EUR / USD

Source: Massive (polygon.io)

The EUR/USD pair bounced back on the back of dollar weakness, from depressed levels near 1.1380 to approximately 1.1423, with RSI climbing from 31 to 38.6—a notable momentum shift suggesting oversold conditions are unwinding. Fundamentally, however, the pair remains under significant structural pressure driven by widening transatlantic policy divergence, with the Federal Reserve's hawkish pivot toward potential rate hikes contrasting sharply with the ECB's constrained tightening capacity amid a downgraded 2026 Eurozone growth forecast of just 0.8%.

Markets are pricing approximately 60% odds of Fed tightening by September while expecting only 28 basis points of additional ECB hikes by year-end, a differential that fundamentally favours sustained dollar strength. The partial de-escalation of US-Iran tensions following the weekend ceasefire agreement has provided modest euro relief by easing energy import cost fears for the Eurozone, though this geopolitical risk remains a latent binary catalyst for the pair.

From a technical perspective, the pair trades meaningfully below all major moving averages, with the 20-day SMA at 1.1494, the 50-day at 1.1606, and the 200-day at 1.1658 all representing formidable overhead resistance that underscores the entrenched bearish trend.

The upside surprise in Eurozone economic confidence at 95.0 offers only marginal support against the weight of superior US economic momentum, where PCE inflation at 4.1% and consistently strong payrolls reinforce the hawkish Fed narrative. Thursday's US employment report represents the key near-term catalyst, with any upside surprise likely to reignite dollar strength and push EUR/USD back toward its recent low near 1.1330.

USD / JPY

Source: Massive (polygon.io)

The Japanese yen has depreciated to its weakest level against the US dollar since December 1986, trading near 161.96 as persistent monetary policy divergence between the Federal Reserve and the Bank of Japan continues to dominate price action. The interest rate differential remains the primary driver, with Fed funds futures pricing a 64% probability of another rate hike by September while markets see virtually no chance of an additional BOJ move at its July 31 meeting, despite the BOJ having raised its benchmark rate to 1% in June.

From a technical perspective, USD/JPY has advanced steadily to print a fresh high near 161.98, sitting just below the all-time peak of 162.00 set in July 2024, with the pair trading well above all key moving averages—including the 200-day SMA at 156.61—while the daily RSI at 76 signals elevated overbought momentum. A decisive break above the 162 level could trigger stop-driven buying into uncharted territory, potentially accelerating toward 162.50, though overbought conditions raise the risk of profit-taking back toward the 20-day SMA near 160.90.

The primary constraint on further yen weakness remains intervention risk, as Japanese Finance Minister Katayama has stated authorities are ready to take "bold action" against excessive speculative moves, though Japan's record intervention of approximately $72.5 billion between late April and late May ultimately failed to reverse the depreciation trend. Structural headwinds for the yen persist, including Japan's aging population, ballooning public debt, and deeply entrenched carry trade positioning at extremes not seen since 2024, all of which reinforce the bearish yen trajectory while simultaneously creating vulnerability to a sharp unwind should conditions shift.

GBP / USD

Source: Massive (polygon.io)

The GBP/USD pair staged a 0.4% recovery from its Sunday open near 1.3199 to settle around 1.3252. The Bank of England's decision to hold rates at 3.75% with limited hawkish dissent, combined with moderating UK inflation at 2.8% and softening economic activity, limits interest-rate support for the pound. Political uncertainty surrounding potential leadership changes and fiscal policy direction is adding a meaningful risk premium to sterling, keeping investors cautious despite intermittent reassurances of fiscal discipline.

On the technical front, the pair remains well below all key moving averages, with the 200-day and 50-day SMAs converging near 1.34 and the 20-day SMA sitting around 1.33, confirming that the broader downtrend from the January highs near 1.3850 remains intact. The Federal Reserve's hold at 3.50–3.75% amid rising Core PCE at 3.4% reinforces expectations of elevated US rates for longer, with upcoming non-farm payrolls data posing a further risk to sterling if labour market resilience is confirmed.

Until UK economic data improves materially or the political landscape stabilizes, the diminishing interest rate differential and overhead technical resistance near 1.33 suggest the macro and technical backdrop continues to favour dollar strength, with downside risk toward the three-month low around 1.3147 remaining the path of least resistance.

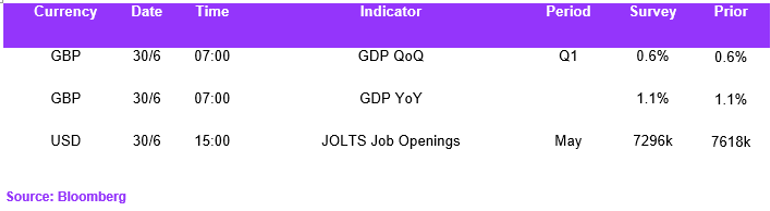

Economic Calendar