cut in March.

- The eurozone entered 2024 teetering on the brink of recession, with deepening contraction in manufacturing and services sectors.

- China continues to face challenges of low consumer confidence, weaker global demand, and intensifying property crisis.

- Brazil's economy grew by about 3% in 2023, but faces challenges in 2024 with reduced agricultural output due to adverse weather brought by El Nino.

- Starbucks ended Q4 2023 on a high note, with an 8% increase in global comparable store sales and record consolidated net revenues of $9.4 billion.

- Nestle and JDE Peet’s reported contrasting performances: Nestle experienced strong organic growth, particularly in emerging markets and e-commerce, while JDE Peet’s faced challenges with lower organic sales growth and a decrease in underlying profit due to price increases and volume decreases.

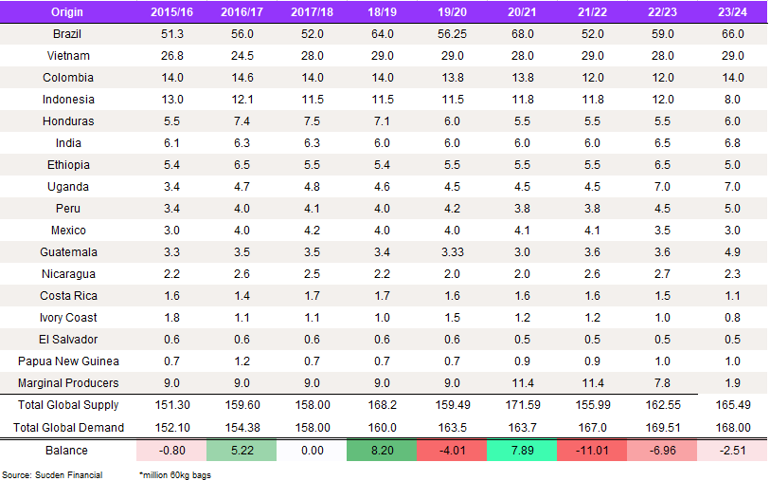

- The industry remains reliant on Brazil and Vietnam, accounting for 58% of the total blend.

- Our outlook for Brazil is at 66m bags for 2023/24.

- Although the weather is still a concern, we believe that most of the damage has been done, and the expectations of a super crop are likely to fade.

- It is difficult at this time to determine how the farmer will react but if they hold their nerve, we expect that they would attain a good price level.

- Vietnam has enough coffee to be shipped, but the industry might be reluctant to purchase in large quantities due to farmer selling between VND70,000-72,000.

- As a result, we have seen a bigger shift toward conillons, but the industry will still need Vietnam for now as there is little replacement for this origin.

- We remain optimistic about both contracts but believe that the most recent rally has been overdone, and we expect a marginal retracement in the near term.

- There is no shortage of coffee overall, but there are gaps in certain regions creating uncertainty regarding coffee accessibility.

Our View

The coffee industry witnessed turbulent prices last year, affecting both Arabica and Robusta contracts. The industry remains reliant on Brazil and Vietnam, accounting for 58% of the total blend. However, the market has been questioning which type of coffee will be in higher demand, resulting in a greater appetite towards Robusta for the majority of 2023. This has prompted contract prices to multi-decade highs of $3,200/mt, leading Arabica prices to drop to 145 cts/lb. In Q4 2023, the sentiment changed, due to the threat of El Nino and other weather concerns, pushing the KC contract to test the 200 cts/lb level – the high not seen since April 2023. Low certified stocks were also supportive of coffee prices. Although the weather is still a concern, we believe that most of the damage has been done, and the expectations of a super crop are likely to fade. Our outlook for Brazil is at 66m bags for 2023/24. Vietnam has enough coffee to be shipped, but the industry might be reluctant to purchase in large quantities due to farmer selling between VND70,000-72,000. We remain optimistic about both contracts but believe that the most recent rally has been overdone, and we expect a marginal retracement in the near term.

We have noted changes in other coffee origins for the 2023/24 crop. From India and Indonesia, we expect to see a production of 6.8m and 8.0m for these regions, respectively. For Central America, shipments have been quite slow, but we expect to see softer differentials as we enter the new year with the possibility of some coffee heading for certification for the May contract onwards. In particular, Honduras exports expanded by 63% y/y to 110,000 bags, and we expect to see 6.0m to be supplied by the region in 2023/24.

