EUR / USD

EUR/USD is consolidating in a narrow range around 1.1710, caught between competing macro forces that leave the pair without clear directional conviction. The dollar continues to draw safe-haven demand from the US-Iran conflict and the Strait of Hormuz blockade, while relatively stronger US economic data — including a CB Consumer Confidence reading of 92.8 — further underpins the greenback against a eurozone facing deteriorating growth prospects, with GDP forecasts cut to 0.9% and manufacturing PMIs stuck in contraction.

However, narrowing interest rate differentials are supporting the euro. The ECB is turning more hawkish, with markets pricing in a 72% chance of a June rate hike if inflation broadens, while the Fed is likely to hold at 3.75%, limited by stagflation risks. If the ECB signals a possible June hike and determination to fight inflation, while the Fed remains patient, EUR/USD could rally toward 1.1850–1.1900 as the rate gap narrows, prompting traders to shift from dollar shorts to euro longs.

From a technical standpoint, the pair is trading just above a critical cluster of moving averages near 1.1700–1.1710, with the daily RSI at a neutral 52.6 reflecting the market's indecision. A sustained hold above this support zone could fuel a move toward resistance at 1.1835, while a break below 1.1680 would expose the 1.1615 support area and signal that safe-haven dollar demand and eurozone growth concerns are winning out over rate-differential optimism.

USD / JPY

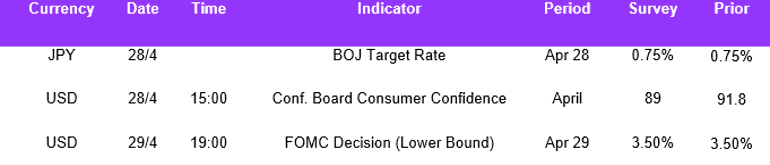

The USD/JPY pair is currently navigating a highly complex macro environment shaped by divergent central bank trajectories and acute geopolitical risks. The Bank of Japan held its benchmark rate steady at 0.75%, but the unusually wide 6-3 vote split under Governor Ueda signals building hawkish momentum, with the overnight swap market now pricing a 65% probability of a June rate hike. Simultaneously, the BoJ's dramatic upward revision of its core inflation forecast to 2.8% — driven in part by surging crude oil prices from the Strait of Hormuz closure — alongside a halved GDP growth projection, creates a stagflationary backdrop that complicates but does not eliminate the normalisation path.

On the other side of the equation, the Federal Reserve is expected to hold rates at 3.50%-3.75%, maintaining a substantial yield differential that continues to underpin carry trade flows and structural dollar demand. However, any dovish acknowledgement of U.S. growth risks at the upcoming Fed meeting could narrow this differential and provide meaningful yen support.

From a technical perspective, USD/JPY is trading near 159.22 in a consolidation phase, sitting just above a critical confluence zone where the 20-day SMA sits at 159.25, with a neutral RSI of 51 reflecting near-term indecision. The pair faces an asymmetric risk profile at current levels, as repeated intervention warnings from Japanese Finance Minister Katayama around the 159-160 zone effectively cap the upside, while a decisive break below 159.00 could open the door toward 158.59 and 157.32 support.

GBP / USD

The GBP/USD pair is trading in a challenging macro environment shaped by the US-Iran conflict, surging oil prices, and diverging central bank outlooks. The closure of the Strait of Hormuz is disproportionately threatening the UK economy as a net energy importer and complicating the Bank of England's policy stance amid sticky inflation and deteriorating growth indicators.

The dollar continues to benefit from safe-haven demand and better-than-expected US consumer confidence data, while the Fed is widely expected to hold rates steady on Wednesday, with markets assigning a 77% probability that rates remain unchanged through year-end. This macro divergence - with the BoE facing growing pressure to ease amid stagflationary conditions while the Fed may acknowledge upside inflation risks from the energy shock - is tilting the fundamental backdrop against sterling.

Technically, the pair settled near 1.3518 after fully retracing a sharp midweek dip to 1.3464, holding above the key 20-day SMA at 1.3441, with the daily RSI at 56 remaining modestly constructive. Institutional positioning has shifted cautiously bearish on sterling, with declining speculative net longs and a slight premium for puts in options markets, suggesting that while the 1.3500 support zone may hold near-term, the fundamental risks from elevated energy prices and geopolitical uncertainty leave the pound vulnerable to a deeper move toward 1.3407 should the macro backdrop deteriorate further.

Economic Calendar