EUR / USD

Source: Massive (polygon.io)

EUR/USD remains under sustained bearish pressure, and we see the dominant driver as the asymmetric energy shock stemming from the U.S. Iran conflict and the closure of the Strait of Hormuz. With Brent crude holding above $100 per barrel, we expect the eurozone, as a net energy importer, to face a significantly sharper deterioration in its growth and inflation trade off than the United States, which continues to benefit as an energy exporter.

We also see a reinforcing structural dynamic through dollar demand. Elevated energy prices are increasing the need for dollar funding, as European importers bid for USD to settle energy transactions, creating a mechanical tailwind for the dollar that sits outside traditional macro drivers. This, combined with safe haven flows, continues to underpin broad dollar strength.

On policy, we see a clear divergence. The Federal Reserve has shifted more decisively hawkish, with markets now pricing out most 2026 rate cuts, while the ECB remains constrained by a stagflationary backdrop. Although rhetoric has turned more hawkish, we expect deteriorating eurozone growth, particularly in Germany, to limit the ECB’s ability to follow through aggressively.

Technically, the pair remains weak, trading near 1.1560 and below all key resistance levels, including the 200 day, 50 day and 20 day SMAs as well as the 30 day VWAP clustered above. The RSI near 45 suggests there is still room for further downside. We expect that failure to reclaim the 1.16 resistance cluster would open the path towards 1.1415, with a break below exposing the 1.14 area. In the current environment, we see rallies as likely to be sold into unless there is a meaningful shift in the geopolitical backdrop.

USD / JPY

Source: Massive (polygon.io)

USD/JPY remains structurally supported, and we see the pair continuing to reflect persistent monetary policy divergence combined with energy driven macro pressures. The Federal Reserve’s more hawkish repricing, with markets even assigning some probability to an additional hike, contrasts with a Bank of Japan that is struggling to build a convincing case for aggressive tightening, particularly as inflation data softens.

We see this divergence reinforced by external dynamics. Elevated oil prices continue to weigh on Japan’s terms of trade as a major energy importer, while safe haven flows remain skewed towards the dollar rather than the yen. This combination continues to favour USD strength against JPY in the near term.

From a technical perspective, the pair is trading near 159.43 and remains firmly above all key moving averages, with the 50 day SMA trending higher and confirming the strength of the uptrend. The RSI near 59 suggests momentum is moderating slightly but remains supportive. We expect that a sustained break above 159.85 could open the path towards the 162 high.

However, we also see increasing two way risk. Failure to hold above the 20 day SMA near 159 could trigger a pullback towards 158 and potentially the 157 area. We expect intervention risk to rise materially as the pair approaches 160, and any shift in BoJ rhetoric or narrowing in yield differentials could act as a catalyst for a correction.

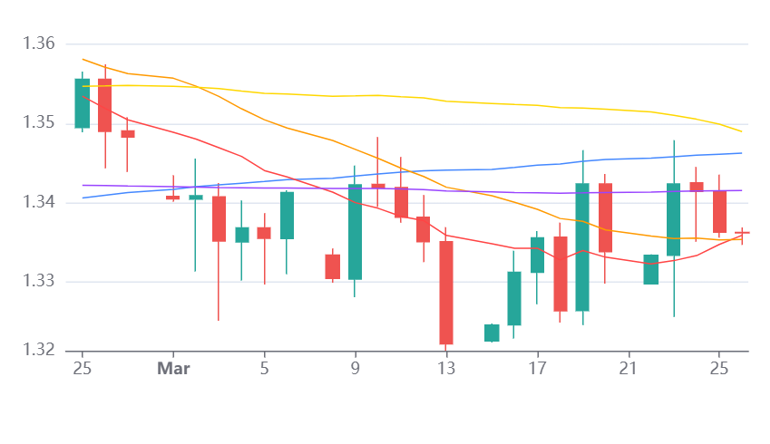

GBP / USD

Source: Massive (polygon.io)

GBP/USD remains under pressure, and we see the pair primarily driven by the interaction between energy driven stagflation risks in the UK and persistent dollar strength. The surge in oil prices linked to the U.S. Israeli conflict with Iran is particularly negative for the UK, given its reliance on imported energy, and we expect this to continue feeding into higher inflation and weaker growth.

This creates a difficult backdrop for the Bank of England. While inflation is already rising, we expect further upside pressure from energy costs, limiting the BoE’s flexibility and reinforcing a stagflationary narrative. At the same time, the dollar continues to benefit from safe haven demand and a more hawkish Fed repricing, with markets expecting rates to remain elevated through 2026.

Technically, GBP/USD is trading near 1.3360 and remains below a key resistance cluster at 1.34, where the 200 day SMA, 20 day SMA and 30 day VWAP converge. The RSI around 47 suggests only a modest recovery in momentum, with the broader structure still bearish.

We expect that failure to reclaim the 1.34 level would keep downside risks in focus, with a move towards the mid March low near 1.3222 likely. More broadly, we see sterling remaining vulnerable in the current environment, with any recovery dependent on a clear de escalation in geopolitical tensions and a stabilisation in energy markets.

Economic Calendar