Macro Overview

US

Compared to expectations this time last year, the outlook for the world’s largest economy in Q1’24 remains positive, showing no signs of the recession that was once a topic of concern. Resilient output growth continues despite certain sectors of the economy, particularly real estate, feeling the pinch from the elevated interest rates. The recent GDP print for Q3’23 came out at 4.9% YoY, marking the biggest rise in 2 years, leading economists to lift the forecasts for 2023 GDP growth to 2.4% YoY. These relatively high numbers can be attributed to strong consumer spending, which continues to be underpinned by a resilient labour market. Unemployment rate is hovering near a 50-year low, with the recent reading at 3.7% YoY in November, demonstrating ongoing strong job creation bolstered by an increase in the labour force. Notably, the labour force participation rate, especially among individuals aged 25-54, has seen a significant uptick since last year. Weekly jobless claims continue to fall short of expectations while nonfarm payrolls remain higher than the pre-pandemic norm, suggesting that overall economic growth is likely to maintain a steady pace without significant downturns in the coming quarter. Despite variances in consumer confidence, spending patterns indicate a level of optimism about personal financial situations. Retail sales have shown consistent strength as reduced inflation has resulted in increased disposable income for households. In November, for the first time in over three and a half years, US prices experienced a monthly decline, leading to a reduction in the yearly inflation rate to 2.6%. As the Personal Consumption Expenditure (PCE) index - the Fed’s preferred inflation gauge – approached the target 2% level, the markets adjusted their expectations of interest rates cuts with projections settling below 4% by 2025. That would mean more than 125bps decrease over the course of the year. While we believe that the cycle of rate hikes is now over, monetary easing will not be as rapid as the markets expect, as such steep cuts could undermine the work that has already been done to soften inflation, especially with unemployment remaining at historically low levels. We expect the first 25bps interest rate cut to materialise in March and until then a ‘’data-dependent’’ narrative from the policymakers, aiming to prevent premature expectations of rate cuts from excessively lowering Treasury yields. With the US government's cost of borrowing and mortgage rates at elevated levels, market dynamics are effectively aiding the Fed’s efforts, reducing the need for further rate increases. Overall, US economy will likely remain resilient in the coming quarter with solid consumer spending and a robust, albeit moderating labour market. We expect inflation to hover around the 3% level while the central bank starts to gradually ease monetary policy.

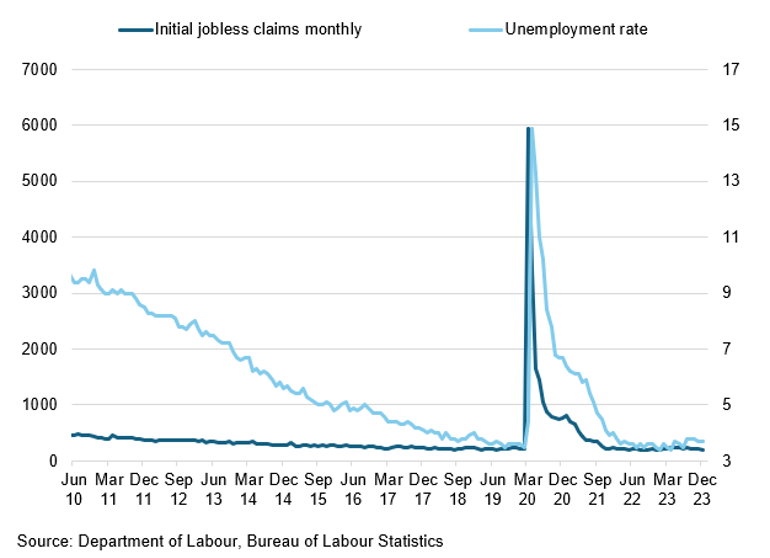

US Labour Market

The unemployment rate remains at a historically low level.

Europe

While the eurozone managed to avoid fully fledged recession in 2023, the common currency area entered 2024 on the back foot relative to its younger cousin from the other side of the Atlantic. The last two quarters of 2023 saw the eurozone teetering on the brink of a recession after months of weakening in manufacturing and services activity. Business activity remained stuck in contraction at the end of the year with the December HCOB Composite PMI reading at 47.6, unchanged from the previous month. Both manufacturing and services output continues to fall as the region struggles to remain internationally competitive amid ongoing conflict in Ukraine and deepening structural problems. Unstable energy prices led many multinational companies to either pause their investment strategies or, in more extreme cases, establish new production facilities out of the continent in countries like the US or China. Germany, accounting for 29% of eurozone’s GDP, is particularly affected by the changes in energy supply and decreased investment. As a leading player in the European manufacturing value chain, the country's underperforming manufacturing sector continues to impact other countries in the region. In addition, the recent budget approval crisis in Germany will likely result in the implementation of austerity measures at the time when the block’s largest economy struggles to rebound from an economic downturn. We expect another quarter of stagnation in the eurozone with business activity remaining below the 50-point mark. At the same time, we believe that the block will continue to avoid full-blown recession as business and consumer confidence is bound to improve with price pressures abating. While the headline inflation rose in December to 2.9% YoY from 2.4% YoY recorded in November, it was mostly driven by the expiration of government energy subsidies implemented amid the energy crisis in 2022. The annual core inflation continued to soften in December, falling to 3.4% from 3.6% in the previous month. At their latest meeting, the ECB left the interest rates unchanged, reiterating data-dependent approach when it comes to deciding on the path of monetary policy in 2024. Although we do not expect the European policymakers to start monetary easing before the Fed, they will likely adopt a similar timeline, particularly since Europe’s economy remains susceptible to an unwarranted economic slump.

