UK 2025 Autumn Budget

This week brings Rachel Reeves’ second Autumn Budget, a key moment for the government’s economic agenda. The combination of slow growth and high debt has created a demanding environment for fiscal decisions. Investors and households alike will look for clarity on how policy will evolve in the year ahead. Given this backdrop, what should we expect from the coming Budget?

A stuck economy, rising debt

The economic environment remains challenging. Real GDP growth has been subdued for several years, and the OBR now expects the economy to grow by around 1% in 2025, roughly half the pace it anticipated a year ago. Much of that downgrade reflects persistently weak productivity. Public sector net debt stands at around 94–95% of GDP, similar to levels last seen in the early 1960s, and borrowing in the year to October reached 3.9% of GDP, approximately £116.8bn and above earlier projections.

Low growth combined with still-elevated real interest rates creates a difficult setting for an economy carrying a large debt burden. Even with markets expecting gradual Bank Rate reductions over the next year, debt interest remains a significant and unpredictable component of public spending. The UK continues to face a set of structural constraints: pressure on the health system contributing to higher disability claims, elevated housing costs driving up welfare needs, and weak productivity weighing on earnings and tax receipts. In this environment, Reeves is under pressure to make progress on the fiscal position, although the available choices are limited and none are straightforward.

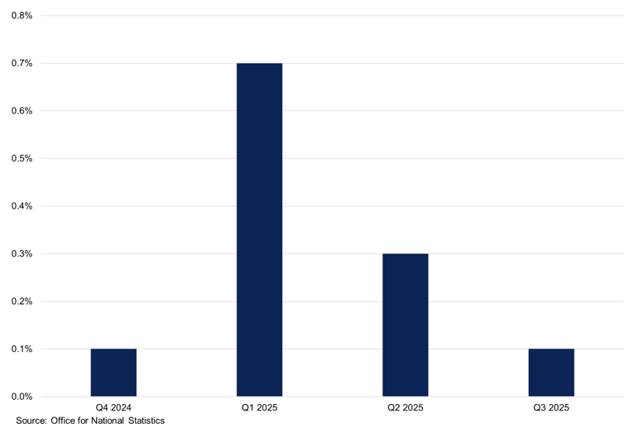

UK ANNUALISED GROWTH QOQ

GDP growth softened in Q3 2025.

Fiscal rules and the need to keep gilts onside

Labour has tied itself closely to its fiscal framework, which requires a surplus on the current budget by 2029–30 and public debt to be on a downward path as a share of GDP in the target year of the forecast. With borrowing already running ahead of expectations and the OBR likely to revise down its medium-term outlook for growth and productivity, Reeves faces a gap of roughly £20–30bn to remain within those rules. This places the emphasis firmly on measures that strengthen the fiscal position, whether through higher revenues or tighter control of spending.

Another factor is the lingering caution created by the gilt market turmoil after the 2022 mini-Budget. That episode, when long-dated yields spiked and LDI funds came under strain, remains prominent in investors’ minds. Reeves is therefore expected to avoid any measures that could be seen as unfunded or out of line with her fiscal rules. That expectation was reinforced by Moody’s recent decision to affirm the UK’s Aa3 rating with a stable outlook, noting its confidence that forthcoming policy announcements will remain aligned with the government’s fiscal commitments.

The government’s debt management approach has already begun to reflect this need for caution. The 2025–26 gilt remit is large at just under £300 billion, and the DMO has shifted issuance toward shorter maturities and bills while reducing reliance on long-dated gilts. It has also increased the portion of unallocated issuance to retain flexibility as conditions change. Long-dated yields remain close to levels last seen in the late 1990s, making additional duration relatively expensive at a time when the Bank of England is working to improve the resilience of gilt and repo markets. In this setting, a Budget that keeps borrowing contained and aligns closely with the DMO’s strategy would help reinforce policy credibility and support market stability.

GBP/USD

Sterling remains under pressure against the dollar.

