GBP/USD

Sterling enters H2 2026 with domestic fundamentals becoming less supportive. Growth has lost momentum, political leadership is changing, and investors are awaiting greater clarity on fiscal policy ahead of the Autumn Budget. With the BoE constrained by inflation and the Fed expected to remain relatively hawkish, does GBP/USD have enough support to move higher, or are risks skewed towards dollar strength over the coming months?

GBP Analysis

UK Politics

Keir Starmer resigned on 22 June 2026, after less than two years in office. Andy Burnham, former Greater Manchester mayor and now MP for Makerfield, is the only declared Labour leadership candidate and could be confirmed as party leader on 17 July, with appointment as Prime Minister shortly afterwards if he remains unopposed. For markets, the transition has so far been orderly. Gilt yields showed little reaction to Starmer's departure, suggesting investors do not currently view the leadership change as a material threat to fiscal policy.

Markets are likely to focus more closely on the new government once Burnham finalises his cabinet and sets out policy ahead of the Autumn Budget. His platform is generally viewed as more interventionist than Starmer's, although he has pledged to maintain the fiscal rules and avoid increases in the main rates of income tax, VAT and National Insurance.

For GBP/USD, the key questions are therefore who controls economic policy after July and whether the Autumn Budget delivers a credible fiscal plan. Until then, politics is likely to influence market sentiment at the margin, with GBP/USD taking clearer direction from growth, inflation and relative rate expectations.

GBP/USD vs UK-US Composite PMI differential

UK growth momentum has softened relative to the US, leaving GBP/USD with limited support from the macro side.

Source: FRED, S&P Global

UK Growth

The UK economy entered 2026 on a firmer footing, with Q1 GDP growth unrevised at 0.6% QoQ, supported by services, government spending and a recovery in household consumption. However, that strength did not translate into higher living standards. Real disposable income per capita fell 0.8% over the quarter as taxes and inflation continued to weigh on households.

More recent data suggest the pace of growth has eased. The flash June composite PMI fell to 49.4, signalling a second consecutive month of private sector contraction, while services activity weakened to its lowest level since early 2021. Labour market indicators have also softened, with PAYE employment declining, vacancies falling to their lowest level since 2021 and real wage growth broadly flat.

Taken together, the data suggest the economy has lost momentum following a stronger first quarter. While activity remains above recessionary levels, recent survey and labour market data point to a softer growth profile through the second half of 2026. The OBR expects GDP growth of 1.1% this year, though achieving that forecast will likely require an improvement in private sector activity from current levels.

For GBP/USD, weaker activity data are unlikely to provide support for sterling. A softer UK growth profile reduces the relative attractiveness of the UK economy and leaves GBP increasingly reliant on the rates story for direction.

GBP/USD vs Inverted DXY

While broad dollar direction remains the dominant driver of GBP/USD, sterling has struggled to fully participate in periods of dollar weakness.

Source: FRED

BoE expectations

The Bank of England left Bank Rate unchanged at 3.75% in June in a 7–2 vote, with two members favouring a 25bp increase. While CPI eased to 2.8% in May, the MPC expects inflation to move higher again over the second half of the year as earlier energy price increases feed through, with CPI projected to rise above 3% by Q4. June minutes also highlighted a sharp repricing in short-dated UK rates following the escalation of tensions in the Middle East, as markets pared expectations for policy easing and pushed rate expectations higher into year-end.

We expect the BoE to leave policy unchanged at the 30 July meeting, with the hurdle for rate cuts remaining high while inflation is projected to reaccelerate and policymakers remain concerned about underlying price pressures. Although growth and labour market indicators have softened, we do not see sufficient evidence for an easing cycle to begin in H2 2026. Risks remain tilted towards rates staying higher for longer, particularly if higher energy costs feed into wages and services inflation. While a further hike is not our base case, it cannot be ruled out should inflation prove more persistent than currently expected.

Relative rate differentials remain more supportive of the dollar than sterling, with markets pricing around two further Fed hikes against roughly one additional BoE increase. Our central view is less hawkish than current pricing, with the Fed delivering no more than one hike and the BoE remaining on hold. As a result, we see limited scope for sterling to gain through the rates channel alone.

UK CPI Headline vs Core

Inflation remains above target despite recent moderation.

Source: Office for National Statistics

USD Analysis

US Midterms

The 2026 US midterms, scheduled for November 3, will set the balance of power in Congress for the remainder of President Trump’s second term. The full House will be up for election, alongside 35 Senate races — 33 regular contests and two special elections in Florida and Ohio following Senate vacancies. At this stage, Republicans hold narrow majorities in both chambers, with around 218 House seats versus Democrats’ 212 and 53 Senate seats versus Democrats’ 45. That means Democrats only need a small net gain to reclaim the House, but the Senate remains the harder path, as they are defending more seats and need four net gains to flip control.

