EUR / USD

The EUR/USD outlook is shaped by several significant macroeconomic factors. The Federal Reserve appears poised to begin its easing cycle with a rate cut in September following weak US employment data, with August showing only 22,000 jobs added and unemployment rising to 4.3%. The labour market weakness in the US has dramatically increased expectations for Fed rate cuts, with markets now pricing in a 90% probability of a cut this month. Persistent inflation remains a concern, with US CPI expected to rise to 2.9% annually in the August data.

Meanwhile, the European Central Bank is expected to maintain rates steady at its upcoming meeting, though political uncertainty in France with a confidence vote adds complexity to the Eurozone outlook.

The diverging monetary policy paths between the Fed and ECB, combined with heightened political risks in Europe and shifting economic momentum in both regions, suggest continued fundamental support for the currency pair.

USD / JPY

The Japanese Yen faces significant headwinds following Prime Minister Ishiba's sudden resignation, which introduces political uncertainty at a crucial economic juncture. The Bank of Japan's normalisation path may experience temporary delays amid this political transition, with potential successors like Sanae Takaichi advocating for more expansionary fiscal policies and showing scepticism toward BOJ rate hikes. The interest rate differential between the US and Japan remains substantial at 3.75-4%, continuing to favour USD strength, while the recent US-Japan trade agreement, reducing auto tariffs, provides some support for Japan's export sector.

Market participants are particularly focused on the BOJ's upcoming September and October meetings, which will be critical in determining monetary policy direction amid the leadership vacuum. The political uncertainty could trigger increased volatility in Japanese Government Bonds, particularly at the longer end of the yield curve, as concerns about fiscal discipline mount. Recent economic indicators show Japan's economy expanded 0.3% in Q2, with external demand rebounding 0.8%, suggesting some resilience despite earlier trade pressures. A record 6.3% minimum wage hike in Japan adds to inflationary pressures and could influence the BOJ's policy calculations, though the central bank may now be more hesitant to adjust policy amid the political transition.

This political uncertainty is likely to keep the pair volatile in the near term; however, technical support and resistance levels in the form of 50 and 200-day moving averages, respectively, will be key in suggesting a sustained breakout of the current ranges.

GBP / USD

The GBP/USD outlook is shaped by significant shifts in monetary policy expectations and labour market dynamics. Recent weak US jobs data, showing only 22,000 positions added in August versus 75,000 expected, has dramatically increased the probability of a Federal Reserve rate cut at the September 16-17 meeting, with markets now pricing in a 90% chance of a 25-basis-point reduction and a 10% chance of a 50-basis-point cut. The unemployment rate rose to 4.3%, a four-year high, further strengthening the case for Fed easing, particularly as June's employment figures were revised to show the first job losses since late 2020. Political uncertainty adds another layer of complexity, as Trump's attempts to influence Fed policy and potential leadership changes create questions about central bank independence.

The Bank of England's relatively hawkish stance, maintaining rates at 4.0% while showing concern about persistent inflation pressures, provides underlying support for sterling. However, the UK faces its own challenges, including a housing market slowdown and weakening construction activity, which could limit sterling's upside potential.

The divergence between Fed and BoE policy paths, combined with broader economic uncertainties, suggests continued volatility in the GBP/USD pair through year-end.

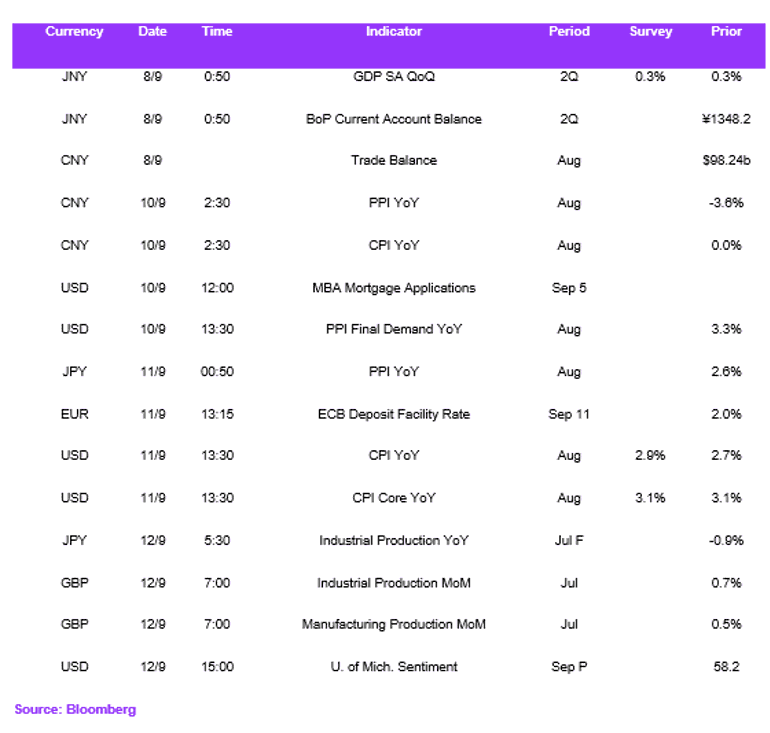

Economic Calendar