Personal tax: stealth, not shock

On the personal side, the most likely source of additional revenue is an extension of fiscal drag rather than increases in headline tax rates. The freeze on income tax thresholds and allowances already runs to 2027–28, and credible reporting now suggests Reeves may extend this to around 2030 while potentially adjusting some thresholds instead of raising nominal rates. This approach gradually moves more basic-rate taxpayers into higher-rate bands and brings more estates into inheritance tax as frozen nil-rate bands intersect with rising asset values. The Treasury can frame this as a matter of fairness and stability rather than a direct increase in income tax, yet over the next five years it would still raise substantial sums and place a greater tax burden on middle-income households.

Politically this approach carries risks, although it is still viewed as less contentious than a direct increase in tax rates. The wider implication is that the government intends to rely on a gradual widening of the tax base over time.

Developed Economies' 10YR YIELD

UK 10-year yield remains elevated compared to other developed economies.

Property and wealth

If Labour wants to demonstrate that it is taxing wealth rather than placing additional pressure on workers, property is the most straightforward area to target. Council tax is the simplest tool, and the IFS notes that doubling charges on band G and H homes could raise more than £4bn a year by the end of the decade. A mansion tax is also being discussed, with ideas ranging from a revaluation of higher bands to an additional levy on homes above £2m. To address concerns from households that are asset-rich but income-poor, the Treasury may allow payments to be deferred until a property is sold or transferred.

From a market perspective, a combination of council tax changes and a well-signalled mansion tax could raise meaningful revenue while appearing progressive and being harder to avoid than broader wealth taxes. The main risk is a slowdown at the top end of the housing market and a perception that policy is becoming less favourable to homeowners in the South.

Pensions: less about rates, more about the plumbing

Pension tax relief, which costs around £45–50bn a year, is a regular feature of Budget debates. Reeves has little room for major reforms without unsettling auto-enrolment or long-term saving, so changes to relief rates or the annual allowance look unlikely. The focus is more likely to fall on salary sacrifice and the technical side of relief. Surveys suggest most employers expect tighter rules, with a possible cap on the amount of pay that can be put into pensions through salary sacrifice while remaining free of NICs, with figures near £2,000 often mentioned. This could raise several billion pounds, though it may also reduce incentives to contribute above the minimum.

A further idea being explored is a small levy on pension fund values, collected by fund managers and applied mainly to larger pots, which could generate meaningful revenue with limited complexity. These ideas remain under discussion, but the overall direction points to a gradual tightening of the more generous features of the system rather than a major redesign.

UK CPI Core vs CPI total services vs CPIH

Inflation in the UK continues to show signs of stickiness, particularly in the services sector.

“Sin” taxes and targeted business measures

The Budget is also expected to tighten taxes in areas where political resistance is lower. Gambling duties are likely to rise, with changes to remote gaming, betting and machine duties under active consideration, which markets will likely interpret as a targeted sector move rather than a broader policy shift. Increases in sugar, tobacco and alcohol duties could follow, although these are more likely once inflation moves closer to target and the pressure on household budgets eases, with hospitality expected to receive some limited protection.

On the business side, the clearest change would be the removal or sharp reduction of low-value consignment relief on imports under £135, a step that would raise costs for overseas fast-fashion and discount platforms, while delivering a steady revenue uplift for the Treasury.

Our View

Our view is that this Budget will be shaped primarily with the gilt market and ratings agencies in mind, with voters a secondary consideration. Reeves is likely to emphasise strict adherence to her fiscal rules and a commitment to rebuilding headroom. The aim will be to signal stability and predictability after recent years of volatility, even if this requires further indirect tax measures on income, property and pensions at a time when households already face a heavy tax burden and stretched public services. We expect markets to respond positively, with a relatively calm gilt market and a contained risk premium.

For sterling, however, the balance of risks looks softer. A fiscally cautious Budget that leans on higher effective taxation and muted growth assumptions is unlikely to offer near-term support for the currency. We expect the combination of weak domestic momentum, tight spending plans and a lack of clear catalysts for stronger growth to keep sterling on the back foot into early 2026, particularly against the US dollar.