EUR / USD

Source: Massive (polygon.io)

EUR/USD is trading near 1.1580, and we see the pair caught between a significant technical ceiling and intensifying macro crosscurrents linked to the Middle East conflict. The cluster of resistance between 1.1600 and 1.1700, including the 200-day, 50-day and 20-day SMAs alongside the 30-day VWAP, remains a critical barrier, and we expect the resolution of this zone to define the medium-term direction.

We see the energy shock from the disruption in the Strait of Hormuz as the dominant macro driver. The eurozone’s dependence on imported energy leaves it particularly exposed, and we expect this to translate into a stagflationary backdrop, with weaker growth and higher inflation. Early signs are already visible in sharply deteriorating consumer confidence, and while PMI data may reflect this trend, we do not expect it to materially shift direction in the current environment.

At the same time, we see rate differentials beginning to shift more subtly. While the Fed–ECB spread remains wide, markets have repriced towards a more hawkish ECB path and reduced expectations for Fed easing. If this continues, we expect some compression in rate differentials that could provide medium-term support for the euro though this remains conditional on the ECB following through.

From a technical perspective, we expect a break above the 1.1600-1.1700 cluster to trigger a move towards 1.1900. Conversely, failure to hold above 1.1485 would confirm the broader downtrend and expose 1.1415. Near-term direction will hinge on whether geopolitical tensions ease and energy prices stabilise. Without that, we expect rallies to remain vulnerable.

USD / JPY

Source: Massive (polygon.io)

USD/JPY remains in a volatile but broadly supported uptrend, and we see the pair increasingly driven by the interaction between energy dynamics and policy divergence. The disruption to global energy flows is particularly negative for Japan, given its reliance on imports, and we expect this to continue weighing on the yen through a deterioration in the terms of trade.

At the same time, we see the Bank of Japan facing a more complicated policy environment. Inflation has softened to 1.6%, below target, which reduces the urgency for tightening, even as policymakers signal a willingness to normalise. In contrast, the Federal Reserve remains relatively restrictive, and we expect this to sustain the rate differential in favour of the dollar in the near term.

Technically, the pair is consolidating around 158.60–158.75 following a sharp rejection from near 160. We see this as a key inflection zone. The RSI has moderated to around 55, suggesting momentum has cooled, while support sits at the 30-day VWAP near 157.50 and the 50-day SMA around 156. We expect a move back towards 160 if energy pressures persist, though the risk of intervention rises significantly into that level.

Looking ahead, we expect USD/JPY to remain highly sensitive to developments around the Strait of Hormuz. A resolution would likely trigger a pullback towards the mid-150s, while prolonged disruption would keep the pair biased higher. We also expect markets to closely monitor any shift in BOJ rhetoric into the April meeting, as well as signs of official intervention near 160.

GBP / USD

Source: Massive (polygon.io)

GBP/USD is consolidating near 1.340, and we see the pair at a key technical and fundamental inflection point. The convergence of the 200-day and 20-day SMAs around current levels is acting as a near-term pivot, and we expect this zone to determine whether the pair can stabilise or resume its broader downtrend.

From a macro perspective, we see sterling facing persistent headwinds. The UK’s exposure to higher energy prices leaves it vulnerable in the current environment, and we expect the ongoing Middle East tensions to reinforce this disadvantage relative to the US. At the same time, while the Bank of England has shifted more hawkishly, rising gilt yields are not providing the usual support for the currency. Instead, we see markets increasingly interpreting higher yields as a signal of fiscal stress and stagflation risk.

This shift in the relationship between yields and the currency is a key development, and we expect it to continue weighing on sterling, particularly if growth concerns intensify.

Technically, we see a sustained break above 1.340 opening the path towards 1.350 and potentially 1.353. However, failure to hold this level and a move below 1.335 would expose the recent low near 1.322 and reinforce the bearish structure.

Looking ahead, we expect GBP/USD to remain driven primarily by geopolitical developments and energy price dynamics rather than traditional macro releases. Any sustained recovery in sterling likely requires a clear de-escalation in the Middle East and improved confidence in the UK macro and fiscal outlook. Without that, we expect downside risks to dominate in the near term.

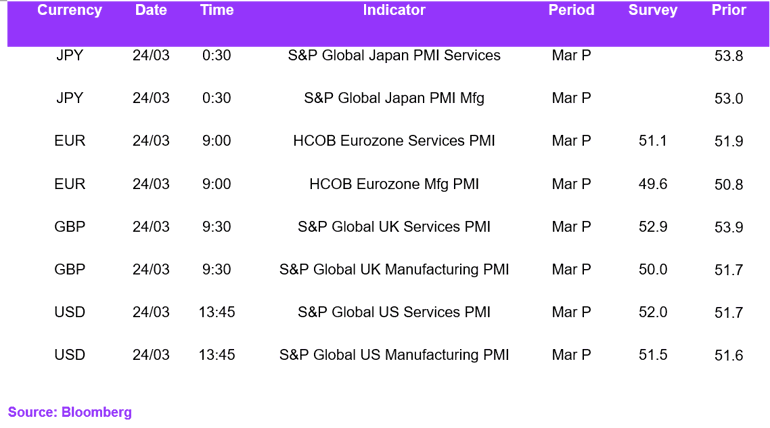

Economic Calendar