Executive Summary

- In Q3 2020, signs of global economic recovery are becoming more pronounced; however, this recovery is not uniform and is primarily driven by government spending while domestic demand is lagging

- Since the beginning of easing lockdown measures, the credit data indicated that spending has improved; however, it remains below pre-crisis levels

- Fiscal and monetary policy has shown to be successful in protecting people and businesses; however, containment measures failed to protect to slow down the virus

- Because of signs of new localised outbreaks, economies are at risk once again in Q3, potentially requiring another inflow of fiscal spending

- The outlook of the US economy in the upcoming quarter will depend on two things: the spread of the virus and the policy environment.

- In Europe, intra-bloc tourism will set the trajectory for recovery, especially as international travel remains low, and the way the countries will monitor the spread of the virus

- Nevertheless, consumer aversion to public places and adjusted working-from-home conditions are more likely to keep consumers at home for longer

- Despite the Chinese economy being the first country to recover from the pandemic, consumers remain wary of social interactions, and increasing tensions between China and the US add to economic uncertainty

- In Brazil, the lack of appropriate lockdown measures along inadequate healthcare provision has left the country to be an epicentre of one of the world's most severe waves of infections

- In major coffee exporter countries, the rebound in Q3 will be lower than expected due to the low performance of foreign demand and private consumption

- Earnings results saw that the inevitable drop off in demand away-from-home. However, Starbucks results suggest that approximately 97% of its stores across the globe are open

- JDE Peet’s earnings show that the consumer packaged goods market has seen strong sales, aiding the premise that at-home consumption has offset the loss of out of home consumption

- Below we have calculated the potential loss of demand during the lockdown and as economies have started to re-open, using various assumptions

- Online sales have also seen a large increase, and we expect H2 2020 demand to return to more normal levels and help offset the loss in H1 2020

- From a supply perspective, we are expecting rains in Brazil to help offset some of the recent dryness

- There is talk of some very early flowering in the Conillon areas which is very early, especially as we are moving into an off-cycle

- This year’s delayed harvest continues at a steady clip and is 90% finished at the time of writing, shipments have slightly tailed off.

- Local Brazilian prices have seen more selling, and we expect coffee to be bought at the current differentials

- The March21/March22 spread has tightened significantly, in the last few months

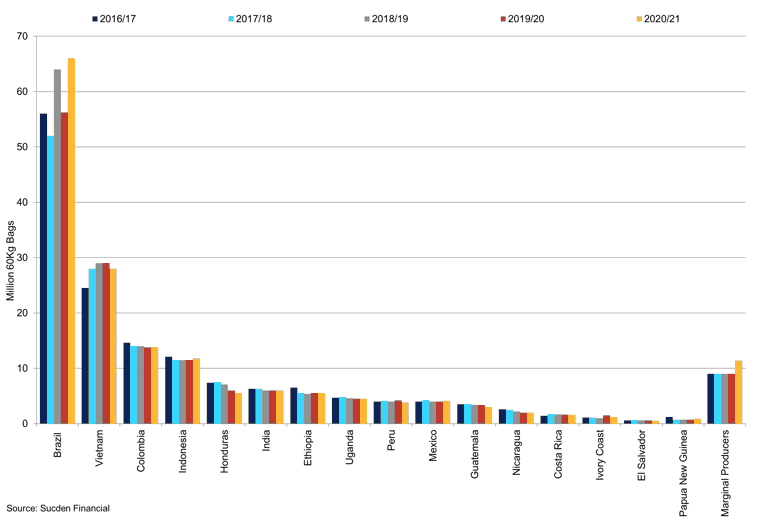

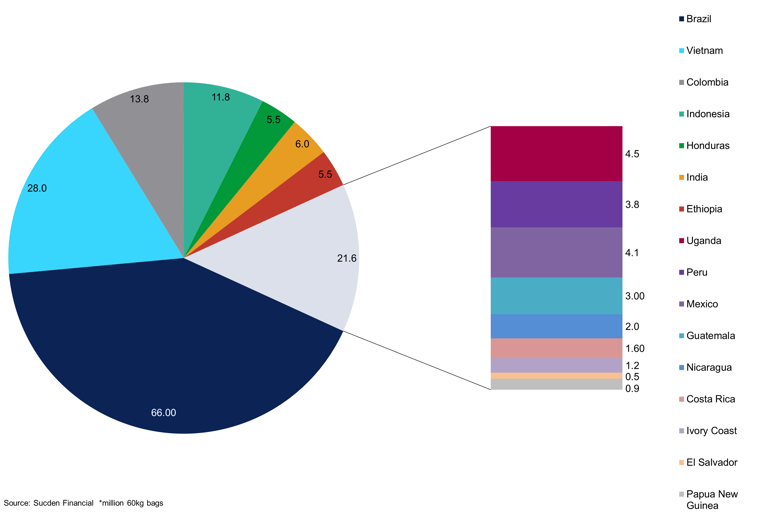

- We have increased our Colombia crop for the current year to 13.8m bags, after a good Mitaca crop

- While we have also increased our Honduras number by 500,000bags to 5.5m bags, we still see issues in C.America.

- Lack of skilled workers and the recent lockdowns have hindered the crop but progress was better than we expected.

- We still see tightness in mild Arabica’s going into next year, especially after the recent drawdown in Honduran certified stocks

- We have dropped our Vietnam crop figure to 28m bags from 29m bags and we expect this to prompt tightness in the longer-term spreads

- Carry-over will be lower and we expect Ho Chi Minh inventories to continue to fall with the lower crop number

Market Activity & Trade Ideas

- The rally in both contracts has been strong, and consistent with our June report we favoured building a long Arabica futures position but deferred down the curve. This has proved fruitful

- We maintain our options view of owning Dec 130 call which currently costs $5.99, in our last report the premium was $2.85

- We still think there is an upside to this option but it could be worth selling a Dec 160 call worth $1.75

- The March 2021/March 2022 spread has widened to $4.10 since tightening into $2 and we anticipate further tightness and favour holding a long position

- For Robusta, we favour owning the November 2020/November 2021 spread which trades at -$75 at the time of writing

- We are bullish on Robusta futures, with a potential drop-off in Vietnam and Conillon crops and a recovering demand outlook. However, if traders prefer to play the options market by buying 1400 January calls and selling 1600 January calls, you pay out $57 but could potentially only make $140. With this in mind, futures may have more value

Macro Overview

US

As the nation enters the Q3 of 2020, the outlook on economic recovery is shifting. The view was that once lockdown measures are lifted, the consumer spending would rebound to normal levels, driving the economic growth. That does not seem to be the case anymore. Consumer aversion to public places and adjusted working-from-home conditions are more likely to keep consumers at home for longer. Indeed, the retail sales bounced back in May to 17.7% m/m and then grew at a slower pace in June at 7.5% m/m, and the total yearly change was 1.1%, as shops opened across the country. Overall, since the beginning of easing lockdown measures, the credit data indicated that spending has improved; however, it remains below pre-crisis levels.

While in most of the European countries the virus spread seems to be under control, the situation in the US appears to be heading in a different direction. Although fiscal and monetary policy has shown to be successful in protecting people and businesses, containment measures in much of the country failed to protect to slow down the virus. Therefore, because of signs of new localised outbreaks, economic activity is at risk once again in Q3, potentially requiring another inflow of fiscal spending. At the time of writing, the enhanced unemployment insurance payments are expiring by the end of August. Thus, without new significant interventions by the government, lack of fiscal support could significantly drag on economic recovery.

According to more high-frequency data, overall consumer spending peaked in mid-July before gradually subsiding in the subsequent months. As of July 31st, personal spending was 5.6% in June, slightly softer growth than the previous month at 8.2%; however personal consumption for Q2 was -34.6%. Indeed, initial jobless claims increased for a couple of weeks in July but have since started to fall week on week, with claims in the week up to August 1st at 1,186,000, continuing claims for the week up to July 25th were 16,107,000. Some employees remain nervous about going back to work; this is where testing remains key. The outlook of the US economy in the upcoming quarter will depend on two things: the spread of the virus and the policy environment, and the latest deadline for the new stimulus package has passed after a deal could not be agreed on. As stated by Pres. Trump, "the situation will get worse before it gets better", and while news of the vaccine is hopeful, we do not envisage an effective wide-spread use in the medium-term.

As for the manufacturing and service industries, while most of the European economies seem to be returning to normal, the US performance seems to be just staying above the water. Indeed, the ISM service PMI index has increased to 49.6 in July from 47.9 in June, indicating that the economy is still contracting. At the same time, the manufacturing PMI index increased from 49.8 in June to 51.3 in July. On the other hand, the housing market is started to show signs of recovery in June after housing started improved to 1,186,000, up from 1,011,000 the month before. Building permits were also higher, at 1,258,000m for June, with new home sales also increasing to 776,000 for June, up from 682,000.

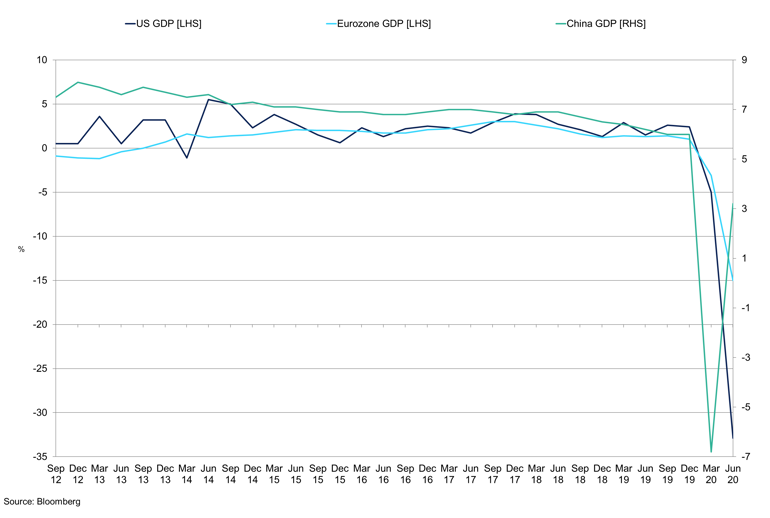

US, Eurozone and China GDP Growth

The world's biggest economies experienced record growth declines due to COVID-19 containment measures in H1 2020.

Overall, the US outlook remains muted as renewed lockdowns and signs of fiscal expirations daunt on consumers. In Q2, the US economy contracted by 32.9%, we expect an improvement in Q3 but is too early to say for sure yet as cities and states delay reopening of their economy. At the same time, the Fed is expected to keep the federal reserve rate at record lows of 0.00-0.25% for the long-term. Even as the Fed maintains its loose monetary policy stance and provides further fiscal support, continuing social distancing measures are likely to keep GDP well below its pre-crisis levels, and the unemployment rate elevated.

The virus outbreak and the government response in the US have severely reshaped the pattern of personal income and expenditures. Real disposable income fell 5.0% m/m in May as government stimulus checks declined and was only partially offset by a rise in wage income as employment rebounded. The lion's share of the decline was due to a reduction in spending on services. The savings rate increased from 9.5% in the first quarter to 25.7% in the second quarter.

Europe

After a prolonged period of debates, the EU has agreed on a EUR750bn recovery fund to provide support for all member states. This new deal is by far the biggest fiscal action undertaken by the bloc. Additionally, the ECB has expanded its asset purchase programme by additional EUR600bn, as a high degree of uncertainty took a toll on consumer and business spending. According to ECB President, Christine Lagarde, the EU economy is forecast to contract by 8.7% y/y in 2020, and inflation is to remain low for the rest of the year.