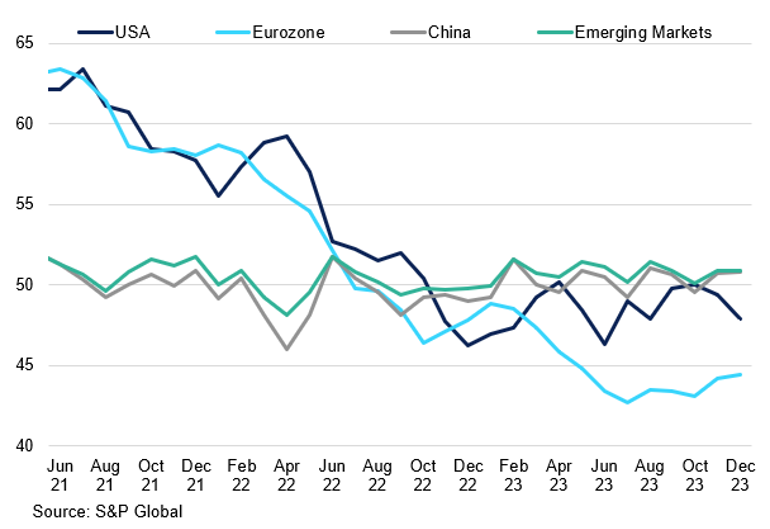

Major Economies Manufacturing PMIs

Eurozone manufacturing activity lags behind other economies.

China

When forming the outlook on the Chinese economy in 2024, it seems crucial to reflect on the dynamics that shaped the country in the past year. The lack of a strong rebound from the covid pandemic, which was expected by economists at the start of 2023, shone a light on the underlying challenges faced by the world’s second-largest economy. The weakening global demand exacerbated by prolonged period of high borrowing costs around the world has proven that China can no longer rely on exporting itself into prosperity, leading policymakers to shift their focus inward. At home, sluggish domestic demand reflected in weak retail sales proved time and time again the lack of consumer confidence amid ongoing property sector crisis, deflationary pressures, and record-high youth unemployment. The policymakers found themselves between a rock and a hard place trying to implement adequate stimulus while taming risks in property and local government debt without triggering disorderly spillovers. Among policy measures announced last year, authorities have bolstered specific sectors, including an extension of tax breaks for electric vehicle purchases. Additionally, in 2023, the government raised 152.3 billion yuan ($21.05 billion) via special bonds to provide capital for small and medium-sized banks to finance infrastructure spending. While complex challenges remain, China’s economic downturn managed to stabilise in recent months with the GDP growth expected to reach the 5% target set at the start of 2023. Looking forward to the first quarter of 2024, China’s economic performance will likely remain muted while policymakers continue to implement further policy measures aiming at maintaining current growth levels. We are entering the new year with reduced expectations regarding the world’s second-largest economy, anticipating low levels of consumer confidence to remain as the real estate crisis intensifies.

China’s Property Market

China’s real estate market crisis intensifies.

Brazil

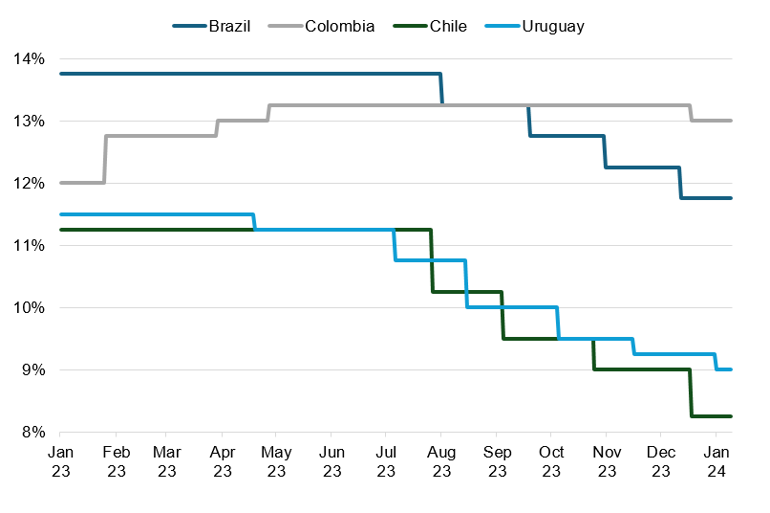

While at the start of last year the predictions for GDP growth in Brazil were at around 1%, the largest Latin American economy beat expectation in 2023 growing at around 3%. However, economists highlight that much of 2023's growth was concentrated in the first half of the year, with a noticeable slowdown from Q3, leading to a more cautious outlook for 2024. The significant contributions from fiscal stimuli and agrobusiness seen last year will likely diminish further in the coming quarter as the exceptional heat and dryness brought by El Nino weights on planting and harvesting. Adverse weather conditions have already prompted a 1.4% reduction in Brazil’s 2023/2024 soybean harvest forecast, which will undoubtedly lead to a significant decrease in exports. At the same time, the outlook for the industry remains bleak. While the December tax simplification reform, which introduced a dual value-added tax system, should attract foreign investment by streamlining fiscal processes, the slump in manufacturing activity will likely weigh on economic performance in the coming months. The Manufacturing PMI fell to 48.4 in November, indicating a deepening contraction. Consumer demand also remains subdued with the latest retail sales reading in October at a five-month low at 0.2% YoY, well below a 10-year average of 3.2. As 2024 begins, Brazil confronts a difficult economic environment, where stringent monetary policy continues to impact activity despite expectations of a gradual decrease in the key interest rate. The BCB was among the first to shift to a dovish policy, beginning its easing cycle in August. Following four consecutive rate cuts in the second half of the year, the interest rate was brought down to 11.75%. While further monetary easing is on the table for the coming months, we expect the scale of cuts to subside and for the cash rate to find support at the 9.25% level.

Latin America Interest Rates

Brazil was one of the first countries to start easing monetary policy last year.

