EUR/USD 2026 Outlook

The December FOMC as the Final Macro Catalyst

EUR/USD enters the final stretch of 2025 with markets almost entirely focused on the Federal Reserve, and it is difficult to see any other factor dominating the pair before year-end. The next FOMC meeting, coming after an unusually long gap in official data releases due to the prolonged government shutdown, represents the final major macro event of the year and therefore the central driver of the dollar. The Fed has repeatedly emphasised its data-dependent approach, but this December meeting is unique in that policymakers must decide without several of the inputs they usually consider essential.

September’s PCE and payrolls remain the last complete dataset available, which forces the Committee to rely more heavily on private indicators such as the ADP Employment Report and high-frequency inflation trackers. This lack of clarity is itself a source of volatility for the dollar, as the more uncertain policymakers remain, the more reactive the greenback tends to be to even small shifts in expectations.

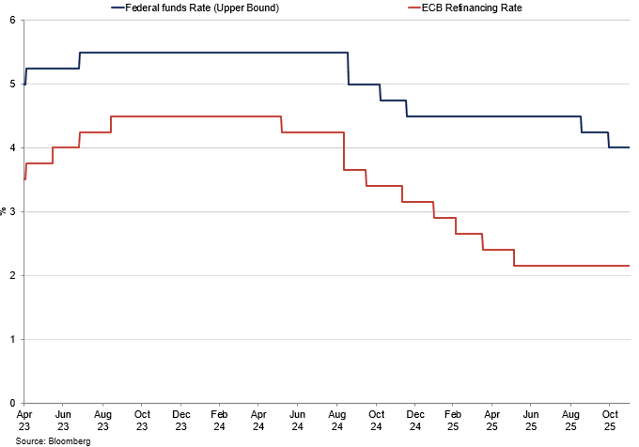

Interest Rates (%)

The difference in monetary policy remains the main driver for EURUSD.

Internal Divisions and a Cautious Cut

The political dynamics inside the FOMC are no less important. Reports suggest the meeting could see several dissents, with up to five voting members either opposed to further easing or sceptical of the wisdom of cutting again before full data resumes. At the same time, a dovish core inside the Board of Governors is firmly in favour of reducing rates, creating the possibility of a contested decision regardless of the outcome.

From a market-behaviour perspective, the Fed seldom chooses to move sharply against expectations this late in the year, and with futures currently pricing an almost unanimous likelihood of a 25bps cut, we believe the Committee will ultimately align with this view. Yet the absence of data gives the Fed a strong incentive to stress caution, and the most likely messaging is that while a December cut is justified, the bar for another early in 2026 remains high.

For EUR/USD, this should mean a modest downward drift in the dollar into the final days of the year, tempered by language that tries to prevent markets from pricing in a January follow-up move. In other words, we expect the Fed to validate the December easing while simultaneously keeping the probability of immediate further cuts low — a combination that tends to weaken the dollar mildly without triggering a larger USD sell-off.

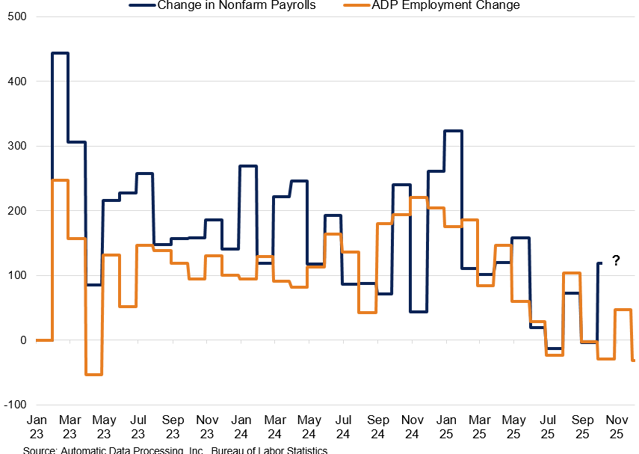

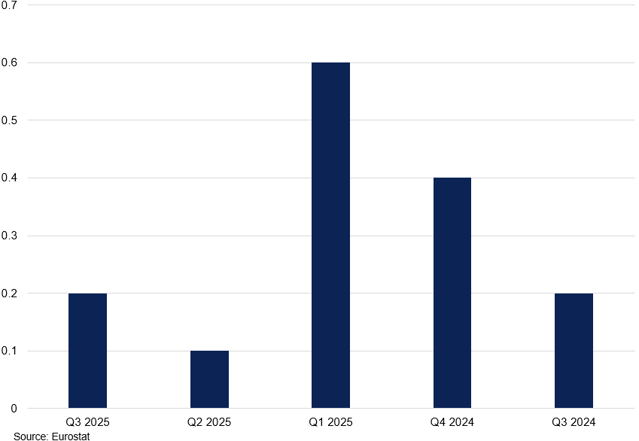

US labour market (k)

While available data point to a mild softness in the labour market, the real picture remains unclear.