The ISM PMI indices for the Eurozone indicated strong growth in July, as services increased from 48.3 in June to 55.1 July and manufacturing jumped from 47.4 to 51.1 in the same period. However, backlogs and stagnant employment could pose risks to recovery. Indeed, firms are proceeding to reduce headcounts at a fast pace.

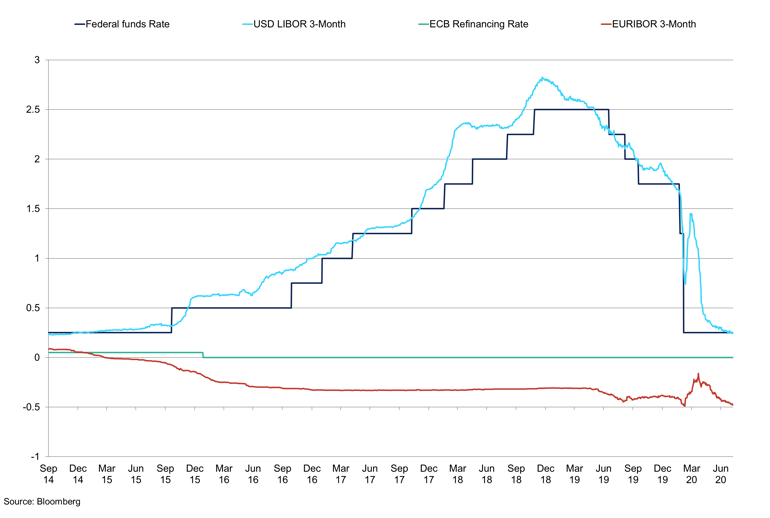

Developed Economies Interest Rates

Most of the developed economies lowered interest rates to record-lows to inject liquidity back into the market.

Consumer spending aided the economic recovery in June, exemplified by retail sales turning positive once again at 1.3%y/y, but growth slowed on m/m basis to 5.7%. The strength of consumer engagement in Europe is helping to offset weaker growth of the industrial sector. Europe is being hurt by the weak global demand for its exports and weak business investment, exports but strengthening domestic consumption may help to offset this. However, unemployment levels are expected to rise, and this will have a significant impact. The trade balance in May was 8bn surplus, up from 1.6bn the month prior. We could see the surplus increase once again in June, however, as cases start to rise in Europe and some travel bans are re-instated this will present some headwinds to the bloc. However, one bright spot is that in 2018 70% of EU tourist came from within the country of residency.

Comparing to the US, the unemployment rate has remained quite low during the pandemic, thanks to quick implementation of employment protection programmes. The result was that in June, the unemployment rate has picked up to 7.8%, comparing to 16.5% in the US for July. However, as the bloc continues to lift strict lockdown restrictions, many of the protection schemes will also be diminished, resulting in a sharp pickup in unemployment.

Germany, Europe's largest economy shrank by 10.1% q/q in Q2, declining marginally faster than the US, outlining the scale of the challenge the European economy after the devastation of virus restrictions. As we enter Q3, economic activity is starting to expand while keeping the number of infected low. Tourism will set the trajectory for recovery, and the way the countries will monitor the spread of the virus. The situation in Spain has clearly emphasised tourism's importance in the country's recovery.

China

Chinese economy rebounded strongly in Q2 2020 to 11.5% q/q after falling at the fastest pace on record in Q1. This, however, could be attributed to strong growth in the industrial sector, largely driven by government investment into infrastructure as well as a strong level of exports. Yet, consumer spending remains weak, at -1.38% y/y in June. On a year-to-date y/y perspective, sales are down 11.4% in June; we expect both to continue to improve in the coming months. Despite the Chinese economy being the first country to recover from the pandemic, consumers remain wary of social interactions, and increasing tensions between China and the US add to economic uncertainty.

Industrial production in China has continued to grow, up 4.8% y/y in June, the best growth since December 2019. By industry, output was up 13.4% for automotive, up 12.6% for computers and electronics, and up 8.7% for electrical machinery. Meanwhile, retail sales were down 1.8% y/y in June, and overall investment continued to decline. Overall, China's economic recovery is ahead of Europe' and the United States', but activity mostly remains below pre-crisis levels.

The COVID-19 crisis disrupted the relationship between China and the US once more, as Pres. Trump lashed out at China over the coronavirus pandemic. As a result of renewed trade spat and overall low global activity, in H1 2020, South Asia became the biggest trading partner with China, surpassing the EU. China's trade with the rest of the world has been rising recently, thanks to the relaxation of lockdown measures in the Western economies, however, remains at the pre-crisis levels. Additionally, China's plan to boost the role of the state-owned enterprises in the economy could further deteriorate trading relations with the US and Europe.

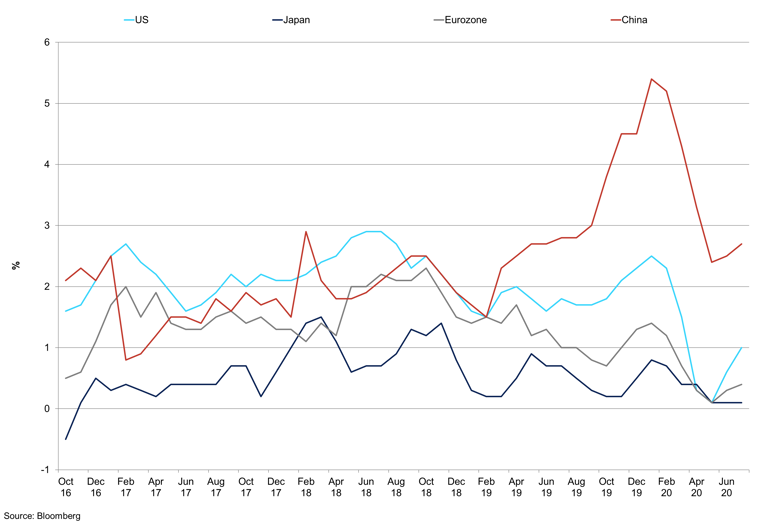

US, Japan, Eurozone and China CPI

China's CPI jumped higher relative to other economies due to high food prices in Q2 2020.

China is undergoing a V-shaped recovery; however, this recovery is not uniform and is primarily driven by government spending while domestic demand is lagging. With the COVID-19 pandemic controlled in April, growth picked up significantly in Q2 by 3.2% y/y. Auto sales recovery supported retail sales, which turned to positive as pandemic eased. High CPI caused by high pork prices have eased, and PPI remains in the negative territory amid sluggish growth.

The fiscal stimulus package is equivalent to around 5% of total GDP, coupled with monetary loosening measures including RRR and LPR cuts and targeted monetary measures on SMEs, is set to add to growth. Thanks to better than expected recovery in Q2, we believe China's fiscal spending will be more conservative in H2, leaving room for more interventions given possible uncertainty.

Origin Focus

Brazil

Compared to other Latin American economies, the Brazilian recession was seen to be more subdued in Q2 2020. In its latest statement, the central bank sounded more optimistic than usual, forecasting a 5.7% GDP fall in 2020, up from -6.5% a month before. Retail sales have picked up from -16.3% m/m lows in April up to a record high 13.9% m/m in May, suggesting strength in the retail sector. Same goes for the industrial activity, as it picked up from -19.20% m/m in April to 8.90% in June. Services, however, continue to be a drag on the economy. These data sets outline the improvement in sequential data sets; however, when we look at the year-on-year data, the economy is struggling. Lower-than-expected inflation could pose a risk to the economic recovery and local currency.

From the monetary policy perspective, the outlook remains expansionary. Indeed, while Brazil's household income-support programme has been substantial enough to offset the consequences of losses in income, the overall package remains below those of other LatAm economies. Nevertheless, Brazil has had one of the most expansive monetary policy stimuli across the emerging markets, with extensive interest rate cuts, down 2.00% since March, and significant credit-enhancing initiatives. These are likely to stay in place in the longer term. Ultimately, more interest cuts are possible, considering the level of uncertainty the economy will face in the remainder of the year.

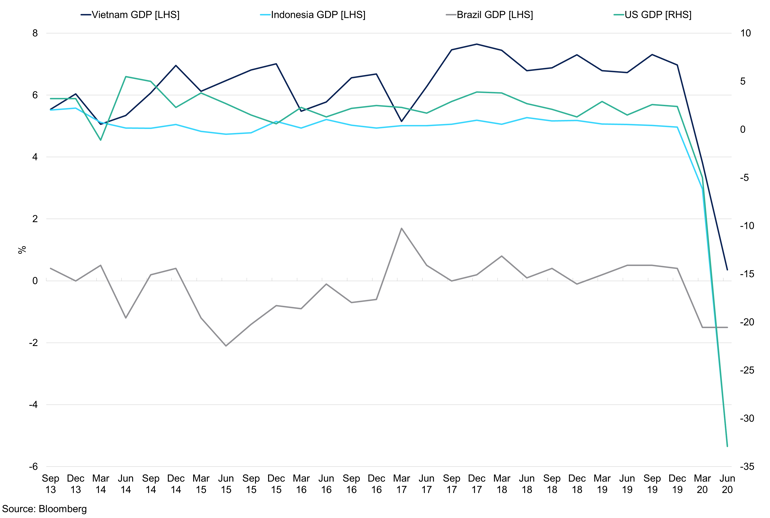

US vs Major Coffee Exporters GDP Growth

Both developed and emerging markets have felt the impact of containment measures, with the US feeling the biggest hit.

The number of coronavirus-related cases has fluctuated significantly since the beginning of the global pandemic. Nevertheless, the lack of appropriate lockdown measures along inadequate healthcare provision has left Brazil to be an epicentre of one of the world's most severe waves of infections. At the time of writing, there are more than 2m cases recorded since March. Nevertheless, as of the beginning of July, there have been aggressive attempts to reopen shops in what to be believed the peak of the spread.

While pandemic-driven spending is viewed as beneficial for the economic recovery, its impact on its tax reform, that urges to decrease the net burden on companies, will be more significant. The new 12% VAT levy will combine the unemployment insurance contributions and 'Cofins' social security levy. According to the Economy Ministry, this could generate between 142,000-373,000 jobs, and increase overall productivity by 0.20%-0.50%.

Brazilian manufacturing expanded in July at the fastest pace on record, as manufacturing PMI picked up to 58.2 in July, as new orders, confidence and hiring rebounded strongly. At the same time, Brazilian data showed a record $8.1bn trade surplus in July as the country exported more than imported. Indeed, strong demand from China, as well as the reopening of Brazilian businesses in June and July, boosted economic activity.

Indonesia

Since reopening its economy in early June, Indonesia has seen a surge in new coronavirus cases and deaths, surpassing Singapore, to become the country with the most reported cases in the ASEAN region. Despite the surge in cases, the government has continued to relax lockdown measures due to fear of a further slump in the economy.

The central bank of Indonesia cut its benchmark interest rate for the fourth time this year to 4.0% to bolster the economy that is forecast to contract by 4.8% in Q2 2020, making it the sharpest decline in almost two decades. In Q1, Indonesia's GDP growth fell to a 21-year low of 2.97% y/y. Nevertheless, the government is expecting a U-shaped recovery in 2020, as the number of infections continues to increase, and the path to recovery is uncertain. Indonesia, in line with other South-East Asian countries, extended the fiscal and monetary support this year to help combat the consequences of COVID-19. Indeed, more than 3.06m have either been laid-off or furloughed as of May 27th, urging the government to launch a new task force to tackle both the public health and economic aspects of the pandemic.