Corporate Results

Starbucks

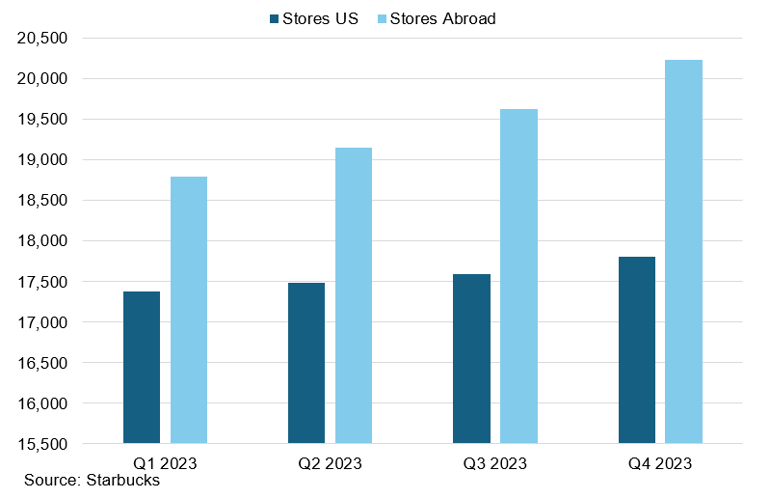

As the company celebrated the 20th anniversary of its iconic Pumpkin Spice Latte, Starbucks finished Q4 2023 on the higher end of their full-year guidance. Global comparable store sales increased by 8%, softening from 10% seen in Q3. North America sales were up by 8%, whereas international sales saw an increase of 5%. Out of the international sector, China’s growth was up by 3%, marking a significant softening from 46% recorded in Q3. The average ticket – or cost per order – rose by 4%, while comparable transactions increased by 3%. This means that customers visited more often and spent more per trip, contributing to increased revenue for the company. Consolidated net revenues as a whole grew by 11% to a record of $9.4 billion, suggesting that the hardships brought by the long period of elevated borrowing costs has not affected consumer’s willingness to buy their favourite drinks. The number of members signed up to the Starbucks rewards loyalty programme in the US increased by 14% YoY, reaching 32.6 million customers. September marked the 5th anniversary of the Global Coffee Alliance with Nestle, which brought together Starbuck’s brand strength with Nestle’s production capabilities and extensive market presence.

Starbucks New Stores

The company was consistently opening new stores last year, ending the year with 17,810 stores in the US and 20,228 abroad.

Nestle

Nestle’s organic growth was up by 7.8% in the nine months ending October, with real internal growth (RIG) of -0.6%, impacted by portfolio optimisation activities and remaining capacity constraints. Pricing with negative RIG led to a lower organic growth in developed markets compared to emerging markets at 6.9% and 9.0%, respectively. Coffee sales saw growth at a high single-digit rate supported by a surge in Starbucks products sales following the introduction of ready-to-drink options in South-East Asia and Oceania. Organic growth in retail sales maintained a strong momentum at 7.1% while E-commerce sales saw a 12.7% increase, accounting for 16.6% of the total Group sales. In North America, sales in the Nestlé Professional and Starbucks out-of-home sectors continued to expand at a robust double-digit rate, driven by the acquisition of new customers and the momentum in e-commerce. Meanwhile, the beverages category, which encompasses Starbucks products, Coffee mate, and Nescafé, achieved mid-single-digit growth. In Europe, Nescafé showed the strongest performance, leading the coffee category to experience growth in the mid-single-digit range. The company expects organic sales growth for the whole 2023 to reach between 7% and 8% with underlying trading operating profit margin slightly above 17%.

JDE Peet’s

The latest half-year financial results show JDE Peet’s organic sales increasing by 3.5% in H1 2023 as a 6.8% increase in price balanced out a 3.3% decrease in volume. In-Home sales increased by 2.2%, while sales in Away-from-Home jumped by 9% on an organic basis. Unfavourable impact from fair value changes in derivatives and forex, as well as a lower level of operating profit led the underlying profit – excluding all adjusting items net of tax – to decrease by 21.4%. In Europe, organic growth increased compared to H2 2022, albeit at a slower rate than originally expected. The 0.3% growth was driven by an increase in price of 8.9% and a decrease in volume of 8.6%. While the Away-from-Home segment saw a positive volume performance, it was more than offset by a volume decline in the Consumer Package Goods segment. The biggest gains were seen in France, Switzerland, and most Easter European markets while best performing brands included L’OR, Kenco and Pickwick. The company performed better in the US where organic sales growth reached 8.6% driven by an increase of 5% in price and 3.5% rise in volume.

