UK Economy

The UK economy enters 2025 facing a complex set of challenges but also showing signs of resilience. While sluggish growth and weakening confidence across key sectors continue to weigh on the outlook, recent data offers reasons for cautious optimism. Business investment increased by 1.2% in Q3 2024, standing 4.5% above last year’s levels, suggesting that some firms are maintaining confidence in longer-term prospects despite economic uncertainties.

Fiscal pressures remain a central concern, as the government grapples with the dual challenge of managing elevated public debt while supporting growth. These domestic hurdles are further compounded by external factors, including shifting global trade dynamics and geopolitical tensions.

While moderating inflation provides a glimmer of hope, structural issues such as subdued productivity and fragile confidence could limit the impact of monetary easing. As the UK navigates these headwinds, understanding the interplay of fiscal policy, monetary measures, and global pressures will be critical for assessing the economic trajectory in the year ahead.

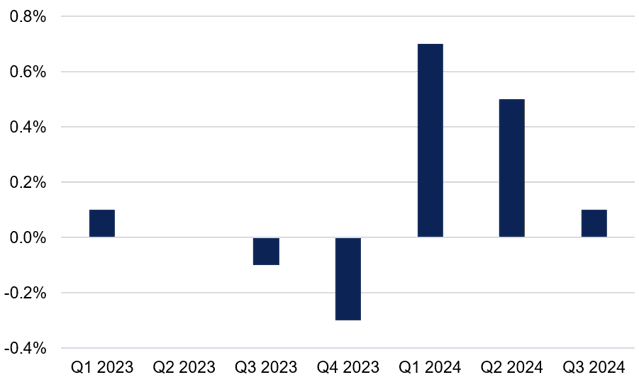

UK ANNUALISED GROWTH QOQ

UK GDP growth has been weakening in the recent quarters.

Source: Office for National Statistics

The UK economy’s performance in late 2024 suggests a challenging road ahead for 2025. GDP growth for Q3 2024 came in at a sluggish 0.1% QoQ, below expectations of 0.2% QoQ, underscoring the economy's fragile momentum. Earlier in the year, the services sector, which accounts for about 80% of the UK’s GDP, was a key driver of growth. However, by the second half of 2024, the sector’s performance began to falter, reflecting growing economic uncertainties and declining sentiment.

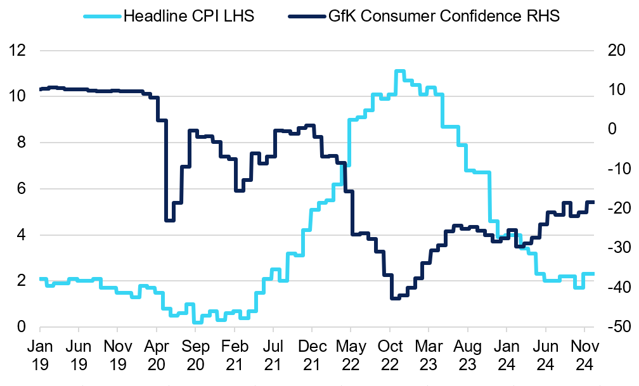

Consumer confidence, a bellwether for spending and economic activity, has come under pressure in recent months. The GfK Consumer Confidence Index, which had been steadily improving since the pandemic, dropped from -13 in August to -21 by October, marking a 7-month low. However, confidence showed a modest improvement in November, rising to -18, suggesting tentative stabilization in household sentiment. Despite this, concerns about household spending remain, as the broader economic environment continues to weigh on consumer optimism.

UK HEADLINE CPI VS GFK CONSUMER CONFIDENCE

Consumer confidence remains subdued.

Sources: GfK, Office for National Statistics

The services sector grew by a marginal 0.1% in Q3, with recent data pointing to further deceleration. The November S&P UK PMI Services Index showed its lowest reading since August, indicating a marked loss of momentum. Service providers reported near-stagnant activity, workforce reductions, and declining business optimism, with growth expectations falling to their weakest since late 2022. These trends hint at muted service sector contributions to GDP in the coming year.