Meanwhile, the government has allocated $47.35bn in stimulus to bolster the economy and expects the budget deficit to reach 6.34% in 2020. It also expects the economy to shrink 0.4% in 2020 under a worst-case scenario or grow 1% in the best-case. Additionally, Indonesia is placing $793m in state funds with some regional development banks and extending loans to provincial governments to support economic recovery amid the pandemic. Nevertheless, the government is facing the daunting task of borrowing $104.53bn this year to fund the budget deficit, which is expected to reach 6.34% of GDP, as well to finance investments and repay its debts.

Vietnam

While Vietnam managed to contain the COVID-19 outbreak, with 685 total confirmed cases since the beginning of March, its economy has been hurt in H1 2020. The country's GDP was still growing at 0.4% in Q2 2020, yet it was the worst performance since 1985. A drop of almost 7pps seems just below of those seen in the Western economies in Q2, and short lockdown measures have made Vietnam one of the first ASEAN economies to be open for business after the hit of the pandemic. Nevertheless, for 2020, growth is expected to contract 3.0-4.0%.

Manufacturing is a huge part of the Vietnamese economy, and the PMI was negative in July at 47.6, a fall from 51.1 in the previous month. New orders contracted in July, and this was also accompanied by a sharp drop in export sales, with employment suffering further. Delivery times have continued to lengthen once again. The trade balance recovery in July to $1,000m, beating expectations of $300m, and June's total of $500m. Exports improved marginally by 0.3% y/y in July, but imports declined by 2.9% y/y. We continue to watch the country's propensity to import, as this suggests a weak consumer market and may indicate a weak employment market. Industrial production did rebound strongly in June to 7% y/y, up from -3.1% y/y the month prior.

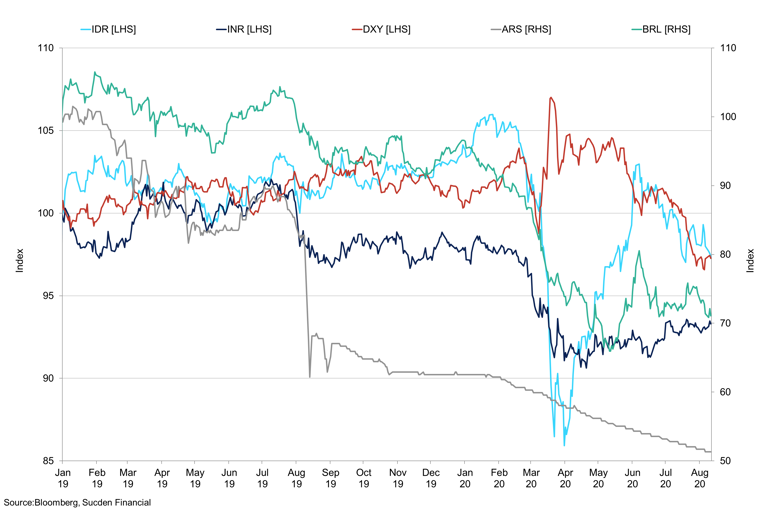

Emerging Market Currencies

Most of the emerging market currencies depreciated significantly during H1 2020, as the dollar became the new safe-haven.

The authorities estimate that over 30m people, approximately 50% of the labour force, were affected at the height of the lockdown in April. Urban unemployment rose 33% in Q2, while average income per worker decreased 5%. We believe that the rebound in Q3 will be lower than expected due to the low performance of foreign demand and private consumption, the main drivers of Vietnam's growth. Like everywhere else in the world, household consumption is likely to stay low given low income, and exporters will suffer from constricted global trade activity. Indeed, all manufacturing exports have contracted in H1 2020, with the negative trend accelerating during the most recent months. Spending on necessities, which contributes to more than 40% of Vietnam's GDP, however, remained robust throughout the pandemic and is likely to be stable for the rest of 2020.

Vietnam is an import-dependent exporter, and due to suffering global trade, the economy has felt the brunt of the crisis the most. Due to a fall in exports from China in Q1, Vietnam has experienced a 21% dip in FDI, as investors put their plans on hold during the crisis. China's gradual shift from labour-intensive manufacturing could help accelerate Vietnam's transition as a substitute market.

Nonetheless, compared to other South East Asian Economies, Vietnam is in a better position to escape the consequences of an outbreak. Firstly, before the pandemic took hold, Vietnam reduced its public debt-to-GDP ratio to 7.0%, leaving enough room to implement an expansive fiscal stimulus programme later in the year. Indeed, cuts in corporate income tax should alleviate some of the pressure off businesses. Secondly, by staying ahead of the curve, Vietnam has higher chances of attracting foreign demand, both business and tourism-related. Additionally, China's manufacturing shift to Vietnam could add to the country's growth in 2020. Ultimately, appropriate containment measures in the upcoming months will be crucial in sustaining the economic recovery.

To help offset the effects of the COVID-19 pandemic, the government had introduced fiscal stimulus of around $11.68 billion, or 3.4% of GDP, including tax deferrals, cuts and exemptions, and cash transfers to affected workers and households. The government debt-to-GDP ratio is expected to rise to around 42% in 2020 from 37% in 2019.

Corporate Earnings

Starbucks

A vast majority of the stores around the world have reopened, with a steady recovery felt in sales. Nevertheless, global comparable sales declined by 40% in Q3, driven by a 51% decrease in comparable transactions. The biggest burden has been felt by the US, where the comparable store sales were down 40%, vs 37% down internationally. Those stores in the US that remains open throughout the quarter China has felt a drop of 19%, thanks to a benefit from value-added tax exemptions.

The company reopened 130 net new stores, 5% y/y growth, most with modified store hours and limited seating; 61% of global portfolio came from stores in the US and China. Consolidated net revenues declined by 38% y/y due to lost sales related to the COVID-19 pandemic. Due to general reduction in customer frequency in stores, the Starbucks Rewards loyalty programme 90-day active member declined 5% y/y to 16.3m. For the upcoming quarter, Starbucks revised its guidance to lower losses than once expected.

Despite the reopening in most of the global locations, Starbucks plans to expand the convenience-led formats with curbside delivery and company's pickup locations, naturally allowing for online orders to meet evolving customer preferences. And finally, customer usage of mobile ordering increased to 22% of total transactions, up 6pps from a year ago. Overall, the Seattle-based coffee giant plans to lean heavily on its Starbucks Rewards members as it hopes to climb out of the pandemic.

Starbucks has already announced its strategies to shift development towards more drive-thru units while shifting its focus on core urban markets toward a larger selection of takeout locations and fewer traditional restaurants. The loyalty program is playing a key role and Starbucks continue to push sales through this platform. The virus has meant Starbucks have needed to adapt, and this caused them to fast-track of their futures plans to increase contactless transactions.

Nestle

Nestle experienced organic growth of 2.8% in the first half of 2020, with underlying trading operating profit margin increasing to 17.4%. For 2020, Nestle expects organic sales growth of 2-3%, assuming no deterioration in COVID-19 conditions. Retail sales have picked up by 2.7pps between H1 2019 and H1 2020, and out-of-home sales fell by 30.3pps in the same time period, highlighting the extent to which the pandemic took a toll on sales.

Americas once again had the biggest share of sales, with EMENA closely behind. There has also been a steady growth in developed markets. North America and Latin America reported mid-single-digit growth in sales, led by coffee and frozen food, with the latter seeing significant contribution from Brazil and Chile. Despite sharp sales declines in the out-of-home sector and store closures, Nespresso maintained mid-single-digit organic growth, driven by e-commerce. Overall, compared to other Nestle categories, powdered and liquid beverages saw one of the slowest organic growths in H1 2020.

Coffee remained resilient, with low single-digit growth, as a double-digit sales increase for coffee at home outweighed a sharp decline in the out-of-home sales. Starbucks products were the biggest driver in sales, growing at a double-digit rate. Nestle's broad portfolio protected the company through the lockdown.

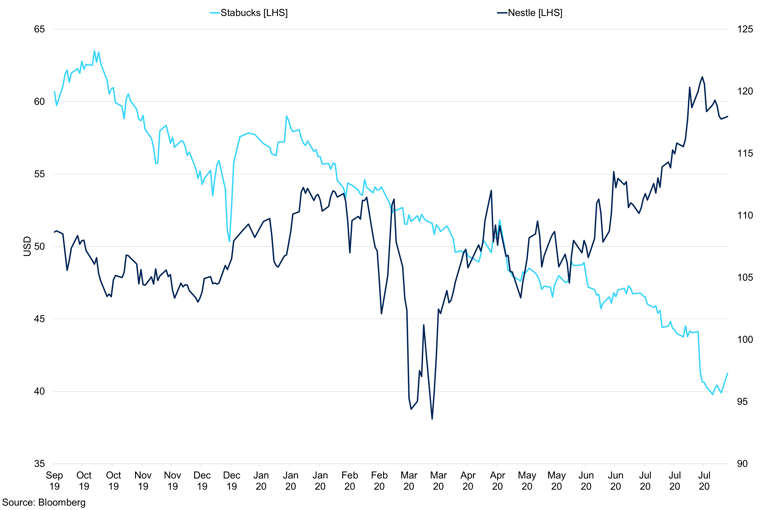

Nestle and Starbucks Share Price

Share prices have diverged since March as Starbucks has been hit by the loss of out-of-home consumption, whereas Nestle's CPG sector has supported earnings.

JDE Peet's Earnings

The business performed well in H1 2020 despite the coronavirus, with the underlying profit at 12% and earnings per share of EUR0.79. Despite the economic uncertainty, the company continued to grow, highlighting record in-home consumption. It indicated that CPG (consumer packaged goods) performance also offset away-from-home consumption. The report highlighted a recovery in out-of-home sales in June and the company hoped this would continue going forward. The threat of a second wave is becoming more prevalent, but their H1 results suggest that they will be able to adapt quickly if lockdowns are re-enforced; something we all hope can be avoided.

Total sales for H1 2020 were down 1.1% on an organic basis, with total reported sales down 2.9% to EUR3,236m. According to their company report, away-from-home sales represent 25% of total sales, and clearly, between mid-March and June, away-from-home sales were considerably down. Organic sales were 5.2% in Europe for CPG, which was offset by the prices of -0.5%. In-home consumption boosted volumes with beans and single-serve offering, benefitting the most from the change in consumer behaviour due to lockdowns. Reported sales increased 3.7% to EUR1, 652m; this also outlines our view that European consumption has remained strong. Out-of-home sales declined by 27.3% due to lockdowns, and customer consumption channels such as offices, bars, cafes, and restaurants were closed. Sales started to rebound in June but are still running at reduced capacity.