Supply

Arabica

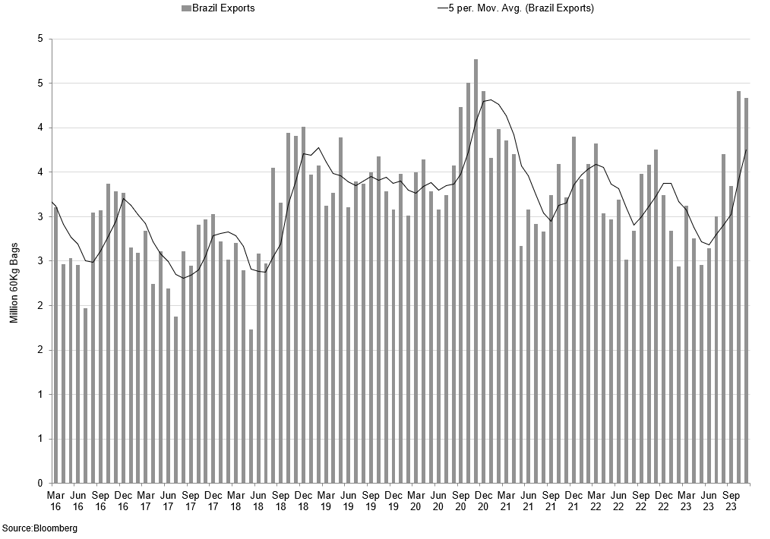

Our feeling last year was that Brazilian farmers were in a strong position and would only sell coffee at firmer prices; this has, in fact, been the case. Roaster buying prompted the jump in prices to above 190cts/lb, meaning that farmers received good value for their shipments. As a result, we have seen a jump in exports from the region: October and November shipments from Brazil combined totalled 6.66m bags, equating to 36% of the 18.3m bags shipped in total. In line with conillon, which totalled 1.53m in the same period, the total contribution from Brazil improved to 44.5%. This highlights the industry’s continued reliance on the region.

Brazil Monthly Exports vs 5-month moving average

With C Contract prices above 170cts/lb, we have seen a strong rebound of export activity from Brazil.

We now enter 2024 with the possibility of a 70m bag crop on the horizon. It is difficult at this time to determine how the farmer will react but if they hold their nerve, we expect that they would attain a good price level. We estimate Brazilian internal consumption at 22m bags and exports at 40m, which would leave a carryover of 8m bags by June 2025. While weather concerns have impacted the conillon crop potential, we see less of an impact on Arabica production. Therefore, this trend is set to continue, especially given softer Brazilian differentials into the new year, at -17 for medium to good bean coffees. For Brazil as a whole, our number for the 23/24 crop is at 66m, with 45m for Arabica and 21m for Robusta. We expect Brazilian farmers to sell into high prices, as industry demand remains robust. In the meantime, the weather is key to assessing the Arabica price trajectory.

The industry has run down its cover, and buying is taking place on a hand-to-mouth basis. The high interest rate environment has prompted the industry to not carry stocks, meaning that they will run close to home. For the 23/24 crop, we see a slight tightness in Arabicas, but with little deficit, in line with what we have seen in 20/21. The 170 cts/lb level seems like a good number to keep the market balanced in our view. With differentials now coming off, some selling is still taking place, albeit at a slower pace.

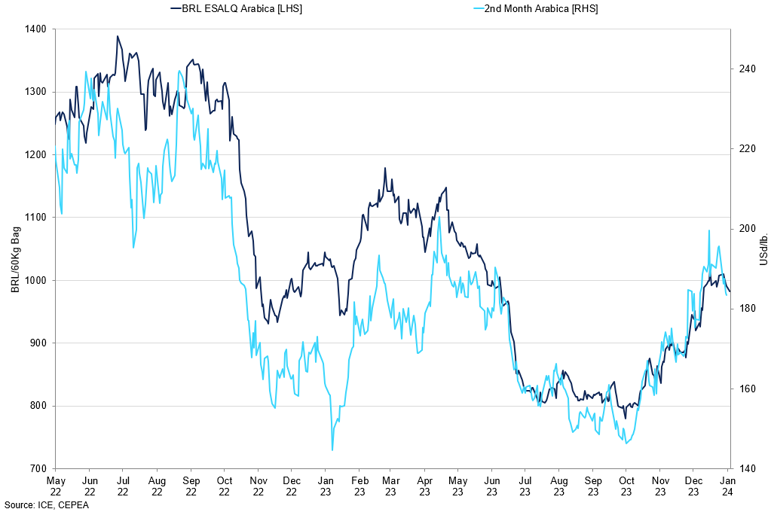

Brazil ESALQ Arabica Prices vs 2nd Month Arabica

At BRL900/bag, the farmer in Brazil is getting a good price for its coffee. This is likely to prompt further selling in the coming months.

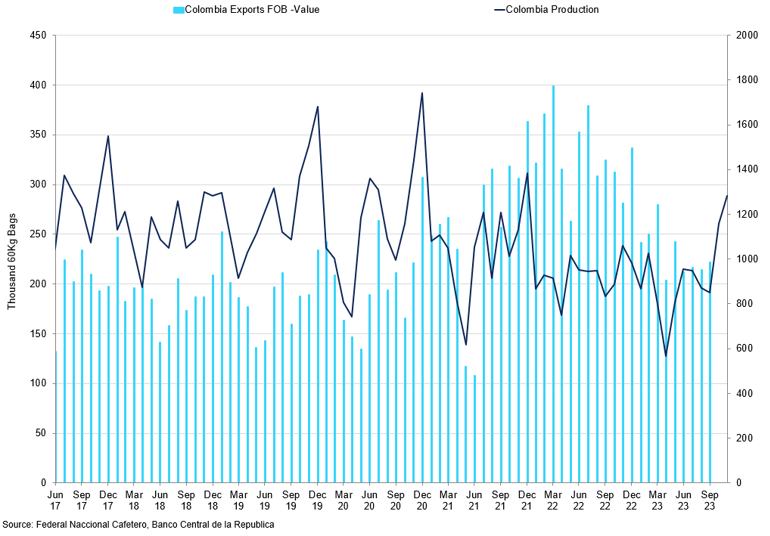

The flow out of Central America has been slow. While stocks remain low at 250,000 lots in certs, there is not a lot of coffee at pending grading, providing little pressure on the market. If the problem with C. America does arise, Colombians and Honduras could help fill in the gap. We have increased our estimates to 14m and 6.0m for these regions, respectively. Colombian diffs have come off strongly in recent months, given the production increase. Indeed, November production stood at 1.28m, up 25%. Honduras exports for November are up 63% y/y at 110,000 bags. We are of the view that some Honduran coffee will start to head for the board, and better-quality coffee will go to the industry. We are starting to see softer differentials but this is a slow process.