Entering 2026 with Divergent Rate Paths

As we transition into 2026, the narrative around EUR/USD continues to revolve primarily around the Fed rather than the ECB. Markets are currently assuming between 50 and 75 bps of additional US cuts next year, while the ECB is widely believed to be at or near the end of its own easing cycle. This asymmetry implies a slow erosion of the dollar’s rate advantage and a gentle upward pressure on EUR/USD, but what truly matters for next year is how expectations evolve rather than the levels themselves.

If incoming data in early 2026 highlights a slower disinflation path or reveals resilience in the labour market, the Fed may struggle to deliver the easing profile that is currently priced. Inflation in the US is still largely driven by services, shelter components, and tariff-sensitive goods categories, each of which can exhibit stickiness independent of broader economic conditions. At the same time, the labour market remains reasonably firm, with wage growth only gradually softening.

Should this situation persist, the Fed may find itself inclined to keep policy restrictive for longer, and the dollar would likely respond with renewed strength as front-end US yields reprice higher relative to their euro-area equivalents.

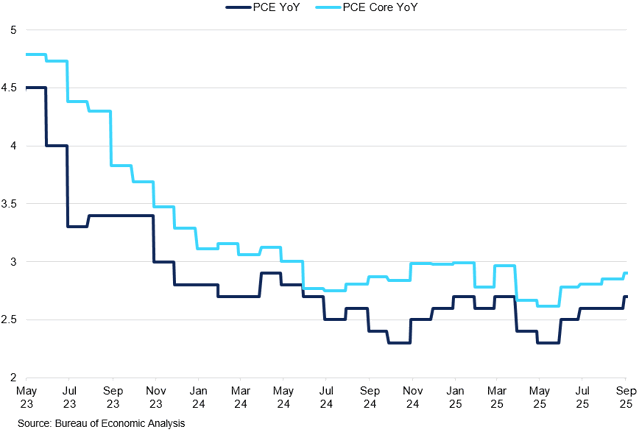

Us inflation (%)

Available data show inflation diverging higher from the Fed’s 2% target.

The Fed Chair Transition as a Core Dollar Risk

Another source of uncertainty comes from the upcoming change at the top of the Fed. Jerome Powell’s term as Chair ends in May 2026, and while his position as Governor continues until 2028, the decision on his successor lies entirely with the White House. Under a second Trump administration, the appointment is likely to become one of the single most important macro events of the year for the dollar.

Rumours currently point to Kevin Hassett as the leading candidate, a figure widely considered more loyal to the administration and more willing to endorse an easier policy stance. Markets have begun to discuss the possibility that Hassett, or someone with a similar profile, would favour earlier or deeper easing than Powell, which could weigh meaningfully on the dollar if confirmed. Yet the dynamic is not one-directional.

If Trump settles on someone perceived as more institutionally cautious or more committed to the Fed’s independence than expected, investors may take this as a reassurance that policy will not become overtly politicised. That sort of appointment would likely bring the dollar relief, particularly in longer-dated rates, just as a more explicitly dovish selection would do the opposite. For most of 2026, the confirmation process itself may generate volatility as investors react to informal signalling from the White House. Each episode of uncertainty will tend to weaken the dollar, whereas breakthroughs in clarity would likely support it.

Politics, Fiscal Expectations, and the Midterms

Overlaying monetary policy is the political cycle, with the midterm elections set to dominate the second half of 2026. Historically, the president’s party tends to lose seats, and early surveys suggest Democrats currently appear more energised than Republicans, though election dynamics can shift significantly once primaries begin.

Because Republicans already control both chambers, the midterms are less about a fiscal shift driven by a Republican sweep and more about whether Trump loses part of the congressional backing he currently enjoys. If Republicans simply retain both chambers, the market impact on the dollar should be limited, as investors would treat this as a continuation of the existing fiscal and legislative environment.

By contrast, if Democrats were to flip either the House or the Senate, markets would likely price a reduced probability of further tax cuts and a tighter constraint on Trump’s fiscal agenda. That would lower expectations for Treasury issuance, push yields modestly lower, and soften the dollar at the margin. In effect, the dollar’s 2026 political risk centres not on Republicans keeping control, but on the possibility that they lose it.

Europe’s Structural Pressure Points

On the euro side, the narrative shifts away from interest rates and towards the sense of strain that has been building in the region. The conflict in Ukraine remains deeply entrenched, and there is little reason to believe a durable resolution is imminent. Even in a hypothetical scenario where peace discussions progress, the structure of any agreement is likely to leave Europe with long-term security risks and budgetary pressures. From a currency-market standpoint, the Ukraine outlook is rarely a source of euro strength. At best it removes a tail risk, and at worst it reinforces the perception of Europe as the region bearing the highest geopolitical burden.