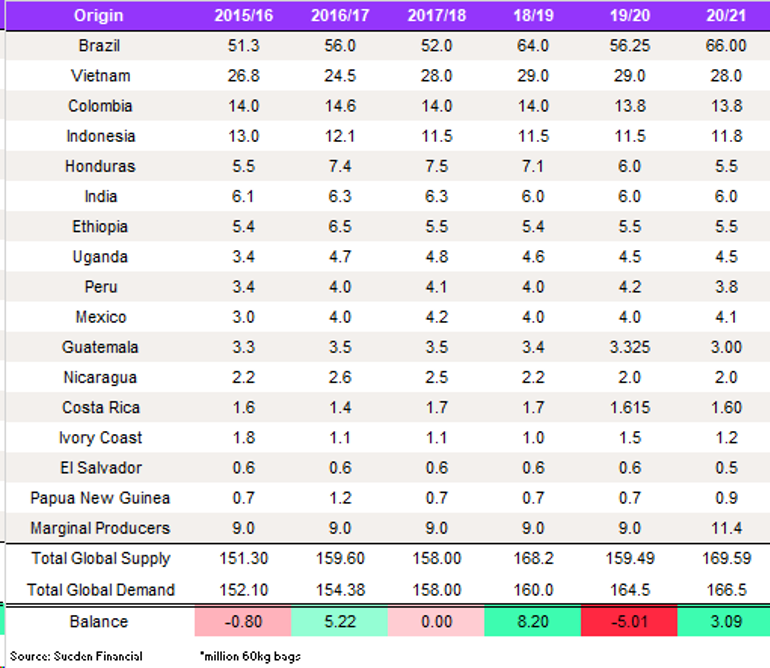

Sucden S&D Balance

S&D Balance Table

COVID-19 has had a detrimental impact on demand, especially during the lockdown months, as the away-from-home consumption ground to halt. We have kept our consumption number for the 20/21 season, despite the below analysis on the loss of demand. This is because the season is not over, and we do not know how much of the demand loss can be offset. We have seen online sales, drive-thru in the US, at-home consumption, and delivery increase significantly, helping to offset the loss of away-from-home consumption. We expect H2 to offset that loss, but it is not clear how much by. From a supply perspective, we have increased our Colombia number to 13.8m bags, an increase of 0.3m bags. Our Honduras number has also increased by 500,000 bags to 5.5m bags. This is due to stronger than expected yields; as our previous estimation was too low. This has brought our total balance for the 20/21 season to 3.09m bags.

Demand

The virus continues to wreak havoc across the globe as cases continue to rise, especially as the US has seen a resurgence in cases after coming out of lockdown too early. India, South Africa, and South America are particularly bad, and the countries have failed to flatten the curve. From the consumption perspective, the longer we see the economy run at a lower capacity in major consuming countries, the longer will the out-of-home demand will persist for. In its latest earnings call, Starbucks outlined the measures it was taking to mitigate the impacts of the virus while keeping its stores open; social distancing measures clearly reduced the number of customers in the store. Thanks to the quick adaptation to a new environment, the company has brought forward plans for contactless transactions; these include delivery, pickup, drive-thru, and curbside orders. These have been rolled out in the US, where the delivery orders tripled in Q3, with mobile orders constituting 22% of total transactions. The digitalisation is something that the company has relied on heavily in recent years in China, exemplified by its joint venture with Alibaba, making it better prepared to implicate technology in the US, and Europe.

Approximately 97% (96% in the US and 99% in China) of Starbuck's stores are open across the globe, and with sales bottoming out in April, down 65% y/y, the company closed its Q3 at -16%, outlining the resurgence of coffee consumption. The disruption to the daily routine did prompt a change to the busy store times; however, there is evidence to suggest that demand for coffee has recovered strongly in unison with the reopening of the economy. The caveat is that in coffee consumption terms, a lot of Starbucks most popular drinks contain little coffee. A Harvard Business School study looked at the restaurant industry in the US and outlined that, as of July 22nd, restaurants were running about 25-50% of dine-in capacity; however, a large proportion of those have pivoted into delivery, which could be another revenue stream in the long run. In our last report, we highlighted that the government employment benefits had supported coffee demand in the near term. Even though savings ratios have increased, we expect these to hit larger purchases such as household appliances, cars, and electrical goods. The inelastic nature of coffee will help support demand in times of recession. Still, when COVID-19 government support schemes finish and return to more normal levels, this could see consumption soften. Chase credit card data indicates supermarket sales have been positive throughout the pandemic, and their R-square correlation between new cases and lagged supermarket spending stood at 0.01, which is not significant. Chase consumer spending has recovered to -13% y/y as of July 25th, up from -40.6%y/y on March 31st; the index uses the sample of 30m US cardholders.

Online sales have been a key theme throughout Q2, internet sales soared in Q2, but as shops open, we anticipate this to have softened slightly. Amazon saw 4.9bn site visits in May alone, up 19% m/m; Walmart, Target, and Kroger all improved significantly as well. Coffee sales on Amazon were worth $1bn and have seen a growth of 37%, pods and capsules made up most of these sales, 86%, while roast and ground made up 14%. This increase in online coffee orders has helped to offset the at-home consumption, and the quality of coffee available at home has improved. Pret exemplifies this by selling their coffee blends for the at-home market, with beans now for sale in-store and online at Amazon. According to Zion market research, the ordering rate for pods and capsules grew 53% in one year, and we expect this to remain the case. The capsule and pod market is expected to grow at a CAGR of 8.2% from 2019 to 2025; this forecast was pre-coronavirus and the move to a more in-home consumption. This growth rate will cause the market to grow from $17.11bn for 2019 to $28.62bn by 2025. Single-serve coffee is expected to be a key driver for Europe and America. Indeed, European pod demand is expected to grow at a CAGR at 6.8% between 2020-2025. In Europe, demand is resilient; German consumption has been strong at 5.5kg per person per year, whereas the average in Europe is 5kg.

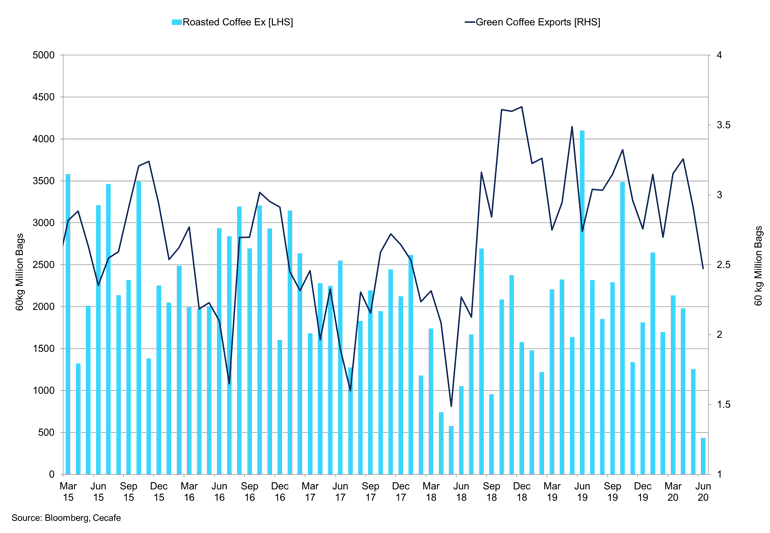

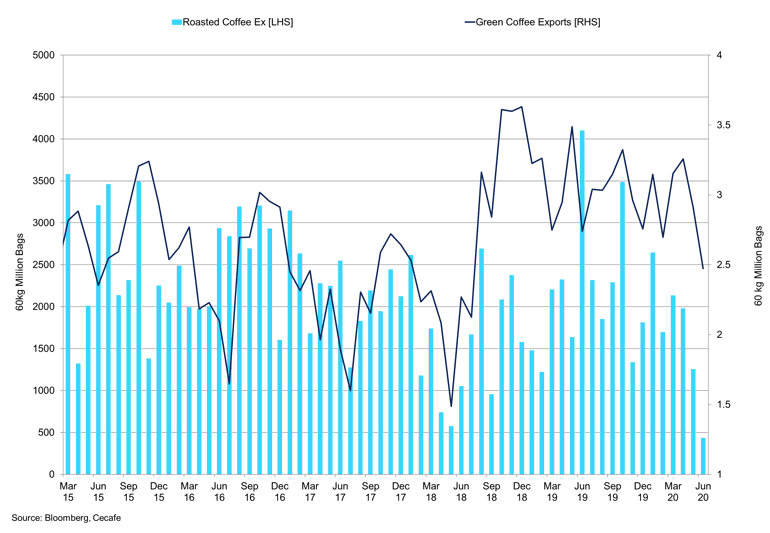

Brazil Roasted Coffee Vs Green Coffee Exports

The drop off in green exports is due to the softer Arabica shipments, as roasted coffee exports continue to weaken.

Demand in Europe has been strong so far this year, and we anticipate the second half of the year to offset the loss in demand seen in Q2, assuming there are no major lockdowns. Even so, consumers will now be prepared, and the boom in online sales will continue to grow. The pod and capsule market continues to grow; this is a much more efficient way of consumption than from a cafetierre. We have also seen strong sales and demand in South East Asia and China. A couple of years ago, we wrote that China was behind the curve in coffee demand, and while this remains the case, it is starting to grow rapidly. Starbucks suggested that it is its fastest-growing market and the use of technology that is increasing the uptake of coffee demand. Sales have improved strongly on a sequential basis and have exceeded Starbucks forecasts. As mentioned, we believe that the second half of the year across the globe will help to offset the loss earlier this year, as coffee shops and online consumption return to some sort of normality. The recyclability of pods and capsules has been called into question due to the packaging and, as ESG metrics continue to grow, it is not inconceivable that pods and capsules, which are not recyclable, see sales soften as consumer knowledge increases. Indeed, according to a Morgan Stanley survey with 10,000 respondents, 87% of people are likely to buy products with sustainable/eco-friendly packaging.

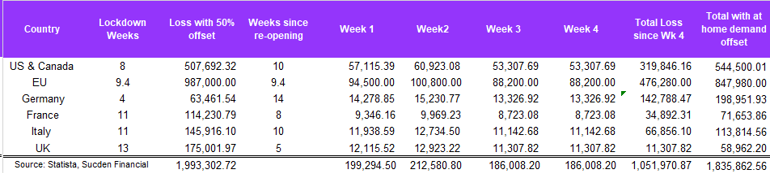

COVID Consumption and Lockdowns

In April, we highlighted the region coffee demand in millions of bags and outlined the percentage of at-home and out-of-home consumption. Demand was significantly in favour of at-home consumption before COVID-19 hit, and we expect this trend to have really kicked on during lockdown. The above data and earnings results suggest that pod demand and online sales confirm at-home consumption has been strong. We do not believe it has completely offset the loss of demand from restaurants, cafés, and hotels. Our scenarios suggested that either 30% or 50% of out-of-home consumption was offset by the rise in home consumption due to working from home. For major consuming regions, the US & Canada, and Europe, we have outlined the potential total loss of demand from the lockdowns for a 30% offset and 50% offset. The figures suggest that during lockdowns, 2,790,623m bags were lost using the 30% demand offset scenario, with 1,993,302m bags lost using a 50% offset number. We expect demand loss in producing countries, such as Brazil, due to economic hardship. However, we mentioned in our previous report that Brazil consumption is notoriously difficult to quantify due to large amounts of on-farm demand. While it remains too early to quantify the loss of consumption for a full year completely, we could see a drop off in Brazilian demand by 500,000 bags to 21m bags.

Table 1 Potential COVID-19 Demand Assessment

At-home consumption offsetting 50% of out-of-home consumption during the lockdowns and economy re-openings.

Now that coffee shops have opened again, out-of-home consumption has increased. However, using the assumptions in the calculations above, we have set a scale where shops run at 10% capacity in week one after reopening, increasing to 40% capacity by week four and then have kept level of capacity until today. This is based on a Harvard business review that indicated that restaurants are running at 25-40% capacity in America; there is a propensity for coffee shops to be running at a higher capacity. Earnings calls have suggested that coffee shops are increasing contactless transactions and deliveries, but this is not enough to offset the loss of in-store capacity. Indeed, we have also assumed that at-home consumption remained constant for the first two weeks in both scenarios, 50% and 30% respectively. In weeks preceding we allowed for a drop in at-home consumption for those who may have been more willing to go to a coffee shop, and while central business districts run at near-empty capacity, it may be the shops in more residential areas that benefit. These assumptions may mean that the consumption loss highlighted is greater than it actually is, but it will give context to what numbers we are looking at. Time will tell if in-home consumption sales tail off as coffee shops open, but it is too soon to quantify this completely; therefore, we have made the above assumptions.