Colombia Production vs Exports FOB Value

Colombian production has improved, prompting us to increase our 2023/24 outlook to 14m bags.

Robusta

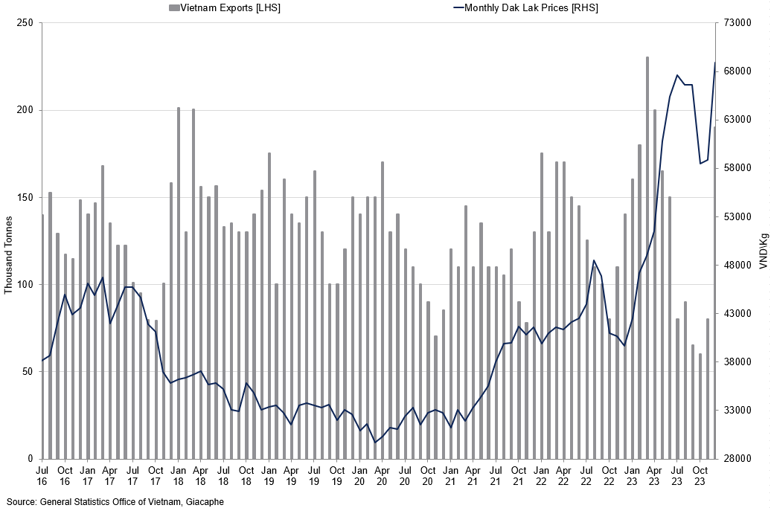

The 22/23 season faced weather issues, resulting in Vietnam having a smaller crop; exports in the region were 27.67m, and internal consumption was around 3.0-3.5m bags. At the same time, demand for Robustas grew over the course of the year, as roasters were substituting Arabicas for cheaper blends. This prompted prices to reach the high of $3,200/mt, which translated into VND70,000-72,000/mt for the farmer. Certified stocks have drawn down to 3,440 lots, which also added to the upside momentum and no real gradings to slow prices. Although demand from big industry buyers is similar to last year, we believe the price is holding the industry back from purchasing in large quantities. As a result, we have seen a bigger shift toward conillons, but the industry will still need Vietnam for now as there is little replacement for this origin. We expect Brazilian shipments of conillons as a proportion of total exports to expand in the coming months.

Vietnam Exports vs Monthly Dak Lak Prices

Despite local prices jumping to multi-decade highs, exports are lagging behind.

Our 2023/2024 Vietnam crop forecast is at 29m bags, which should provide enough coffee. Overall, we do not expect a shortage of Robustas, as most of it is likely to be shipped and not kept internally. With 496,000 bags of conillons shipped in December, we expect more conillons to come out for Robusta grading. In the meantime, farmers remain resilient, knowing the industry will buy the coffee in time.

Conillon

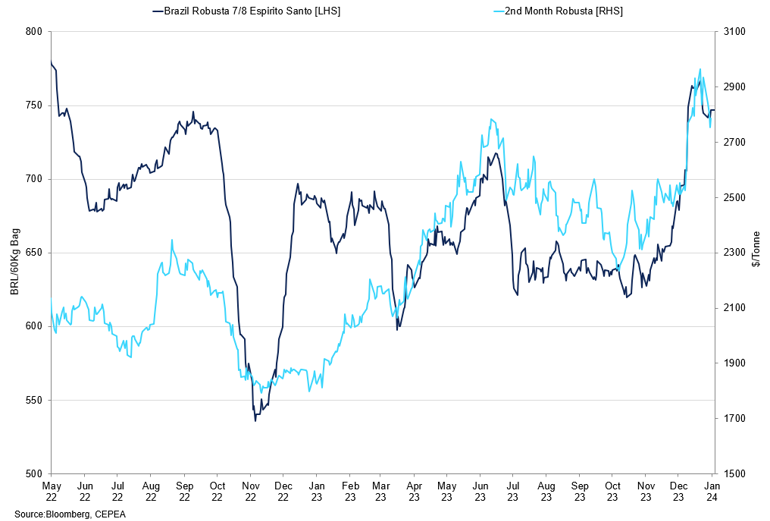

Coffee areas in northern Espirito Santo have not received widespread rains as expected for this time of year. The region is essential for conillon cultivation, which is home to 90% of the current crop. Due to dry weather conditions in recent weeks, there are concerns about the damage that it could cause to the May crop. This is especially worrisome given the high temperatures seen from El Nino threats. Damage estimates now range from 15% to 35% as a result. Although we believe the final impact to be smaller, at 10%, any potential rain will not be enough to reverse the damage that has already been done to the crop. While most farmers in the region use irrigation systems to keep the soil moist, there is no effective way to curb the impacts of the heat. Additional limitations by local governments on the use of irrigation, given limited water reserves, are likely to add further pressure on conillon production. It is key to keep an eye on the situation constantly.

