EUR / USD

EUR/USD enters the week trading with strengthening bullish momentum, having rallied approximately 0.47% to close near 1.1787 on May 8, firmly above all major moving averages including the 200-day SMA at 1.1682. The pair's technical positioning suggests continued upside potential, with a decisive break above the 1.1800 resistance level potentially opening a path toward January highs near 1.2040, though rejection at that level could trigger a pullback toward the clustered support zone around 1.1700–1.1720.

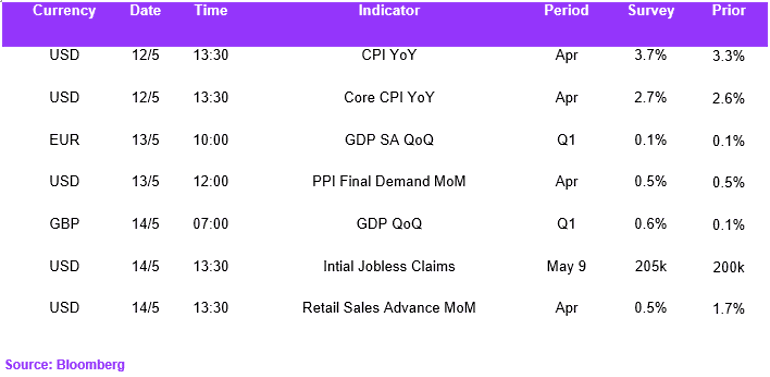

The fundamental trajectory this week hinges primarily on the U.S. April CPI report on Tuesday, expected at 3.7% year-over-year for headline, which captures a full month of elevated energy costs from the Strait of Hormuz disruption and crude oil above $95 per barrel. The hawkish repricing in U.S. rate markets—with markets pushing expected Fed cuts to late 2026 and swaps embedding a one-in-three probability of a rate hike—could either support the dollar if CPI surprises higher or trigger a corrective dollar selloff if inflation comes in softer than feared.

The ECB faces its own policy tension as Eurozone CPI, forecast at 2.9%, reflects the energy shock's inflationary impulse while structural growth weakness in Germany argues for accommodation, creating a less clearly hawkish narrative than the Fed's predicament. The convergence of the incoming Fed Chair Warsh's formal transition on May 15, ECB President Lagarde's Wednesday speech, and the Trump-Xi summit creates an unusually event-rich environment where EUR/USD direction will likely be determined by relative inflation surprises and any shifts in geopolitical risk sentiment.

USD / JPY

The USD/JPY pair is navigating a complex environment defined by the substantial 275-300 basis point interest rate differential between the Federal Reserve and the Bank of Japan, which continues to exert structural downward pressure on the yen despite Japan's Ministry of Finance deploying approximately $64 billion in intervention after the pair breached 160. The BOJ's reluctance to normalize rates more aggressively — holding steady at 0.75% on a 6-3 vote — leaves the fundamental driver of yen weakness largely unresolved, a view echoed by market practitioners who view any intervention-driven yen strength as potentially short-lived.

From a technical perspective, the pair has retreated to approximately 156.67, trading below its 20-day and 50-day levels while the daily RSI at 38 confirms sustained bearish momentum following the sharp selloff from the 160.65 highs. The 156 level now represents the most critical support level, with a decisive break below potentially accelerating selling toward 155.

Looking ahead, the trajectory will likely be shaped by the May 12 US CPI release — where a hotter-than-expected 3.7% year-over-year print could reinvigorate dollar strength by dampening Fed rate cut expectations — alongside the broader unwinding of the geopolitical safe-haven premium that had previously supported the greenback. The pair remains caught between intervention-enforced resistance near 160 and technical support at 156, with the fundamental rate differential suggesting any yen strength will be difficult to sustain absent a meaningful shift in BOJ policy.

GBP / USD

GBP/USD has rallied approximately 0.6% over recent sessions to trade near 1.3634, positioned well above all key moving averages including the 200-day and 50-day SMAs near 1.34, with the daily RSI at roughly 61 reflecting sustained bullish momentum without reaching overbought territory. The stacked moving average alignment supports a potential push toward the January 2026 peak around 1.3848 if the pair can clear resistance near 1.3637.

However, the macroeconomic backdrop presents significant headwinds for sterling. Tuesday's US CPI release is expected to show headline inflation at 3.7% year-on-year—the highest since 2023—driven by energy costs from the Strait of Hormuz disruption, which has already shifted market expectations decisively away from Fed rate cuts and toward a possible hike. The incoming Fed Chair Kevin Warsh's hawkish reputation, combined with last week's stronger-than-expected US payrolls report, further reinforces the rate differential favouring the dollar.

On the UK side, Thursday's GDP report forecast at 0.2% quarter-on-quarter will be pivotal in shaping Bank of England rate expectations, with weak figures potentially intensifying dovish repricing and weighing on sterling. While the current technical picture favours the bulls, the fundamental divergence between persistent US inflation supporting prolonged higher rates and uncertain UK growth prospects suggests that absent a geopolitical breakthrough on Iran or a significant CPI miss, the pair's upside may face increasing resistance as dollar-supportive forces reassert themselves.

Economic Calendar