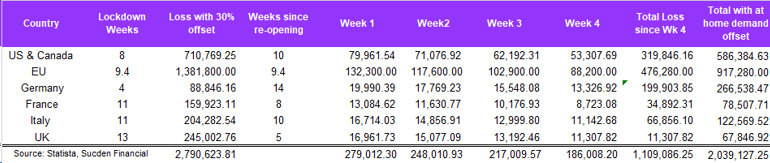

Table 2 Potential COVID-19 Demand Assessment

With at-home consumption offsetting 30% of out-of-home consumption during the lockdowns and economy re-openings.

These assumptions lead us to believe that with in-home consumption offsetting the loss of out-of-home demand by 50%, 1.993m bags were lost during lockdown; using 30% demand destruction - 2.790m bags. Since the reopening of the economies, we believe that demand loss for out-of-home consumption for the 50% scenario has been 1.835m bags, with the 30% scenario suggesting a loss of 2.039m bags. Total demand loss for the 50% scenario is 3.828m bags, with the 30% scenario at 4.829m bags. With demand in S.E.Asia and China strong, and online sales in traditionally mature consuming regions also strong, we expect to see coffee re-cooperated as consumers refill their home inventory or pods and capsule demand continues to grow. We do not expect coffee demand to be down by these amounts at year-end as consumption in H2 2020 offsets the losses earlier in the year, and our assumption for current out-of-home capacity is conservative.

Supply

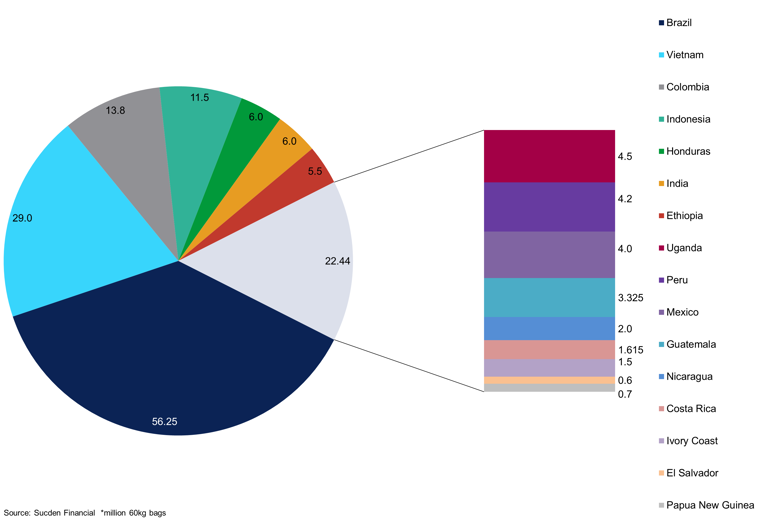

Our crop number for Brazil 20/21 has remained at 66m bags, we have seen strong export figures from Brazil throughout the pandemic, and this remains the case, suggesting the crop is large. However, as the harvest is not finished, numbers of 68m bags cannot be confirmed. The cherries have been on the trees for longer than usual, and if they fall from the tree, this will create downside to the 68m bag crops. Rain now would be detrimental to the drying process, and we believe the weather needs to remain dry until September. We maintain our ratio of 48m bags of Arabica and 18m Conillon for the season, and if there is a downside, we expect it to be in the Arabica crop. When we look at the off-cycle for 21/22, this is where the uncertainty increases. As mentioned, coffee is still on the trees in Brazil, and the longer the harvest, the higher the probability of next year's yield to be lower. We remember that this time last year we saw a very cold patch of weather which was 1 degree from causing significant damage, followed by a prolonged period of dry weather. These weather conditions increased stress on the tree, and now we have a longer harvest, and the shorter the period is between crops, the higher the probability of a lower yield.

Preliminary, the off-cycle could be 10% lower of this crop, again, we expect the majority of this drop off to be in then Arabica regions. This would mean a crop number next year of 56m bags, with 18m Conillon and 38m Arabica. The Vietnam crop looks to be softer this year, and this may put pressure on roasters to amend their blends towards Conillons. Brazil's handling of the virus has been poor, and infection and death rates remain high. This has prolonged the harvest but also reduced consumption within the country. This may increase carry-over going into the off-cycle and keep domestic inventories elevated, helping to reduce any tightness in the market going into the off-cycle. Still, there is no carry-in Brazil now. However, we see the tightness in milds, and Central American grades not semi-washed Brazilian Arabica. Weather recently has been drier, and this is worth watching, as continued dryness will impact next year's crop growth.

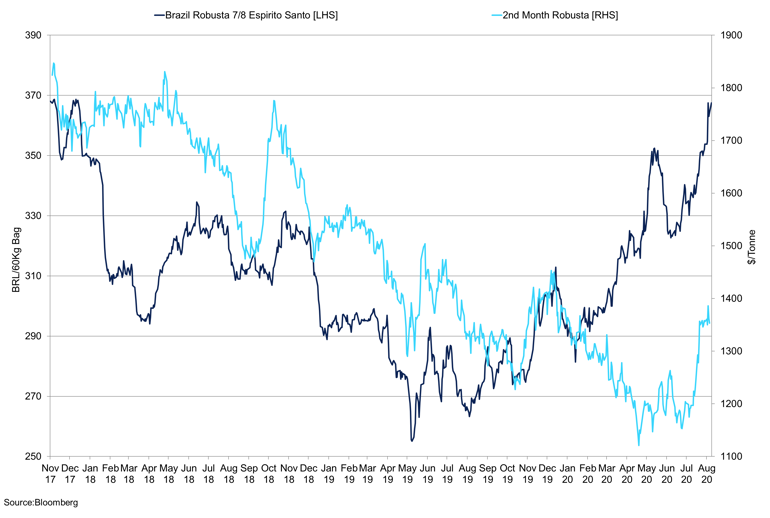

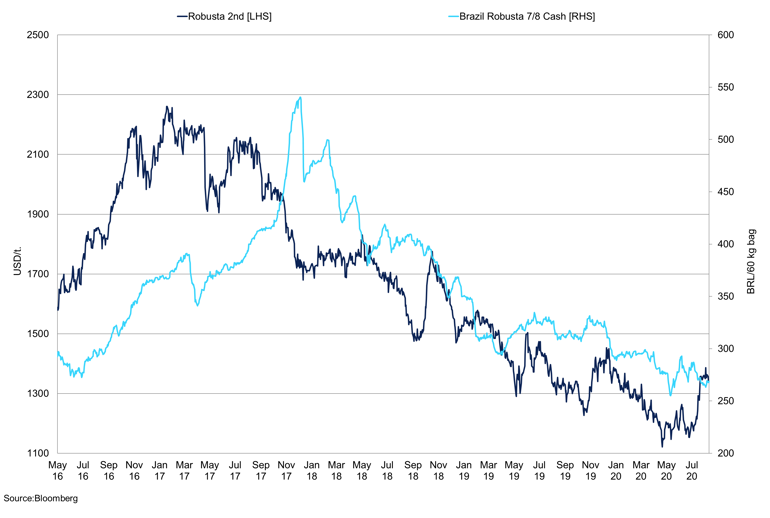

Brazil Robusta 7/8 Espirito Santo vs Robusta

London prices have rallied recently but not nearly as strong as local prices, helped by the real.

We expect the harvest to continue at the current speed; producers are well sold, but we have seen producers continued to sell as prices have rallied. However, as the dollar weakens and the flat price gathers pace, the spread between the differential and the flat price widens. Local prices have improved back towards preferential levels, and some deliveries are for 2021 and 2022. Brazil's ESALQ arabica index has increased in recent weeks back towards R$600/bag, R$562.54/bag as of August 11th. The Arabica type 7 Rio cup Paulista improved up to R$402.5/bag, an increase of 14.6% from R$350.25/bag on June 20th; this increase in local prices has improved local business. Robusta Coffee 7 8 cash price in Espirito Santo has risen 26.7% YTD to R$367.92/bag.

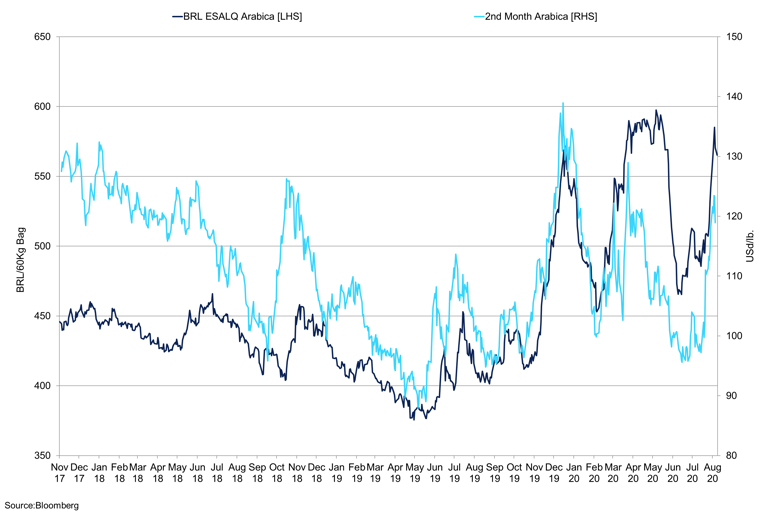

Brazil Coffee Local Price vs 2nd Month Arabica

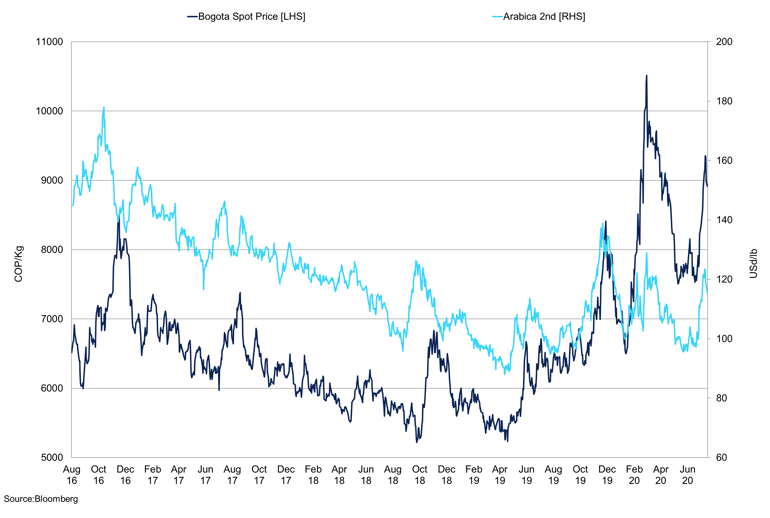

The rise in local prices has buoyed local business and producer selling in Brazil.

Local prices have improved, and the weakening of the dollar in conjunction with lower interest rates has eased any interest payments by Brazilian farmers. The weaker dollar could help with the affordability of inputs next year; we believe the dollar will remain weaker in the near term, but the election in November is a clear risk event. The lower exchange has put pressure on farmer margins; however, differentials have held steady, improving farmer earnings. We expect diffs to hold firm, and demand for Brazilian coffee to remain strong, which is exemplified by the sustained export numbers. Diffs have weakened since our last report, but we expect them to firm once again. The March21/March22 spread has tightened right in to -$4.10cts/lb, indicating tightness down the curve. We saw strong volumes in the final week of July as the curve narrowed, suggesting short covering. In our last report, we outlined that the move downwards was CTA-driven and would not be a long-term trade. We have seen an increased producer selling as the prices have rallied, and if prices push through 125cts/lb, this will bring hedges at 100-105cts/lb under pressure.

