EUR / USD

EUR/USD slipped approximately 0.3% to the 1.1676 area following the decision, falling just beneath the confluence of its 100-day SMA, 20-day SMA clustered near 1.17—a technically significant development that reflects fading momentum and persistent selling pressure. The hawkish undertones from the Fed, combined with markets now pricing in as much as a 25% chance of a rate hike over the next year rather than any easing, have reinforced near-term dollar strength, with the DXY rising 0.4% to 98.95.

The Federal Reserve's decision to hold rates steady at 3.50–3.75% in an 8-4 vote—the most divided since 1992—underscores deep internal disagreement about the policy path forward, with three members dissenting against retaining an easing bias and one preferring a cut. Chair Powell, in what was likely his final meeting before Kevin Warsh's expected succession, cited elevated inflation driven by surging energy costs and high economic uncertainty stemming from the Middle East conflict, characterizing the current stance as at the high end of neutral or mildly restrictive and signalling no imminent rate cuts.

However, the medium-term picture is more nuanced: the narrowing of US-German 2-year yield spreads from roughly 200 basis points a year ago to approximately 118 currently remains a structural support for the euro, particularly as the ECB pivots hawkish with three full rate hikes now priced in by year-end in response to energy-driven inflation expected to push eurozone CPI toward 3.0%. The forthcoming ECB decision is crucial. While the ECB is expected to mirror the Fed by keeping rates unchanged, a shift towards a more hawkish tone could reverse the euro's recent losses, prompting markets to reassess and price in a more aggressive tightening stance among major central banks.

USD / JPY

The USD/JPY pair has breached the critical 160.00 level, climbing to 160.35 and approaching the 2024 all-time high near 162, driven by a powerful confluence of monetary policy divergence, energy market disruption, and extreme speculative positioning. The Federal Reserve held rates steady at 3.5%-3.75% in what was Jerome Powell's final meeting as chair, with Powell characterizing the current rate as at the "high end of neutral or perhaps mildly restrictive" and emphasizing the Fed can afford to wait before acting — rhetoric that reinforced dollar strength by eliminating expectations for rate cuts and even pricing a 25% probability of a hike within the next year. The deeply divided 8-to-4 FOMC vote, the most split since 1992, suggests that incoming chair Kevin Warsh will inherit an institution with hawkish internal pressure that could keep U.S. rates elevated for longer.

The widening policy divergence with the Bank of Japan, which held rates unchanged at 0.75% while citing Middle East uncertainty, sustains the extraordinary yield differential that continues to fuel the carry trade punishing the yen. Surging oil prices above $110 per barrel compound the yen's structural vulnerability given Japan's near-total energy import dependence, widening the trade deficit and adding imported inflation pressures that the BoJ appears reluctant to combat aggressively.

Technically, the pair trades well above its layered moving average support — with the 20-day SMA, 50-day SMA all clustered near 159.25 — providing a cushion for bulls targeting 162, though speculative short-yen positioning at multi-year extremes and Japan's explicit readiness to intervene at the 160 red line introduce the risk of sharp but historically temporary reversals should authorities act.

GBP / USD

The monetary policy divergence between the Federal Reserve and the Bank of England remains the dominant driver for GBP/USD. The Fed's decision to hold rates steady for a third consecutive meeting, with Chair Powell signalling comfort at the high end of neutral or mildly restrictive territory, reinforces the higher-for-longer narrative that has broadly supported the US dollar.

Nonetheless, today's meeting could highlight that this narrative is particularly relevant for economies heavily reliant on energy imports. With oil prices surging above $100 per barrel, the UK—being a net energy importer—faces increased pressure from rising costs, which in turn amplifies inflationary forces. The interplay of diverging growth prospect and persistently high energy prices has created a backdrop that supports a more volatile yet marginally resilient GBP/USD outlook in the short term.

From a technical perspective, GBP/USD declined roughly 0.33% over the past 24 hours to 1.3474, now sitting at the clustered 200-day and 50-day simple moving averages near 1.34 with a neutral RSI around 51.5, suggesting the pair is at a critical inflection point. While the BOE is expected to mirror the Fed by keeping rates unchanged, a shift towards a more hawkish tone could lift the pound, prompting markets to reassess and price in a more aggressive tightening stance among major central banks.

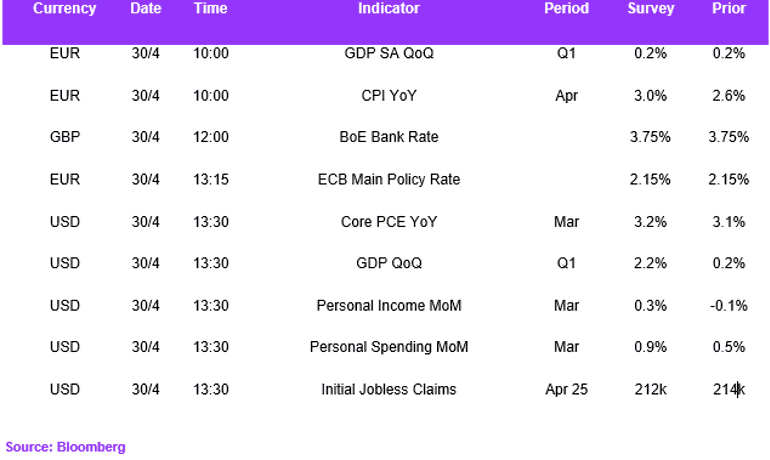

Economic Calendar