Brazil Conillon Prices at 7/8 Espirito Santo vs 2nd Month Robusta

A shift towards Conillon shipments prompted prices to reach summer 2022 highs.

As a result of the recent lack of rain, we have seen May 2024 conillon crop expectations downgraded all the way from 25-26m bags to 20m. Our estimate for the next crop is 21m bags, accounting for the potential damage that could take place during hot temperatures. The current structure for spread for Conillon is at 3 over. In particular, out of 4.3m shipped in November, the conillon number amounted to 855,000 – the highest number in over five years. The shift back from Robusta to cheaper blends is driving this momentum. Additionally, Vietnamese coffee prices remain elevated, and with freight more expensive than from Brazil, appetite for conillon is set to expand in the coming months, helping to tighten the arb.

Inventories

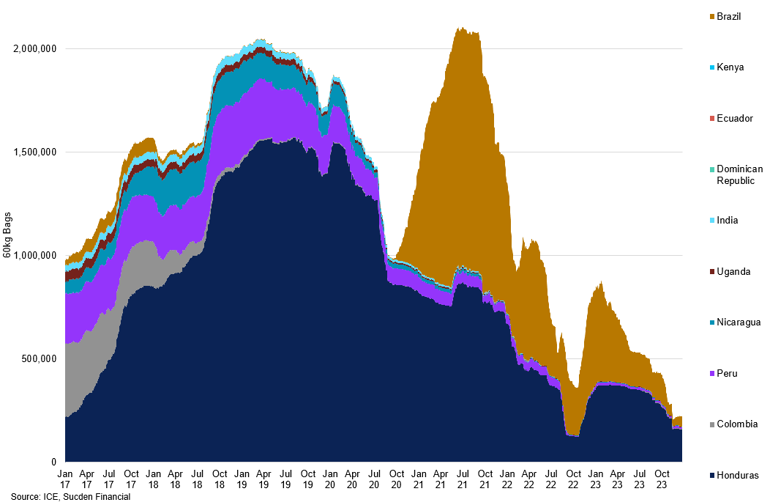

We have seen continued drawdowns from certified stocks, with Arabica levels falling to 1997 lows of 253,144 bags as of January 4th. Currently, we have 52,000 bags in Brazil and 159,032 in Honduras. Despite this being a multi-decade low, the market is not responding drastically to it. Instead, it is supporting the upward momentum and focusing more on the supply story than the demand. Speculations over consumption concerns have been in play since the start of the pandemic, and more attention is being paid to the supply story rather than demand. Central American shipments have been slow, but in our view, some of it will start heading for the boar, and better quality will go to the industry. However, the amount of coffee being attracted to the C contract will depend on the shipments from Brazil.

Coffee Inventory Levels per Location

Stocks have experienced strong drawdowns in 2023, driven in large by Honduras and Brazil.

From Robusta's perspective, we have also seen some strong drawdowns on the certified stocks. In particular, from December 30th 2022 to December 30th, 20223, drawdowns reached 3000 lots. Still, Robusta certs still have some more room to fall, and we expect to see marginal drawdowns in the coming months. Industry has increased their Robusta usage, but at $3,000/mt, these prices are high. The farmer in Vietnam had a profitable 2023 and, as of today, is looking for levels of VND70,000-71,000/mt, which are higher than he received in 2023. In our view, Conillon is the cheaper alternative for the industry.

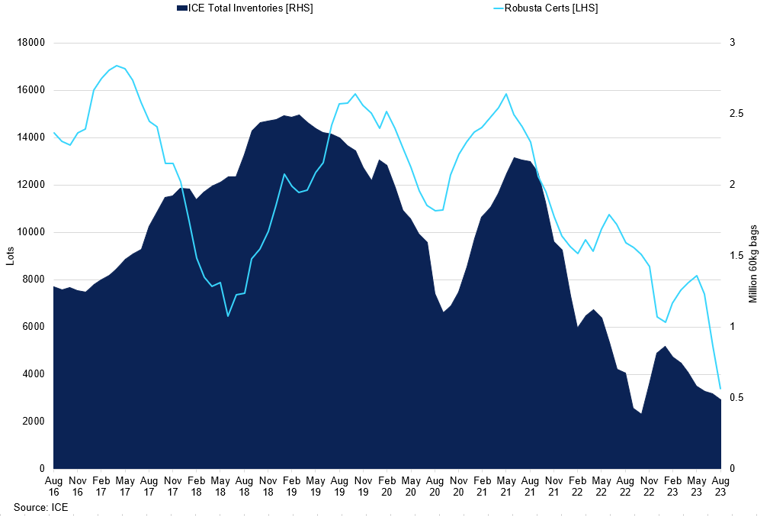

ICE Total Inventories vs Robusta Certs

We have seen strong drawdowns from Robusta certified stocks but believe there is still more room to fall.