This subdued performance highlights the difficulty in coordinating fiscal and monetary measures to stimulate growth. Rising employer costs, limited fiscal flexibility, and persistent but moderating inflation create considerable barriers to reigniting momentum in 2025. Compounding these issues are the pressures on public finances. Public debt reached 100% of GDP in August 2024, the highest level since 1961. The combination of stagnant GDP growth and elevated debt creates ongoing challenges, with limited economic expansion leaving little room to offset fiscal pressures.

Interest payments have become a growing concern, accounting for 4.5% of GDP in 2023—double the UK’s defence budget. This burden reduces fiscal space for growth-enhancing investments and heightens risks if external shocks require additional fiscal support.

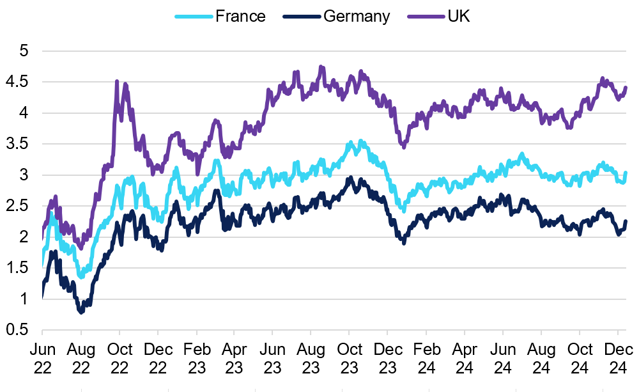

UK VS FRANCE VS GERMANY 10YR BOND YIELD

The spread between UK and European bonds has been increasing.

Source: Bloomberg

UK Budget Analysis

The new government has implemented a tax package expected to raise £40 billion—equivalent to over 1% of GDP—through changes such as increased National Insurance contributions (NICs), tightening inheritance tax exemptions, and reducing private equity carried interest tax breaks. Combined with an additional £30 billion in borrowing, the measures aim to fund £70 billion in government spending. However, doubts remain about whether these policies can deliver the needed boost to growth and confidence.

The NIC increase, particularly for employers, is set to raise labour costs, discouraging hiring and potentially leading to reduced investment or workforce reductions. These impacts are likely to weaken consumer spending and exacerbate challenges in the labour market. While approximately one-third of the planned spending increase is allocated to infrastructure, the lack of detailed plans for housing, energy, skills, and transport investment clouds its potential effectiveness. Outside London, public transport systems highlight the urgent need for funding, with South Yorkshire’s bus network shrinking by 42% over the past decade.

Persistent underinvestment in infrastructure and equipment remains a core issue, directly impacting productivity growth. UK productivity—measured as output per hour worked—has grown just 6% since 2008, compared to 24% in the US, highlighting deeper structural weaknesses. While wage growth has accelerated in recent months, with average weekly earnings excluding bonuses rising to 5.2% in the three months to October, real pay gains remain constrained by inflation and long-term productivity stagnation. Since 2007, real wages in the UK have seen limited progress, lagging behind the 17% and 10% increases in the US and OECD countries, respectively. Rising housing costs further compound these pressures, with UK rents increasing by 13% in the two years to May 2024, far outpacing the 4% seen in France and Germany.

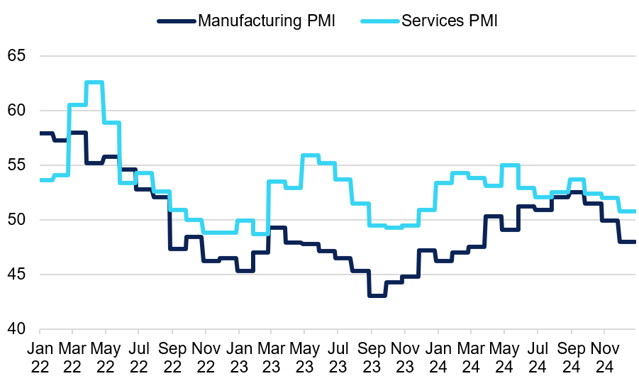

S&P GLOBAL US MANUFACTURING VS SERVICES PMI

UK business activity has weakened recently.