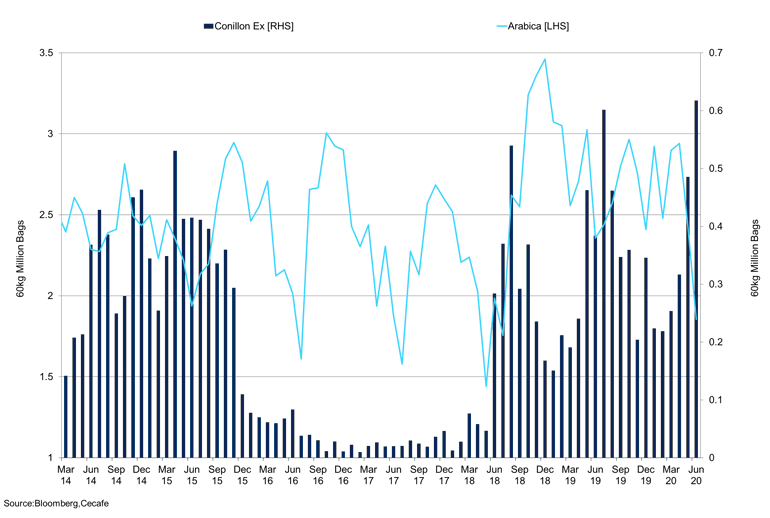

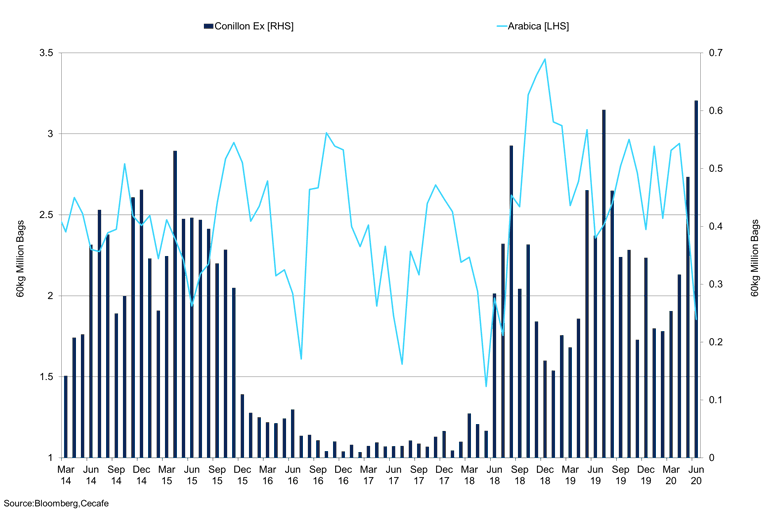

Brazil Conillon vs Arabica Exports

Conillon exports surged in June to 617,739bags, but Arabica has tailed off slightly.

Brazilian coffee shipments weakened in June to 2.80m bags, down from 3.243m bags in May and 3.63m bags in April. June's export number was below 3m for the first time since July 2018. Conillon shipments surged higher to 617,739 bags; we saw 601,684 bags exported in July last year, pre-loading data suggest July's shipments are 439,587 bags, bringing the total 2.116m bags for the year. Arabica exports declined sharply to 1.85m bags, from 2.425m bags in May. The average monthly shipments since 2018 are at 2.588m bags. Total green shipments have fallen to 2.47m bags from 2.91m bags because of the drop off in Arabica shipments in June. We expect shipments will remain steady, but in the coming months, the delayed harvest could present downside risk to exports. Roasted coffee volumes declined significantly to 433 bags in June as soluble coffee exports declined to 327,034bags, a modest decline from May to 331,559 bags.

Colombia

The differentials for Colombia have held strong above 50cts/lb, demand for Colombian coffee has been good despite the high differentials and cheaper Brazil's as there is no substitute for Colombian coffee. The Mitaca crop was reasonable this year; it was quickly accountable for by the trade due to the number of shorts and strong demand. Crop tours have been difficult due to nationwide lockdowns across the globe. Picking for the main crop will not be until next month, but reports have indicated that the crop is in-line with our estimates. The FNC has suggested that Colombian production increased by 12% in June, with registered production at 1.36m bags, up from 1.2m bags in June 2019. However, YTD production is down 8% to 6.1m bags vs 6.7m bags in 2019, for the crop year production has been steady, up 4% to 10.7m bags vs 10.3m last year. Exports have continued at a steady clip despite the pandemic, with y/y exports in June at 1.123m bags, up 1% y/y, but the exports for this coffee year are 6% down at 9.51m bags. YTD exports are down 12%. We expect to see the exports increase slightly as labour returns to the market, albeit at a reduced capacity. The country is formulating a plan to guarantee the safety against COVID-19 for the labourers, especially as the number of cases is increasing in Colombia; this threatens the harvest pace next month. We expect the main Colombian crop to pick 7.5m bags, bringing the total crop figure to just shy of 14m bags. We have adjusted our production number accordingly to 13.8m bags, up from 13.6m bags.

Colombia Bogota Spot Price vs 2nd Month Arabica

Farmers need prices to hold these higher prices to offset losses in previous seasons.

The FNC has also given a guide of what the best practices are after the harvest for Colombia washed coffee. The guide is an attempt for Colombia to keep its market share and maintain its quality and income. The recent rally in exchange prices and the strong differential bring Colombia firmly into the money. As mentioned, the weaker dollar will help with inputs costs, but the advantage Colombia has is that Brazilian Arabica's cannot substitute their coffee. The crop has been good, but export demand for Colombian coffee will keep diffs firm. We expect investment into Colombia's coffee business to continue as it looks to maintain market share, following the donations from Efico & Collibri foundations to the FNC of 100m COP.

Central America

Honduran exports have weakened in 2020; this is synonymous with the lower crop that we have forecast and the negative impact of lockdowns on farmers picking coffee. Honduran Arabica exports in June were 650,000 bags, down from 730,000 the month before. June exports in 2019 were 926,000 bags, while the average exports for H1 2020 are 671,000 bags, down 12.74% on H1 2019, which saw the average monthly exports of 769,000 bags. The four-year average is 604,000 tonnes, and we expect this year's number to be below this level. July exports are down close to 55.5% for Honduras, according to IHCAFE. Shipments have been falling steadily in the last few years after reaching 7.2m bags in 17/18, then dropping to 6.812m bags for the 18/19 season. So far, this year we have seen 4.228m bags shipped and, as mentioned, are down on the year. Our crop number for the 20/21 season is 5.5m bags; this is a 500,000bag increase since our last report. While the crop size is down, despite the lockdown and lack of skilled pickers, the crop has beaten our estimations, causing us to raise our number. It has been tricky to conduct crop reports, and there has also been a lack of skilled worker availability due to lockdowns across neighbouring countries such as Nicaragua, where workers often migrate from, which presented a downside risk to crop.

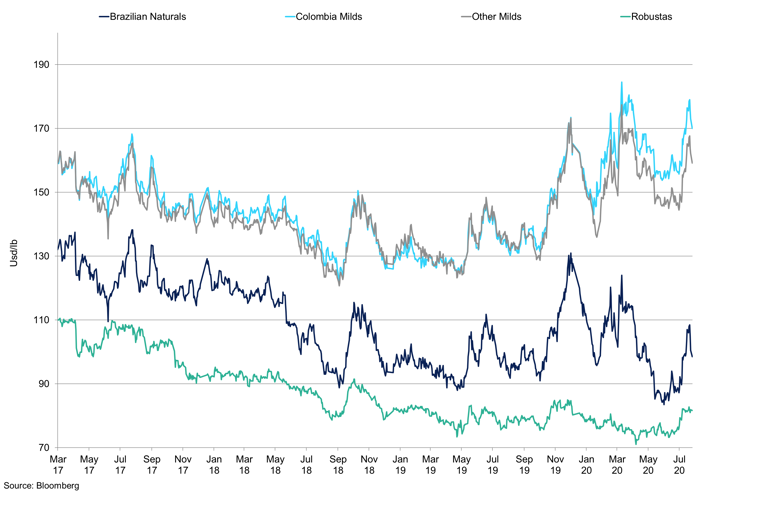

Coffee Types Price Indicator

Milds have been well supported as diffs remain strong but farmers need prices to holds above 150cts/lb to offset previous years losses.

Access to financing and capital is constrained at the time of writing for Central American farmers due to risk aversion because of COVID-19. This will act as a headwind to Honduran farmers who are trying to finance future crops and pay for inputs. Differentials have offset the weaker flat prices, but now, the exchange prices have increased in recent weeks, and farmers need prices to hold gains to recoup lost revenues over the last few years. A break towards 135cts/lb would put pressure on hedges at 100-105cts/lb. We saw a large clip of Honduran coffee withdrawn from Antwerp certified warehouses, indicating that certified stocks are still the cheapest coffee. Local business has ground to a halt, and we have seen the differential soften slightly from 30+, one headwind of exports in Honduras is the lack of container availability, this is also particularly prevalent in Peru and African countries. In other Central American countries, and Peru, we also saw significant damage to the crop, and this has presented some downside to our crop numbers in those regions. The total impact is tricky to quantify now because getting workers into the fields has been tricky to assess the total damage. In Peru, COVID-19 continues to damage progress, and we are still hearing of challenges to workers entering the fields, to picking and crop reports.

Vietnam

Recent crop tours have caused us to drop our Vietnam number by 1m bags to 28m. This is due to poor weather conditions damaging the crop; the recent rally has reflected the reduced availability in the Robusta market. We saw producers sell on the way up, which has improved liquidity in the market. In our previous report, we highlighted that the risk-reward for the Robusta market was on the upside and recommended the July 1300 call. The nature of this options expiry meant the rally came too late, but we expect price action to remain firm in the near term and the pullback in the differentials may present a buying opportunity. Diffs for grade 2 Vietnamese Robusta's have weakened to 160+, and we have heard business done below these levels. We would not buy this coffee with a differential around 140+, but if prices move towards 100+, this is where we would prefer entering the market.

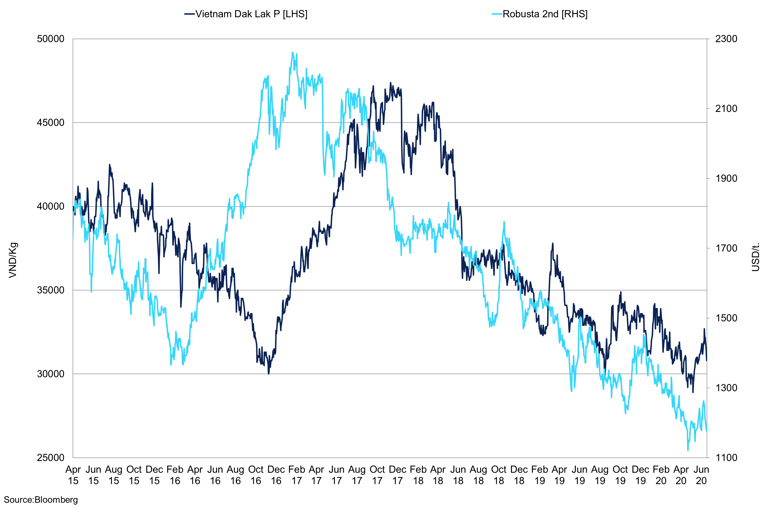

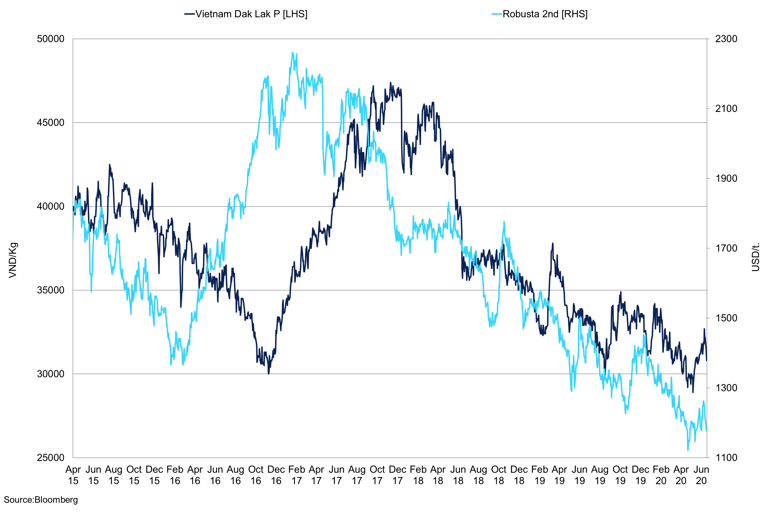

Vietnam Dak Lak Robusta Prices vs 2nd Month Robusta

The rally in local prices has helped the flow of Vietnam coffee after farmers held back coffee.

