Following the release of our Crop Update last month, our analysts provide a more in-depth breakdown of the S&D balance, whilst looking at the bright spots for consumption post-COVID. Brazil shipments are starting to fall, but the deficit has not yet shown its cards. European economic growth lags behind the U.S. and we expect this to remain the case due to poor vaccine policy management, causing consumption growth in the bloc to be weaker.

Global Economic Review

Global equities have recently gained ground, continuing to break new records. Vaccine optimism and the Fed's decision to keep its long-term outlook unchanged eventually outweighed concerns that stronger-than-expected economic growth would alter the monetary policy stance. The UK and the US are making good progress with their inoculation programmes, as they both plan a countrywide reopening in the second half of the year. However, virus mutations still present a risk to the healthcare system, especially those that are not easily detected by standard tests. If vaccinations prove to be effective against these variants, we should see limited impact on activity levels, although this depends on the level of restrictions in place. Therefore, the ratio of vaccinations to the adult population remains a key metric to track the nation's success in preventing another spread of the virus.

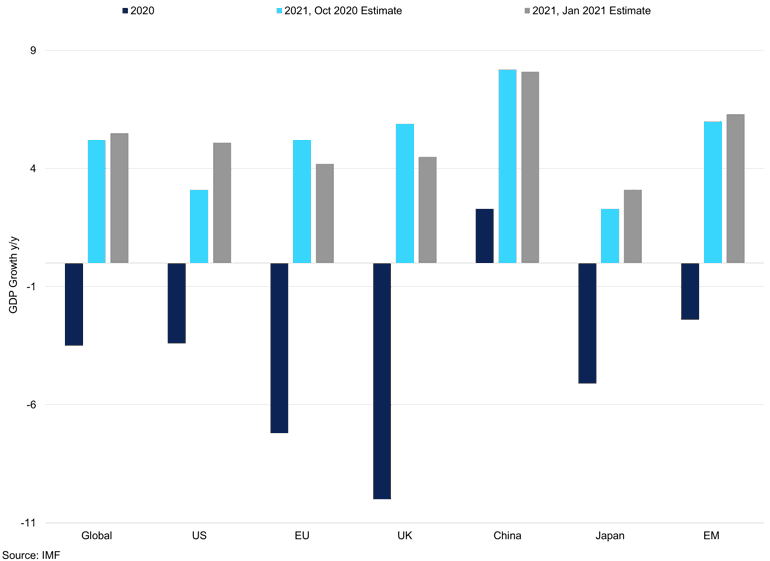

IMF 2021 Growth Projection

Most 2021 estimated have improved as countries began their inoculation programmes.

On the macroeconomic front, manufacturing surveys continue to show solid momentum despite some lockdown measures still in place, aided by extended fiscal support, which is boosting demand for durables. To accompany the recovery, both fiscal and monetary policy support will remain significant. The ECB has sped up the pace of its bond-buying programme, and other countries across the world continue to support the households, albeit at a slower rate. The approval of President Biden's fiscal programme should boost the US recovery with positive spillover effects. However, government spending is creating a concern about heightened debt levels and possible tax hikes. As the recovery progresses, the attention will later shift to a change in the central bank monetary stance. While some countries, such as the US, promise continued support for the economy in the form of low-interest rates, others are considering tightening of rates, especially as inflation expectations rise above country thresholds. In the meantime, we expect the yields to continue to rise and the dollar to weaken further.

The US

The markets continue to touch new highs as optimism over the economic recovery fuels the rally. Cyclical sectors, such as energy, financials, and industrials, performed strongly, whilst more defensive sectors lagged. A tame inflation report and promises of record low-interest rates until 2023 were contributing factors in the market's gains, but the headliner was the passage of President Biden's stimulus bill. From the vaccine front, the US administered a new record high of nearly 5m doses on March 13th, and, the daily count of new cases resumed its declines. As the number of vaccinations continues to grow, and some restrictions in the country are slowly lifted, we see the mobility changing gradually. According to google mobility trends, while the retail and recreation index is still 11% below the baseline, the level is much higher than seen in February. The same goes for mobility in parks, but that could be attributed to warmer weather conditions.

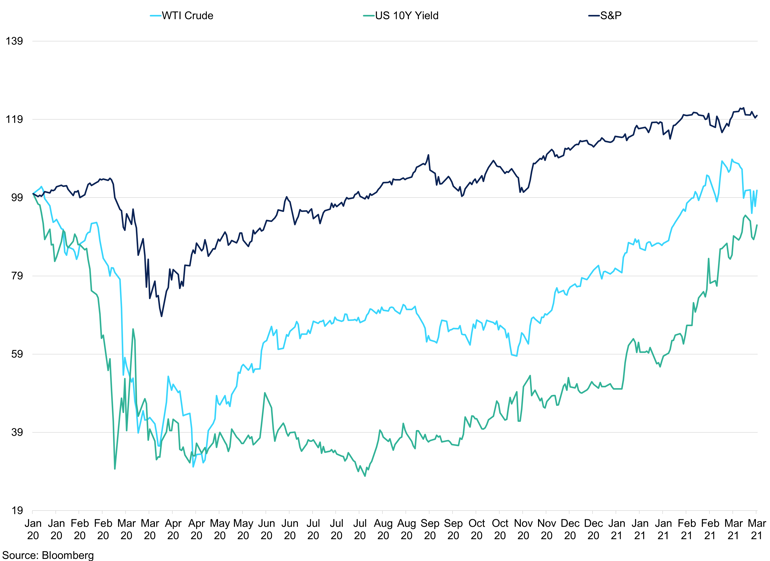

WTI vs US 10yr Yield vs S&P

Inflation expectations continue to drive the yields to levels seen last year.