That starting point matters because midterms typically become a referendum on the sitting president, and given the historical precedent, the incumbent party usually loses seats. Since WWII, the president’s party has lost around 26 House seats and 4 Senate seats on average. With Trump’s approval in the low 40s and Democrats leading by around 3–5 points on the generic ballot, the backdrop looks challenging for Republicans, particularly in suburban swing districts. Still, the Senate map is less favourable to Democrats because many contested seats sit in Trump-leaning states. We therefore believe the most likely outcome is a split decision: Democrats gain the House while Republicans retain the Senate. A full Democratic sweep is plausible but harder, while a GOP hold of both chambers would likely require stronger economic momentum, improved approval ratings, or weaker Democratic turnout.

US Midterm Scenarios: Market Implications

|

Scenario |

Probability |

Control |

Fiscal / Shutdown Risk |

USD / Rates Reaction |

|

1. Divided Congress |

~40–45% |

Dem House; GOP Senate |

Gridlock: little new fiscal policy. Shutdown risk: elevated. |

USD: little changed / slightly softer if expected; volatility possible. Yields: slight downward bias as fiscal risk eases. |

|

2. Democratic Sweep |

~25–30% |

Democrats flip both chambers |

Constrained: Trump veto limits policy change. Shutdown risk: moderate. |

USD: risk-off bounce if surprise; then mild weakening as deficit risk fades. Yields: downward pressure on long rates. |

|

3. GOP Holds Both |

~20% |

Republicans retain both chambers |

Active fiscal agenda: tax cuts / targeted spending possible. Shutdown risk: low-moderate. |

USD: mixed but supported if fiscal easing lifts yields. Yields: upward pressure, mainly long-end. |

Source: Sucden Financial

For markets, the cleaner transmission is still the fiscal channel. A divided Congress would imply gridlock, fewer major fiscal initiatives, and a higher risk of funding standoffs or shutdowns. That should modestly reduce deficit and stimulus expectations, putting some downward pressure on long-end yields and limiting USD upside. A Democratic sweep would still be constrained by Trump’s veto power, but it could increase headline political noise, creating short-term risk-off support for the dollar before markets refocus on gridlock. By contrast, a GOP hold of both chambers would be the more USD-supportive scenario if investors price renewed tax cuts or targeted spending, higher deficits, and firmer growth or inflation expectations.

History also suggests that any USD reaction is likely to be short-lived and context-dependent. Election risk premia tend to build months in advance, with volatility peaking just before the vote and fading once results become clear. In 2018, the dollar reaction was muted because the divided-government outcome was largely expected. In 2022, USD moves were dominated by inflation, Fed tightening, and global risk sentiment rather than the election itself. The same is likely in 2026: midterms may create pockets of volatility, but sustained USD direction should still depend more on Fed policy, inflation, growth, and broader risk appetite.

Dollar Volatility Around Previous Midterms

USD volatility has typically risen into midterm results, particularly when control of the House or Senate remained uncertain.

Source: FRED

US Growth

We believe macro will set the scene for most USD moves into year-end. Inflation is still elevated, with headline CPI around 4.2% YoY in May, partly driven by energy shocks linked to the conflict involving Iran, while core CPI is closer to 2.9%. That split matters because it suggests some of the headline pressure is transitory, but not enough for the Fed to relax. Its own forecasts have still moved higher, with 2026 inflation expected around 3.6% headline and 3.3% core.

US Headline and Core CPI

Energy-led price pressure has lifted headline CPI, while core inflation has remained more contained, leaving the Fed focused on persistence rather than one-off shocks.

Source: Bureau of Labour Statistics

At the same time, growth is moderating rather than breaking. Q1 GDP was around 2%, the Fed’s 2026 growth forecast is near 2.2%, and the labour market is cooling from very tight levels but remains broadly firm, with unemployment around 4.3%. For us, the important point is that the economy is no longer running hot enough to justify a clearly hawkish reaction function, but it is also not weak enough to force the Fed into an early cutting cycle. Payroll momentum has slowed, job openings have normalised, and wage growth is less threatening than it was at the peak. Yet household balance sheets and consumer spending have not deteriorated enough to make growth the dominant concern. This leaves the Fed in a difficult middle ground: inflation is still too high to ease comfortably, while growth is soft enough to make every data print matter more for yields, risk sentiment and the dollar.

The New Fed

Against that backdrop, the appointment of Warsh shifts the market focus away from a simple question of whether the Fed will cut, and toward how much tolerance the new Chair has for inflation volatility, weaker growth and political pressure.

The institutional backdrop is important but should not dominate the market story. The Supreme Court has expanded presidential authority over much of the federal regulatory state, while also preserving some protection for Federal Reserve independence. The Fed remains legally independent from the President, although the pathway for removing a governor for sufficiently serious wrongdoing keeps the issue politically sensitive. Under Warsh, the market question is less about legal independence itself and more about whether investors believe the Fed will resist White House pressure when inflation or growth conditions demand it.

