EUR / USD

EUR/USD has demonstrated remarkable strength, surging 1.8% amid significant shifts in European fiscal policy and mounting US economic uncertainties. Germany's decision to relax its borrowing constraints, coupled with the European Commission's €150 billion defence funding proposal, has provided substantial support for the euro, signalling a decisive shift away from fiscal restraint.

The pair has successfully breached critical technical barriers, including 200-day moving average resistance at 1.0723, approaching another key resistance level of 1.08. The dollar's weakness has been exacerbated by disappointing US private payroll data, with only 77,000 jobs added in February against an expected 140,000, alongside growing concerns about the impact of newly implemented tariffs against major trading partners.

Although the ECB is expected to implement over 60bps of cuts this year, recent developments indicate that US monetary policy is facing uncertainty due to tariff-induced inflation expectations. However, market participants should still remain cautious as escalating global trade tensions could eventually impact European growth, particularly if US tariffs expand further in April, potentially triggering a bearish reversal and a retest of support around 1.036.

In the meantime, we believe the pair to be overbought at these levels, and the 200 DMA could act as a support level, assuming the ECB will cut rates by 25bps today, in line with market expectations.

USD / JPY

USD/JPY experienced slight downward pressure despite a dollar sell-off yesterday, suggesting that technical support levels are keeping the pair mostly rangebound. The Japanese yen has found substantial support from the Bank of Japan's increasingly hawkish stance, with Deputy Governor Uchida signalling a continued upward trajectory for interest rates, while positive economic indicators like the Jibun Bank services PMI reaching a 6-month high further bolster the yen's position.

Conversely, the US dollar faces multiple challenges, including disappointing economic data highlighted by the February ADP employment report showing the weakest job gains in seven months, while uncertainty around tariff implementation with major partners, such as Canada and Mexico, complicates the trade outlook.

The combination of rising Japanese government bond yields and the yen's safe-haven appeal, particularly amid US trade policy uncertainty, suggests continued pressure on the USD/JPY pair, with potential for further downside if the critical support level at 148.40 fails to hold.

GBP / USD

GBP/USD continued its rally, pushing above key resistance levels and reaching 1.2895 despite broader economic uncertainties. Technical indicators suggest the pair is heavily overbought with an RSI of 71.40, with current support above all major moving averages, particularly the crucial 200-day MA at 1.2788.

Recent UK Services PMI data showed marginal improvement to 51.0 in February from 50.8 in January, providing fundamental support for sterling, although the Bank of England maintains a cautious stance on interest rates due to persistent inflation concerns. The US dollar's position has weakened following disappointing ADP employment data, creating additional tailwinds for the pair.

Although the US has not made any tariff announcements regarding the UK, the BoE Governor has warned that these could negatively impact British consumers' purchasing power. Should current momentum persist, the pair could target the 1.300 mark – a November high, though we believe that profit-taking at current overbought levels might trigger a pullback toward the 200 DMA at 1.2788.

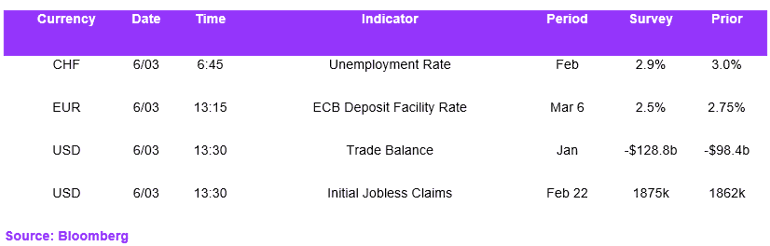

Economic Calendar