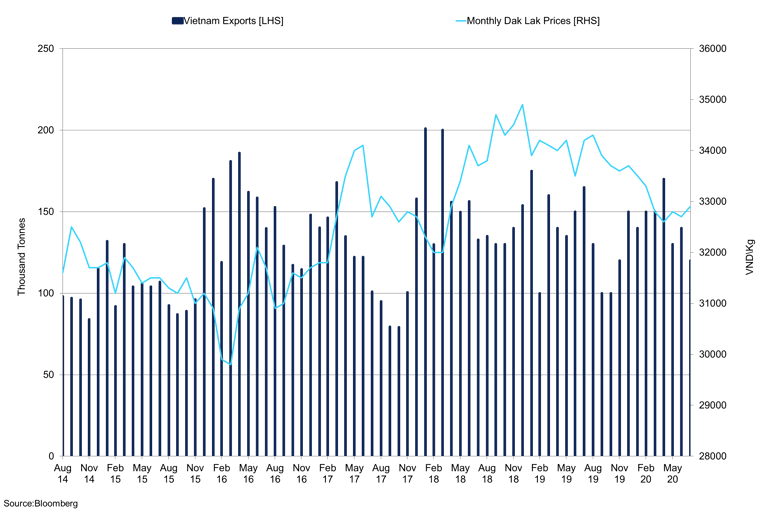

Exports have been weak even though Vietnam has managed to contain the virus well. Shipments spiked in April to 170,000 tonnes but have been falling month-on-month ever since July; exports were at 120,000 tonnes compared to 165,000 tonnes last year. The lower exports are also due to farmers holding out for higher prices, especially as local prices were below 31,000VND/kg for a sustained period of time. Now, the local price is above 33,000VND/kg like in Dak Lak, and we could see coffee start to flow again. The November 2020-2021 12-month spread has weakened after tightening into -$63/t and now stands at -$92/t. The lower crop and steady demand for Robusta beans from European roasters after the summer season should see the spread tighten. The Vietnamese crop is weaker, and this will likely present some tightness in the market and should cause diffs to firm once again. Ho Chi Minh City stocks fell in July as activity picked up in unison with the increase in local prices; stocks fell to 3,160,000, down 197,000 bags y/y and 340,000 lowers than the month before. We expect stocks to continue to fall and carry over to be minimal following the downgrade to our crop number.

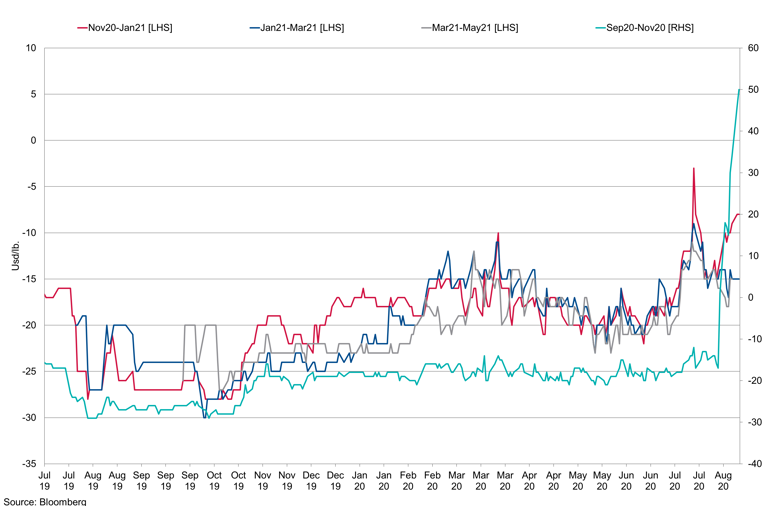

Robusta Calendar Spreads

Sep-Nov has tightened significantly with longer-dated spreads still in contango.

Inventory

We have seen a steep decline in exchange Arabica stocks, whereas Robusta withdrawals have been steadier. This suggests that this is still the cheapest coffee around; we expect inventories to continue to draw in the near term as offtake recovers and certified stocks remain the cheapest coffee around. We saw the large withdrawal of Honduran coffee from warehouse stocks and, in keeping with our previous reports, lower Honduran crop number on year on year basis will reduce the availability of Honduran coffee next year, especially if you factor in the certified Honduran coffee withdrawals. In March, Honduras coffee in Antwerp was 1.353m bags, falling to 1.167m bags at the beginning of August, but since the start of this month, stocks have fallen 12% to 1.027m bags. As of August 3rd, Arabica certified stocks were 1.437m bags, of which 1.27m bags are in Antwerp. We expect stock draws to continue and maintain our view that stocks will fall to 900,000 bags by the end of the year. Due to the softer demand picture because of the virus, the propensity for higher carryover at origin is stronger. We feel the certs are entering a very interesting phase, back in March this year the rumour in the market was industry were booking certs as protection against problems at the origin due to the COVID-19 pandemic. As we publish this report we are still aware of problems in Central and South America as we expressed earlier in the report. We have always believed the certified coffees both Robusta and Arabica are the cheapest coffees in the market place but, one has to take into consideration how much of this coffee industry can use. We may find that a percentage of the 1.437 mill bags, if they were put up for regarding, would fail, based on some of the coffee that has been graded recently.

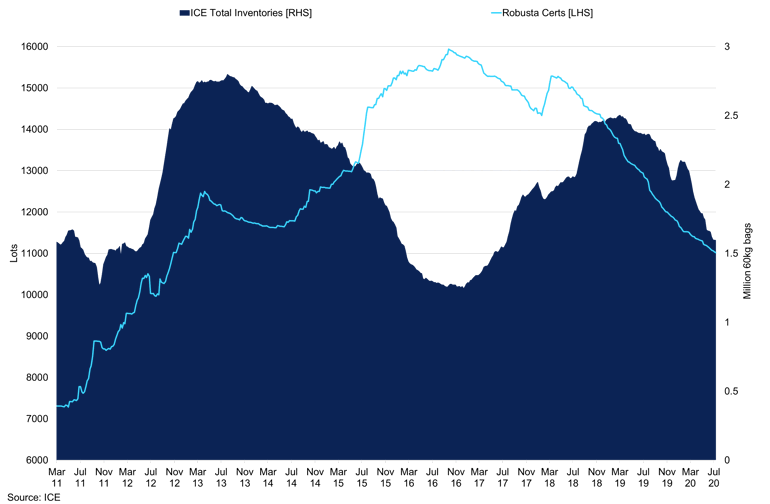

ICE Total Inventories vs Robusta Certified Stocks

Arabica certs have been falling at a steady clip as Honduran coffee is withdrawn from Antwerp.

Robusta inventory draws have been less pronounced, but we expect stocks to decline. Once again, the vast majorities are in Antwerp 6,426lots are in Antwerp, and this is where most drawdowns have been. London has seen little over 1,000 lots of withdrawals since May 19th. As mentioned above, Ho Chi Minh stocks have also started falling once again after local prices increased to preferential levels. Total inventories have fallen 26.76% in 2020 to 11,018 lots, which equates to 1.83m bags, from 15,043 lots which were 2.5m bags.

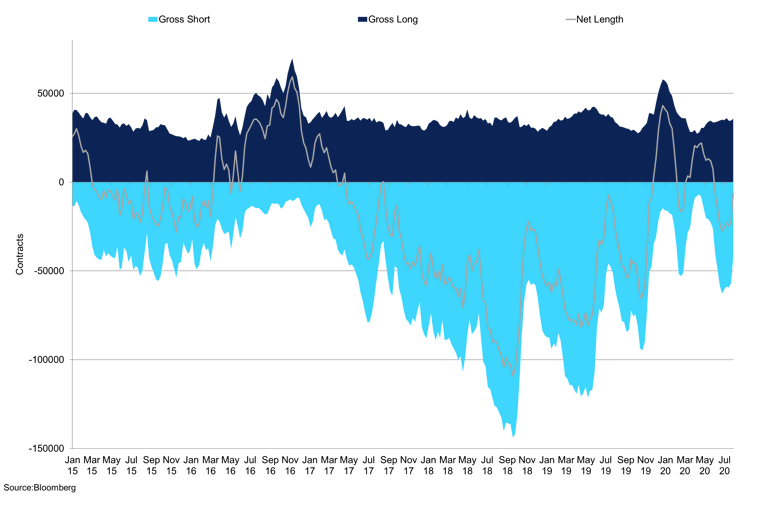

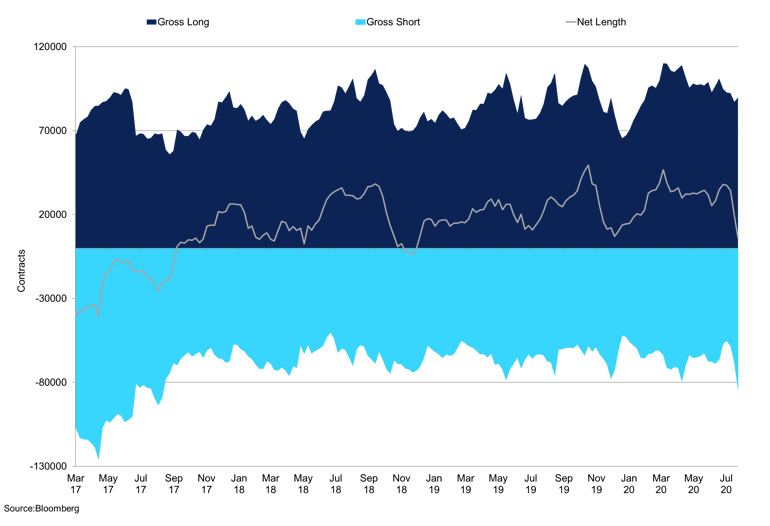

Arabica Managed Money Commitment of Traders

The recent rally saw new longs and shorts covered, however, we have given back 50% of the gains at the time of writing.