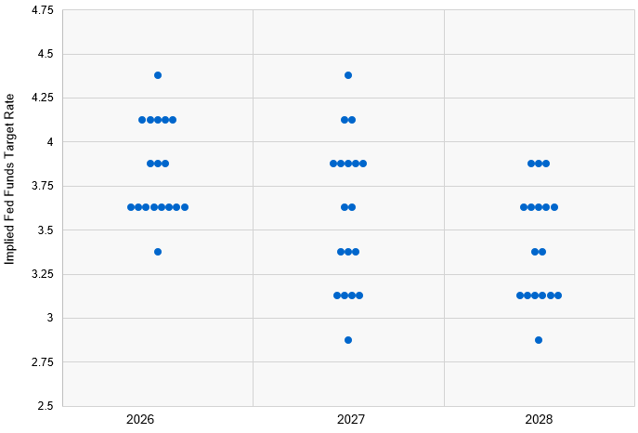

Fed Dot Plot: June Meeting

The June projections point to a more hawkish near-term rate path, with easing expectations pushed further into 2027.

Source: The Federal Reserve

So far, Warsh has leaned more hawkish than expected. Despite earlier assumptions that he might be sympathetic to Trump’s preference for easier money, his first policy signals have emphasised inflation control, reduced forward guidance, and greater data dependence. That is important because a Fed that gives less guidance effectively hands more of the policy reaction function back to the data. Markets will have less visibility on the committee’s next move, keeping yields and the dollar more reactive to CPI, payrolls, wages, and any tariff- or energy-led inflation surprises.

With half of Fed officials now expecting a hike by year-end, the committee still looks uncomfortable with inflation risks. This reinforces a higher-for-longer bias and supports the dollar by preserving the US real-yield advantage, but it also raises the risk of sharper two-way moves whenever incoming data challenge the market’s interpretation of the Fed path.

Our base case therefore remains that the Fed holds rates at 3.5–3.75% through late 2026, with a small risk of one additional 25bp hike if inflation proves sticky, especially if tariffs or energy prices pressure households beyond a simple supply shock. A cutting cycle is more likely to emerge in 2027 than immediately. Short-end yields should therefore remain anchored, while long-end yields may drift lower if markets gain confidence that inflation is easing, although heavy Treasury issuance and term premia should limit the move.

USD Outlook

For the USD, this means the market has already priced a more hawkish Fed. The dollar index has pushed back above 101, highs not seen since May 2025, as investors revised away from aggressive easing and back toward a higher-for-longer path. The question now is what comes next once that repricing is largely embedded.

The lack of near-term cuts should keep the dollar resilient through yield differentials, but the upside is likely to be more limited into the second half of the year unless the data force another hawkish reset. We therefore expect the dollar to remain supported, with upside spikes on hotter inflation, stronger labour data, or any Warsh communication that reinforces anti-inflation resolve, but less scope for a sustained trend higher if growth continues to moderate and risk sentiment holds up.

FX volatility is likely to remain event-driven, centred on inflation, labour data, Fed communication, and election polling. In short, the Warsh Fed keeps USD downside limited for now, while the midterms add headline volatility rather than a durable trend unless the result materially shifts fiscal expectations.

GBP/USD Outlook

Our base case is for GBP/USD to remain under modest downward pressure through H2 2026. UK growth has lost momentum, while the BoE remains constrained by a combination of softer activity and a still challenging inflation outlook. At the same time, we do not expect UK rates to become sufficiently attractive relative to the US to generate sustained support for sterling.

Politics and fiscal policy are unlikely to be the primary drivers of GBP/USD under our central scenario, provided the new government maintains its commitment to fiscal discipline. However, sterling remains exposed to periods of risk aversion given the UK's reliance on foreign capital and its twin fiscal and external deficits.

While we do not expect a significant appreciation in the dollar from current levels, the fundamental picture still appears more supportive for the US than for the UK.

US economy continues to expand at a moderate pace, the labour market remains relatively resilient, and the Fed retains a higher-for-longer bias despite expectations for gradually softer inflation. By contrast, UK growth has slowed, political uncertainty has increased, and the BoE has limited flexibility to respond to weaker activity while inflation remains above target.

Taken together, we see limited scope for sustained GBP/USD upside through the remainder of 2026. Relative growth expectations, Fed-BoE policy differentials and confidence in the UK's fiscal framework are likely to remain the key drivers of the pair, with risks continuing to favour modest sterling underperformance against the dollar.

Glossary

GBP/USD: The exchange rate between sterling and the US dollar, showing how many dollars one pound buys.

DXY: The US Dollar Index, which tracks the dollar against a basket of major currencies.

PMI: Purchasing Managers’ Index; a survey-based indicator of business activity where readings above 50 indicate expansion and below 50 indicate contraction.

CPI: Consumer Price Index; the main measure of consumer inflation used by central banks and markets.

Dot plot: The Federal Reserve’s quarterly summary of policymakers’ individual projections for the appropriate policy rate.

Source Abbreviations

• FRED: Federal Reserve Economic Data.

• ONS: Office for National Statistics.

• BLS: Bureau of Labour Statistics.

• Fed: Federal Reserve.

• BoE: Bank of England.

• OBR: Office for Budget Responsibility.

• MPC: Monetary Policy Committee.