EUR / USD

The EUR/USD pair faces a macro environment that structurally favours the US dollar, as the severe energy shock from the near-total closure of the Strait of Hormuz hits the eurozone economy harder than the US. While inflation is accelerating on both sides of the Atlantic—US CPI at 3.3% and eurozone inflation expected at 3.0%—the eurozone is simultaneously experiencing economic contraction in its services sector and sharply downgraded growth forecasts, creating a stagflationary backdrop that undermines the euro. The Fed's expected hold at 3.50–3.75% and its prioritisation of inflation containment, reinforced by an anticipated 3.5% PCE reading, keeps US rates elevated and the dollar attractive for yield-seeking capital, while the ECB faces mounting pressure to eventually ease policy given Europe's fragile growth outlook.

From a technical perspective, EUR/USD has edged modestly higher from its 1.168 floor to consolidate near 1.172, sitting precisely above a dense confluence of the 200-day SMA and 20-day SMA clustered around 1.1670–1.1680. Daily RSI near 50 reflects the pair's indecision, with this moving-average cluster representing a critical inflection point that will likely resolve in the direction dictated by the upcoming Fed and ECB meetings on April 28–29 and April 30, respectively. Given the widening fundamental divergence—where the US maintains a hawkish policy stance supported by resilient growth while the eurozone grapples with deteriorating activity—the risk of rejection above this technical zone appears elevated. A failure to break decisively above 1.172 would likely see the pair drift back toward the 1.164 region near the 50-day SMA, with the interest rate differential and relative economic resilience continuing to favour a stronger dollar over the medium term.

USD / JPY

The USD/JPY pair stands at a pivotal technical and fundamental crossroads as the Bank of Japan and Federal Reserve deliver back-to-back policy decisions this week. The BOJ is widely expected to hold rates unchanged, with officials leaning toward delaying a potential hike, while the Fed is set to maintain rates in the 3.50–3.75% range amid persistent inflation concerns amplified by oil prices surging back above $100 per barrel. The substantial interest rate differential between the US and Japan continues to fuel carry trade flows favouring dollar longs, which is flagging a shrinking dollar supply dynamic that could push USD/JPY to test new highs if the BOJ remains dovish.

The broader macro backdrop further tilts the balance against the yen, as Japan's acute vulnerability to energy supply disruptions stemming from the Strait of Hormuz crisis undermines its traditional safe-haven status, while the dollar benefits from both haven demand and resilient US growth, projected at 2.2% annualised for Q1. Technically, USD/JPY has drifted modestly lower to 159.37, sitting just above a critical support at the 20-day SMA of 159.23, with overhead resistance firmly capping rallies near 160.32.

A defence of the 159.16–159.23 support zone on dovish BOJ rhetoric and hawkish Fed signalling would likely spark a rebound toward the 160 handle and a retest of the 160.32 resistance level. However, any unexpected hawkish pivot from the BOJ or a decisive break below the moving average cluster would open the path toward the 50-day SMA near 158.81 and potentially deeper structural support at 157.40.

GBP / USD

The GBP/USD pair enters a critical juncture as it trades at 1.3533, well above key moving averages clustered near 1.3400, following a steady climb that saw the pair break convincingly through the psychologically important 1.3500 level on strong volume. The moderate RSI reading of approximately 58 suggests the pair retains room for further upside toward the 1.3587 resistance established in mid-April, though a failure to sustain momentum at current levels could trigger a retracement toward the 1.3460 support zone.

The fundamental landscape is dominated by an unprecedented convergence of G7 central bank meetings, with both the Federal Reserve and Bank of England expected to hold rates steady amid shared inflationary pressures driven by the Strait of Hormuz oil supply disruption, which has pushed Brent crude above $105 per barrel. US inflation has accelerated to 3.3% while UK food inflation runs at 3.7% with warnings of significantly higher readings, complicating the policy outlook for both institutions and making forward guidance the key variable for near-term direction.

The potential leadership transition at the Federal Reserve from Powell to Warsh introduces an additional layer of uncertainty, as Warsh's plans for reduced forward guidance and balance sheet contraction could catalyse a decisive breakout in the dollar from its nine-month consolidation range, materially altering the GBP/USD trajectory. On balance, the technical picture favours cautious bullish positioning in the near term, but asymmetric energy exposure for sterling ahead of UK local elections on May 7, and the possibility of a hawkish Fed pivot could cap the pair's upside potential.

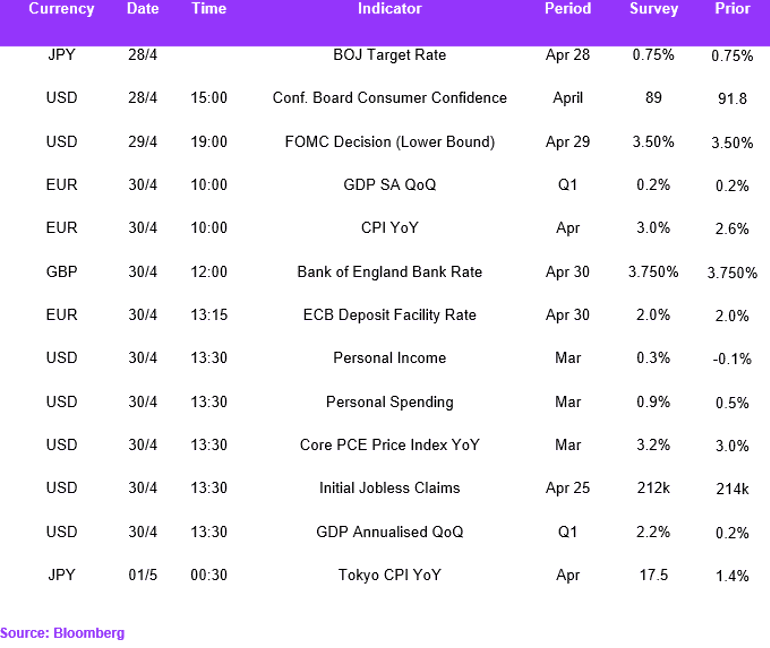

Economic Calendar