Commitment of Traders

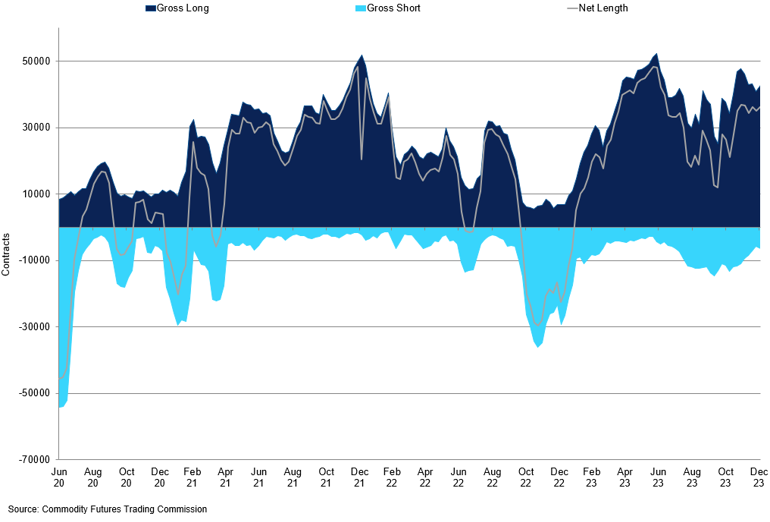

After the recent rally, the net length of managed money for Arabica remained high at 22,556. The gross long contracts supported the upward trend with 48,768 contracts as of January 5th. Short contracts remained mostly unchanged at 26,212 over the past few weeks, indicating that the bullish investors have taken control of the market. However, there seems to be a delay between price changes and the corresponding COT positions. For instance, funds were 22,000 short as of October 2023, and it took some time for the momentum to become more positive. Only after prices crossed the 180 cts/lb level did investors turn long, which suggests that Arabica contracts might be more vulnerable than Robusta. Even if there is an increase in Robusta demand, Brazil's fall in the market is expected to be slow.

Arabica Managed Money Commitment of Traders

Funds are now 48,000 net long, due to a strong increase in long positions.

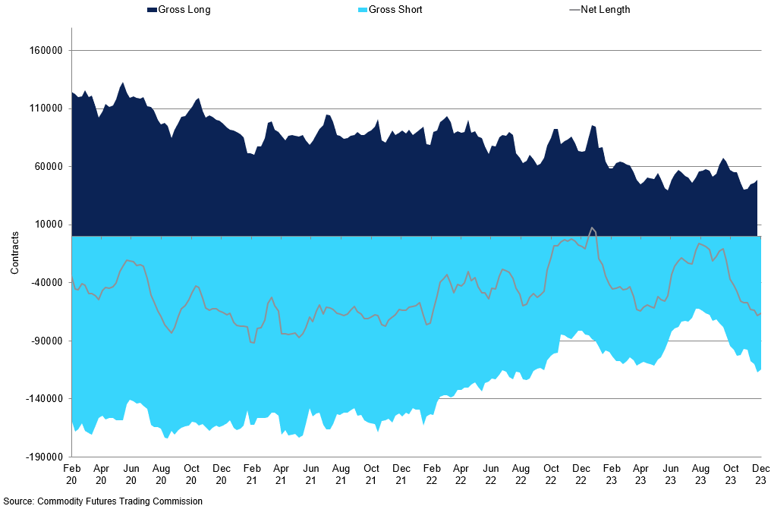

From the commercial perspective, we have seen roaster positioning decrease its net long position to -87,856 contracts. Industry was the buyer down to 145 cts/lb last year, while funds did the selling. It looked like Brazil and Colombia started to sell lightly into the 160s and that selling increased with Central America joining the party. We believe that industry has some catching up to do on the buy side, as their cover was drawn down.

Arabica Producer Commitment of Traders

Arabica producers are now as short as they have been at the start of 2022.

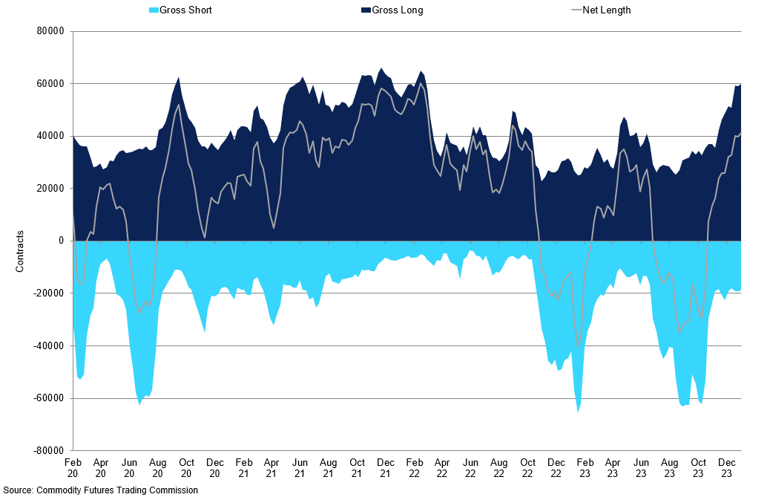

Managed money positions have kept their net long elevated at 23,193 contracts, as of January 5th, with gross long at 38,306 and short at 15,113. The farmer seems comfortable at around VND70,000-71,000 level. A small correction in pricing from the current levels would still be favourable for the seller, however the business is slow, with industry lacking appetite to pay these levels. Moreover, with 70% of Robusta crop harvested, and the new Brazil conillon crop coming in May, industry might be holding back on their Vietnam buying. A turn around in softs market could push coffee prices higher.

Robusta Non-Commercial Commitment of Traders