Commitment of Traders

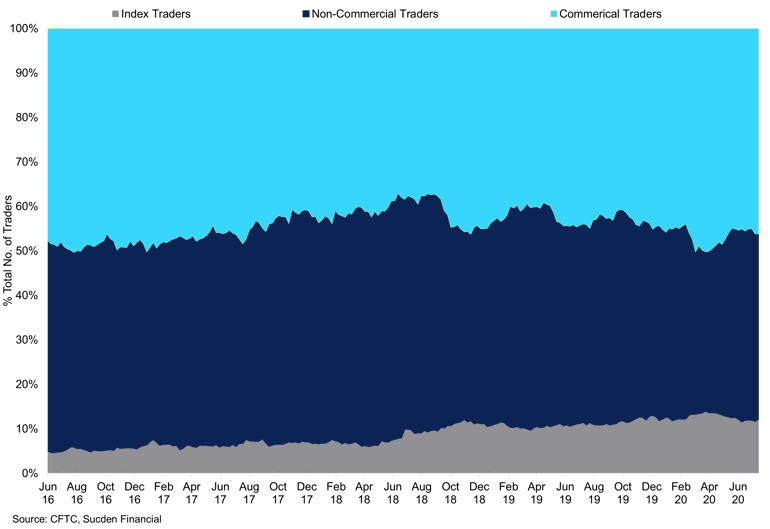

For Arabica, the supplemental commitment of traders' data shows that there was an increase in the net position by 217 contracts, to 13,010 contracts. We saw a significant reduction in the short position by 1,335, bringing the gross short to 21,293 contracts on August 14th. The recent rally saw some shorts covered and new longs entering the market. Spread contracts increased to 102,204, an increase of 22% since July 14th, and we expect this to be as a result of the spread tightening. The Sept-Dec spread tightened into -1.65cts/lb as of August 10th. From the commercial perspective, while we did see some buying at higher prices, the net position increased again to -72,407 as of August 14th, falling from -25,989 contracts at the beginning of July. We saw a reduction in the gross longs by 2,760 as prices rallied to -72,407 contracts on August 14th from 129,882 as of July 21st. Indeed, we also saw a large increase in the number of shorts as commercials sold into the rally. The gross short reached 189,057 contracts as of August 4th, an increase of over 24,000 contracts from July 21st. Since the market has retreated from the highs, we expect some of the longs to have fallen, and increase in shorts. The commercial position makes up over 50% of the whole COT traders combined; however, the non-commercials' have moved the market in recent months. The total notional value of all longs and shorts in the market reached 21,083,128,538 as of the end of July; this is above the rolling average of 19,058,486,185.

Arabica Supplemental Percentage of Total Traders by Category

Commercial Traders still make up the vast majority of the market despite CTA driven moves.

The disaggregated commitment of traders, on June 26th Producer/Merchant gross long and short, were 119,552 and 140,911, for the managed money 35,141 and 62,706, respectively. Gross shorts combined was 203,617, which equates to 57.691m bags, when we compare this to August 8th 2020, the same calculation was Producer/Merchant gross long and short were 111,679 and -162,131, while the managed money gross long and short positions were 42,312 and 25,894, respectively. The gross shorts combined was 188,025, which equates to 53.273m bags. When we strip out the managed money position of 25,894, and 5,000 lots that were re-certified from the gross short 188,025 this leaves 158,000. This is partly option related, but we see the majority of this as Brazil hedging.

Robusta Producer/Merchant Commitment of Traders

The gross long for producers and merchants have declined in recent weeks as the rally set in.

For Robusta, the net producer/merchant position was -8,332 as of August 14th; this was a net change of -7,490 contracts week-on-week, the net position has fallen from 34,327 contracts a decline of over 100%. The number of gross shorts fell by 13,251 contracts to 77,431, since July 14th gross shorts have increased 40% from 57,960. This shows that producers were heavily selling into the rally, as during the same period we have seen longs fall by 25% from 92,287 to 69,099, however, the majority of this was between August 4th and 11th when gross long fell by 20,741. The managed money commitment of traders for futures and options has seen a significant reduction in the net short -41,654 contracts as pf July 14th to a net long of 3,467 contracts as of August 14th. This was as shorts were closed out, as the gross short declined to 8,071 from 51,990 contracts in the same period. Longs have been steadily increasing since the start of May but reached a year to date high of 11,538 contracts as of August 14th. Sentiment in the Robusta has shifted, outlined b the backwardation in the spreads, and the recent rally in the flat price.

Appendix

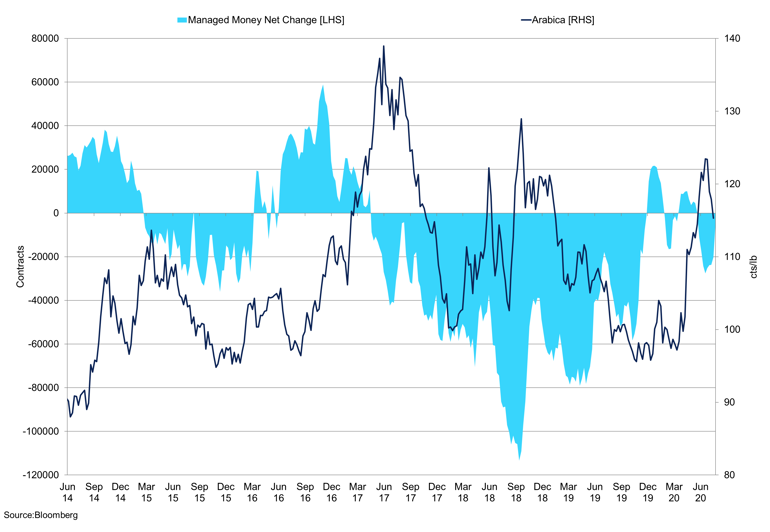

Managed Money Net Position vs 2nd Month Arabica

Brazil Conillon & Arabica Exports

Brazil Roasted vs Green Coffee Exports

Vietnam Dak Lak Robusta Price vs 2nd Month Robusta

2nd Month Robusta vs Brazil Robusta 7/8 Cash

Vietnam Exports vs Monthly Dak Lak Prices

Global Coffee Supply Calendar Year

Coffee Global Supply 2020/21

Coffee Global Supply 2019/20

Coffee Global Supply 2018/19

Coffee Global Supply 2017/18

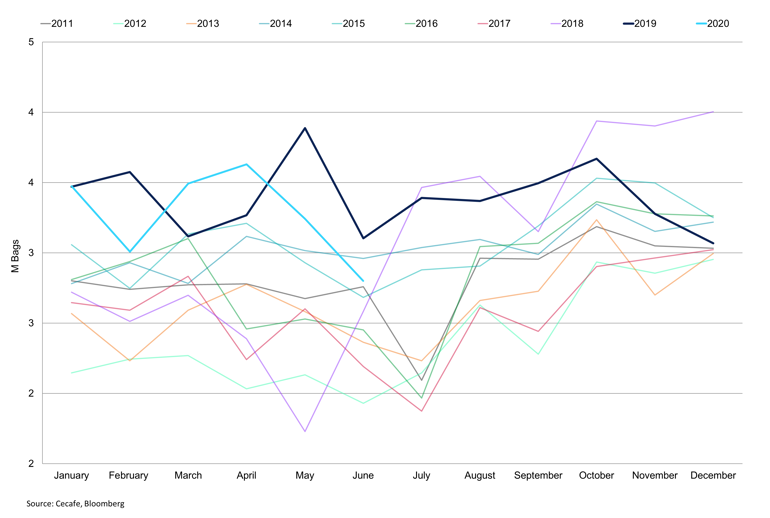

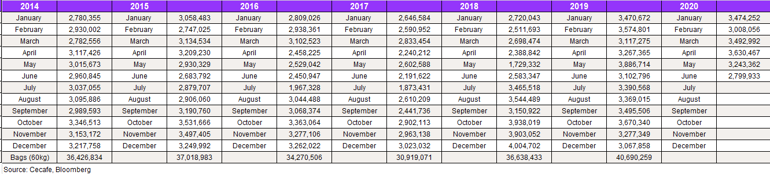

Brazil Exports

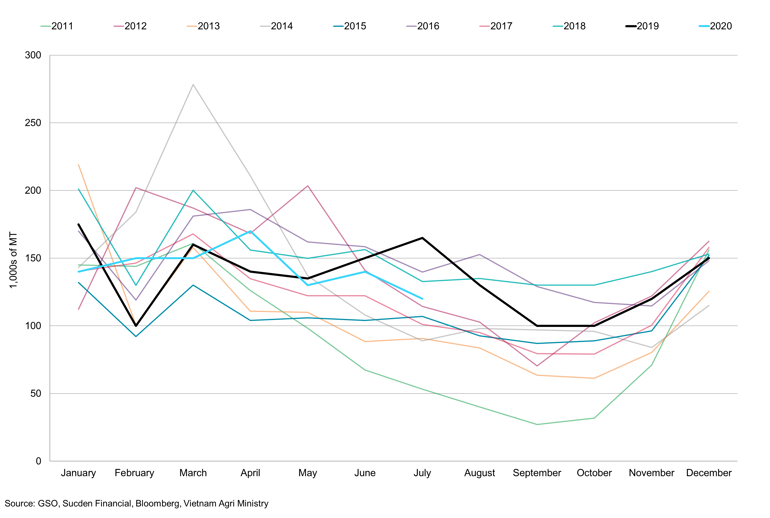

Vietnam Exports

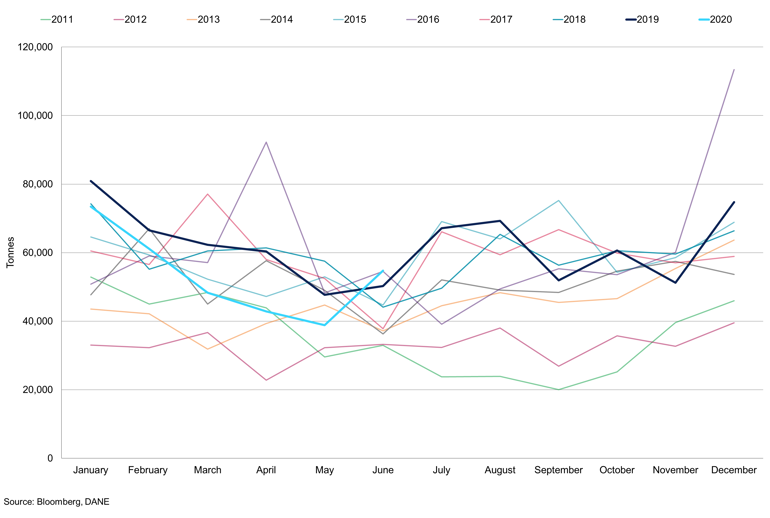

Colombia Exports

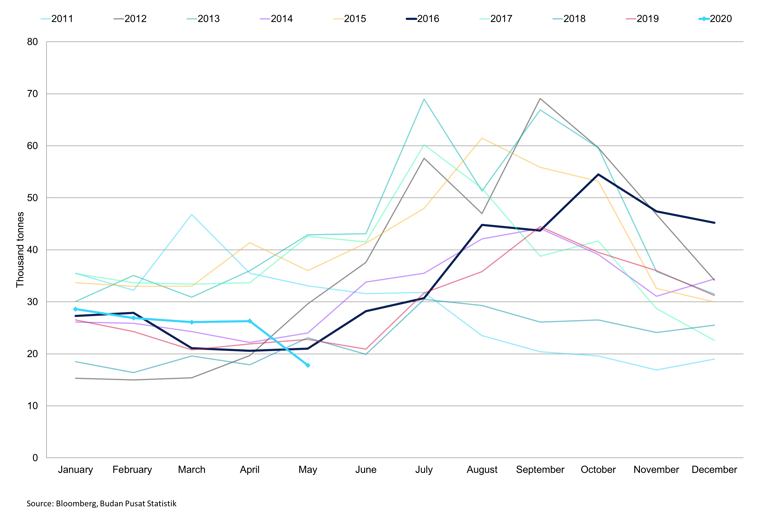

Indonesia Exports

Brazil Coffee Exports Calendar Year

Vietnam Coffee Exports Calendar Year

Indonesia Coffee Exports Calendar Year

Colombia Coffee Exports Calendar Year