EUR / USD

The EUR/GBP pair remains under bearish pressure ahead of the upcoming ECB decision, trading near 0.8661 with the RSI close to 40 and price holding firmly below the clustered moving averages around 0.8700. We see the fundamental backdrop shaped by a clear divergence between a fragile Eurozone economy, where growth projections have been revised down to around 0.9%, and a comparatively more resilient UK economy, supported by a gradually improving labour market and unemployment trending towards 4.9%.

We expect the European Central Bank to hold rates at 2.00%, although its policy outlook is complicated by the energy shock linked to disruption around the Strait of Hormuz, which has lifted oil prices above $100 per barrel and introduced a stagflationary impulse that weighs more heavily on the Eurozone due to its reliance on imported energy. We see the key question as whether the ECB adopts a more hawkish tone in response to rising energy costs feeding into inflation, or whether it prioritises growth concerns amid weak German industrial output and softer services PMI readings. In contrast, we expect the Bank of England to maintain its firmer stance, holding rates at 3.75% as UK inflation remains elevated near 4%, reinforcing a meaningful rate differential in favour of sterling.

We see this policy divergence and associated carry advantage continuing to weigh on EUR/GBP unless the ECB delivers a distinctly hawkish signal. Technical consolidation and narrowing Bollinger Bands point to an imminent breakout. We expect a move below 0.8640 to expose the monthly low near 0.8617, while any euro supportive surprise would need to clear strong resistance around the 0.8700 area to alter the broader bearish trend.

USD / JPY

USD/JPY remains caught between intervention efforts from Japanese authorities and persistent underlying drivers that favour dollar strength. Officials reportedly deployed close to $35 billion in yen purchases on 30 April, triggering a sharp rally of around 3%, with Finance Minister Shunichi Katayama warning against speculative activity and signalling that further intervention during Golden Week remains possible. However, we see these measures as establishing a temporary ceiling rather than driving sustained yen appreciation, given the wide yield gap between steady US rates and the Bank of Japan policy rate of 0.75%.

We expect the macro backdrop to continue reinforcing yen weakness, as elevated oil prices above $100 per barrel both support the dollar through safe haven demand and increase Japan’s energy import burden. Technically, USD/JPY is trading near 157.24 with the RSI around 39, signalling bearish momentum, while price remains below key resistance formed by the 20 day SMA, 30 day VWAP and 50 day SMA near 159. We see the 156 level as critical support, with a break lower likely to accelerate declines towards the 200 day SMA near 155.50, while a successful defence could prompt a rebound back towards 159.

GBP / USD

GBP/USD is under near term pressure, declining around 0.5% over the past 24 hours to trade near 1.3522, as renewed geopolitical tensions in the Middle East, particularly exchanges between US and Iranian forces near the Strait of Hormuz, have driven safe haven flows into the dollar and weighed on sterling. The surge in Brent crude above $114 per barrel presents a clear headwind for the UK as a net oil importer, raising stagflation concerns even as the Bank of England maintains a relatively hawkish stance with rates at 3.75% and inflation around 3.3%.

From a technical standpoint, we see the pair slipping below the 20 day SMA near 1.3500, with RSI easing towards 53 and signalling a loss of short term momentum, although price continues to find support above the confluence of the 30 day VWAP near 1.3500 and the 50 day and 200 day SMAs around 1.3400. Selling pressure intensified through the afternoon session, with price action skewed towards earlier highs, reinforcing a sustained intraday bearish bias.

Looking ahead, we see two competing forces shaping direction. We expect the Bank of England’s relatively firm stance and the modest gilt yield advantage, with UK ten year yields near 5% compared to US ten year yields around 4.44%, to offer underlying support for sterling. However, we also see the dollar’s safe haven appeal and rising energy driven inflation risks maintaining downside pressure should Middle East tensions escalate further. We expect a hold above the 1.3500 level to allow a recovery towards 1.3620, while a decisive break below 1.3510 would likely open the way towards the 1.3400 moving average cluster, particularly if oil prices continue to rise and risk sentiment deteriorates.

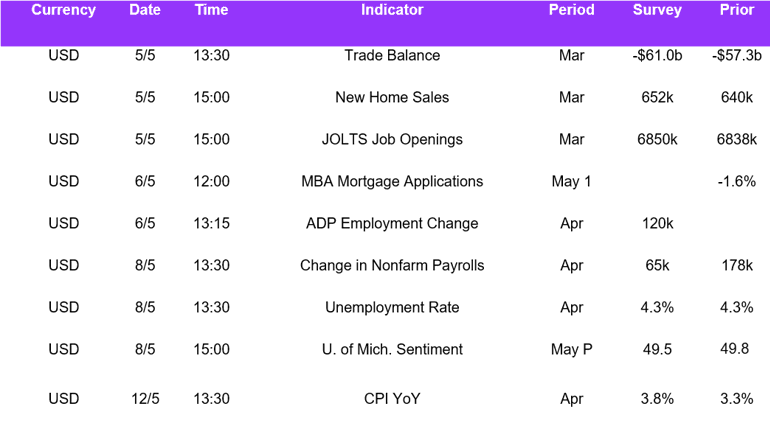

Economic Calendar