EUR / USD

The euro has demonstrated remarkable strength over the past week, appreciating approximately 3.0% against the dollar and briefly surpassing 1.20 before dropping towards 1.1850. This appreciation stemmed primarily from the global trend of debasement and uncertainty about US economic policy, rather than robust eurozone economic fundamentals.

Despite the currency's resilience, the eurozone faces significant economic headwinds, with exports declining 3.4% year-over-year and the trade surplus narrowing substantially from 15.4 billion euros to 9.9 billion euros. ECB policymakers have expressed escalating concern about sustained appreciation, with Vice President Luis de Guindos noting that levels above 1.20 complicate monetary policy operations, particularly as eurozone inflation at 1.9% remains below the 2% target.

From a technical perspective, the daily RSI reading of 56 suggests neutral momentum, with a bullish scenario targeting a retest of the recent 1.204 resistance level on renewed dollar weakness. In the meantime, the sharp decline in precious metals, especially silver, which dropped more than 36% on Friday, may prompt investors to shift portfolio allocations away from metals and toward the dollar in the near term. This shift could pressure EUR/USD lower, with moving averages acting as important support. Additionally, this week’s US labour data is expected to show continued strength, likely further bolstering the dollar’s appeal.

USD / JPY

The USD/JPY currency pair recently demonstrated a notable recovery, climbing approximately 1.1% from around 153 to nearly 155, with solid support established near 152, where buyers stepped in aggressively. The pair currently faces overhead resistance at 155 and the 50-day moving average (156.28). With the daily RSI remaining subdued in the low 40s, the pair retains room for further upside before reaching overbought conditions.

From a macroeconomic perspective, Japan's fiscal pressures and elevated debt-to-GDP ratio exceeding 240% constrain the Bank of Japan's ability to sustain monetary tightening, creating structural headwinds for yen appreciation. The Bank of Japan is not expected to implement another rate hike until June 2026, helping to maintain the 300bps interest rate differential, favouring the dollar structurally.

With moves highly influenced by the dollar, we expect the pair to strengthen, aiming to breach the psychological 155.00 mark.

GBP / USD

Despite a recent 1% pullback from multi-month highs near 1.381 to approximately 1.368, GBP/USD remains well-supported above major moving averages, with the 200-day SMA at 1.34 and the 50-day SMA at 1.3450 providing a solid floor. The daily RSI reading near 60 suggests momentum remains modestly bullish despite the recent weakness, with the 1.365-1.368 zone representing a key area for buyers to defend. A successful hold of this support could facilitate another attempt at the 1.385 resistance level.

The Bank of England is expected to maintain its policy rate at 3.75% during this week’s meeting. New forecasts to be unveiled during the February decision will provide critical guidance on the inflation trajectory and medium-term economic outlook, with market participants closely scrutinising forward guidance for signals on future policy adjustments.

Looking ahead, the combination of the Bank of England's measured approach and uncertainty about the direction of US monetary policy, especially amid Kevin Warsh's nomination as Federal Reserve Chair, suggests GBP/USD may consolidate in a relatively narrow range in the near term. Risk factors include any dovish surprises from the BoE that could weaken sterling, or unexpected dollar strength if the incoming Federal Reserve leadership signals a more restrictive policy stance than currently anticipated.

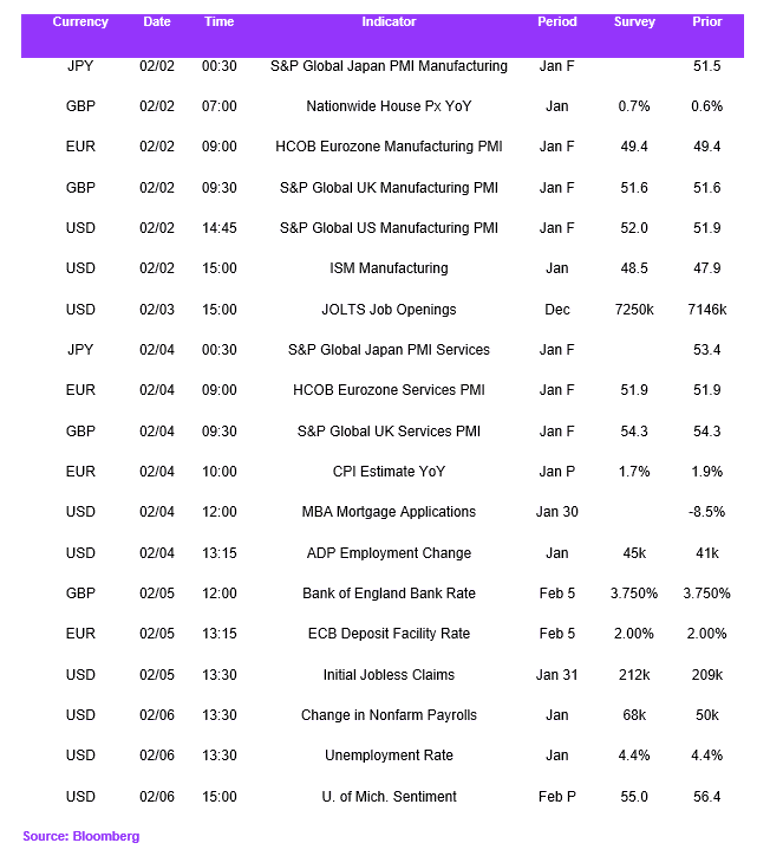

Economic Calendar