Source: S&P Global

Inflation and Monetary Measures

At the same time, the inflation outlook remains challenging, influenced by recent fluctuations, rising energy bills, and the government’s fiscal measures. Although inflation has moderated from its peak of 11.1% in October 2022, the past two months have seen renewed upward pressure. In October 2024, inflation climbed to 2.3%, up from 1.7% in September, surpassing the Bank of England’s 2% target. This resurgence, driven in part by higher energy costs, raises critical questions about the central bank’s ability to support growth without risking a new wave of inflationary pressures.

The Bank of England appears cautious, holding interest rates steady amid expectations that further reductions will come more gradually compared to central banks in Europe and the US. Market pricing suggests that no cuts are likely in December 2024, but there is a 77% chance of a 25bps reduction in February 2025 as part of the ongoing monetary easing cycle. In October, Governor Bailey indicated his baseline expectation of four rate cuts in 2025, but the scope for significant easing is constrained. The neutral rate—thought to balance inflation and growth—may have risen to between 3% and 4%, limiting the Bank’s flexibility. Additionally, the UK 10-year gilt yield has remained above 4.2% since October, reflecting persistent market caution.

Geopolitics

Meanwhile, geopolitical tensions and the growing threat of protectionism are set to further challenge the UK economy in 2025. While the direct impact of tariffs might be less pronounced for the UK than for Europe, the prospect of higher global trade barriers remains concerning for UK manufacturers. These businesses are already grappling with elevated costs, weak demand, and heightened uncertainty. One key risk stems from potential US tariffs, expected to be a universal 10% levy on all imported goods, including those from the UK. As the US is Britain’s largest single export market, accounting for over 20% of total UK exports in 2023, these tariffs could still significantly impact trade. Estimates from the National Institute of Economic and Social Research suggest such tariffs would reduce the UK’s GDP growth by 0.7 percentage points, further constraining an already struggling economy.

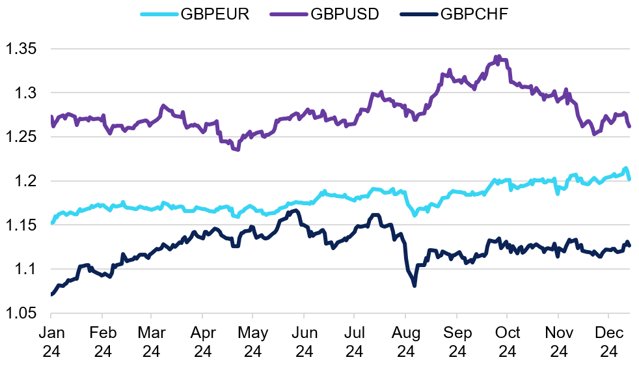

CURRENCY PAIR MOVEMENTS

The sterling has been steadily appreciating against the weakening euro.

Source: Sucden Financial

Final Notes

The UK economy faces a challenging year ahead, shaped by muted growth, elevated debt, and mounting external pressures. While moderating inflation provides some room for the Bank of England to ease monetary policy, rate cuts alone will not address the structural issues of underinvestment, sluggish productivity, and trade risks. Targeted investments in infrastructure and productivity, alongside a clear fiscal strategy, will be critical to restoring confidence and building resilience.

These structural challenges are also expected to have significant implications for currency markets. The pound is likely to weaken against the US dollar as trade risks, slower growth, and geopolitical uncertainty weigh on investor sentiment. In contrast, the pound may perform better against the euro, given the Eurozone’s parallel economic struggles. This divergence presents an opportunity for investors to hedge exposure and strategically position themselves to benefit from disparities in currency performance.