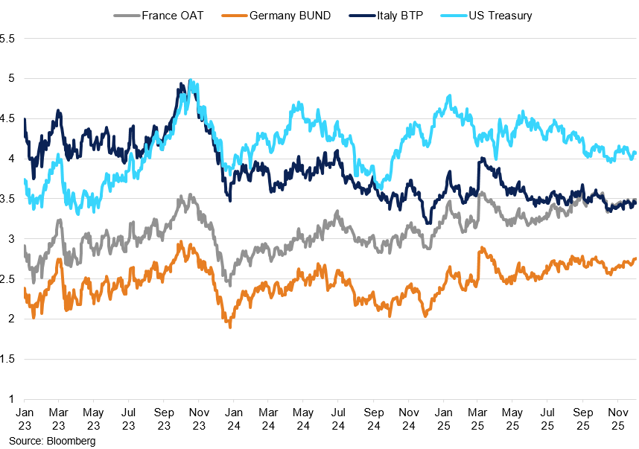

10-Year Government Bond Yields (%)

Persistent yield premium on US Treasuries relative to German Bunds, OATs and BTPs, highlights the disconnect between rates and recent euro strength.

France and the Fragility of Euro-Area Cohesion

France adds its own layer of complication. With a deficit of 5.8% of GDP in 2024 and public debt at 113% of GDP, Paris now sits just behind Italy and Greece in the euro area’s fiscal hierarchy. The European Commission’s decision to place France under the Excessive Deficit Procedure highlights the severity of the challenge. Although France has until 2029 to address its imbalance, markets increasingly doubt whether meaningful consolidation is achievable under current political conditions. Any widening of the OAT–Bund spread would raise questions not only about France but about broader euro-area cohesion, a theme that has historically weighed on EUR/USD during risk-off periods. For now, the situation remains contained. The ECB’s caution on further rate cuts and the relative stability of euro-area sovereign spreads help reduce immediate pressure on the euro. However, the structural risk persists beneath the surface and represents a clear vulnerability for the currency in 2026 if sentiment turns.

Eurozone GDP Growth YoY (%)

GDP growth has softened in recent quarters.

A Soft Growth Environment

The missing piece in the euro discussion is, of course, growth. Eurozone GDP remains weak by historical standards, with the region struggling to rebuild momentum after several years of subdued activity. Ordinarily, such a backdrop would be a clear headwind for the euro. Yet foreign exchange markets tend to respond more forcefully to relative interest-rate expectations than to absolute growth levels, and the ECB’s earlier easing means that much of Europe’s underperformance is already embedded in the currency. In contrast, US growth has remained resilient enough to delay the Fed’s exit from restrictive policy, but this resilience sits atop an increasingly strained fiscal foundation. Markets understand the US faces another debt-ceiling confrontation at the end of January, alongside a deficit profile that deteriorates further under current policy assumptions. These dynamics complicate the usual narrative whereby stronger US growth automatically translates into a stronger dollar, and they help explain why EUR/USD can rise even when the Eurozone is expanding more slowly.

2026 Outlook: Base Scenario

Taking these elements together, our central expectation is that EUR/USD drifts upward over the course of 2026, benefiting from a slow weakening of the dollar as the Fed proceeds with a gradual easing cycle. We think the December cut, likely delivered despite internal dissent, sets the tone for a cautious, data-dependent Fed that trims policy rates twice more next year. Meanwhile, the ECB remains broadly on hold, leaving most of the adjustment to come from the US side. Under this base scenario, we see the pair appreciating steadily, though not dramatically, supported by a narrowing yield differential yet constrained by persistent European political risks.

2026 Outlook: Dollar Weakness

A more pronounced euro-positive outcome would require the US labour market to deteriorate more sharply than we currently expect, allowing the Fed to deliver more than the 75bps priced into markets. A clean disinflation trend, free from tariff distortions, combined with the appointment of a distinctly dovish Fed Chair, could push US real yields lower and weaken the dollar more decisively. Europe would simply need to avoid new shocks for that move to gain traction. In such circumstances, EUR/USD could appreciate materially, supported by broad-based dollar softness.

2026 Outlook: Dollar Strength

The euro-negative scenario emerges if the US data hold up more firmly than expected and inflation proves slow to retreat, leaving the Fed with little reason to extend its easing cycle beyond December. In that setting, even a modest resurgence in price pressures, could prompt policymakers to lean more heavily on a “higher for longer” message. A Chair who signals a preference for tighter policy, or a confirmation process that reassures investors about the Fed’s resolve, would likely push US yields higher and draw renewed support for the dollar. If this coincides with fresh doubts over France’s fiscal trajectory or a broader return of euro-area fragmentation concerns, the euro would struggle to hold recent gains. Under such conditions, EUR/USD could fall back significantly, and talk of parity would probably re-emerge in any period of market stress.