In the meantime, rising Treasury yields along with expectations of higher inflation in the future continue to drive the bond markets. At the time of writing, the 10yr US Treasury yield is at 1.75%, roughly at the same level as a year ago and the highest it has been in a year. This rally was driven by two factors: the growing inflation expectations by the end of the year that will bring in higher borrowing costs and the continued injection of cash into the economy. Indeed, the interest rate on 30yr mortgages has risen, although it still remains near a historic low. The latest factor contributing to the recent rally was the Fed decided to hold the dovish line as Fed signalled zero rates through 2023. Indeed, the Fed's Chairman Jerome Powell stated that the economy has a long way to go until full economic recovery. We expect that inflation expectations will continue to drive the short-term sentiment in the US equity markets, but as the number of vaccinations continues to grow and the restrictions are continued to be lifted, the markets should be biased on the upside.

From the stimulus front, the US government passed another round of stimulus support, worth $1.9tr, as a means of continued support towards consumers and businesses. The impact from the release of the previous stimulus package has been clear through the January report on personal income and expenditures. Personal income increased by 10%, with personal consumption up by 2.4%. Retail sales soared in January, increasing by 5.3% m/m, up from -0.7% in December. While household spending increased significantly, the majority of the increase came from additional personal savings and was disproportionally focussed on durable goods, with services still far behind. Regardless, the savings rate increased from 13.4% in December to 20.5% in January, the second-highest level since the beginning of the pandemic. Therefore, we expect that the passing of the latest bill to lead to similar results, given that the economy remains in the state of lockdown. Increased funds might be saved or spent on durables, with the former adding little to increasing inflation expectations.

On the other hand, to calm the fears of rising inflation, the recent data by the Labour Department reported that the core CPI increased by only 0.1% m/m in February, below expectations. Core producer prices rose in line with the expectations by 0.2%, well below the January jump of 1.2%. The talks of pent-up consumer needs is what is driving the rising inflation expectations. This theory is supported by consumer response to the passage of stimulus bills along with a lift of lockdown restrictions. Indeed, previous data shows retail sales surge after the before-mentioned factors. The question is how long this can last. We lacked the information last year as lockdown restrictions came back into place during autumn periods. February sales fell by 3.0% m/m, most of it attributable to severe weather conditions in much of the US, however the passing of the recent stimulus bill is likely to drive the sales up in the March period.

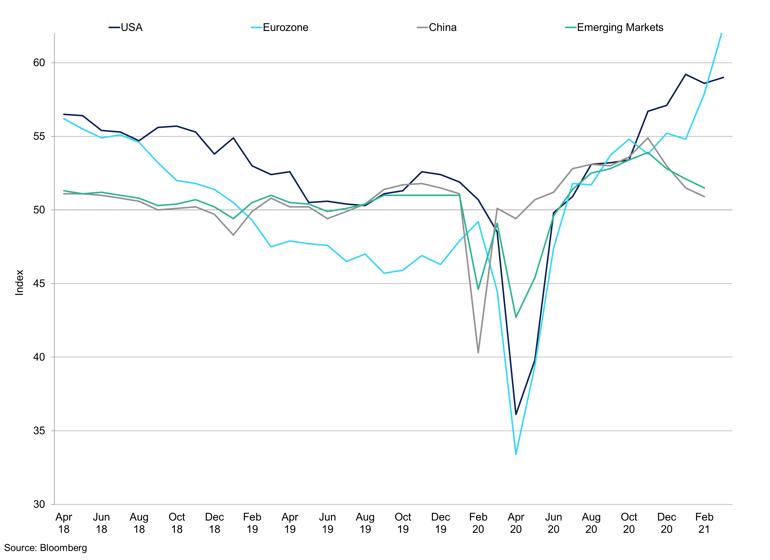

US, EU, China and EM Manufacturing PMI

Manufacturing Performance is beating record highs, however, supply chains issues prevail.

The PMI indicators are surprisingly high in the US. The Markit service index reached 59.8 – a record high – in February, indicating a level of strong growth. This could be attributed to a moderate relaxation of economic restrictions in the country. Export of services remains low; however, domestic employment by service providers continues to grow. The manufacturing industry is also strong, with the latest PMI figures at 58.6. Both sectors of the economy benefitted from the economic stimulus, declining infection rates in tandem with a rising number of vaccinations. With the newly released stimulus check as well as the continued lift of restrictions, we expect to see a similar trend in the upcoming months. This improving sentiment seemed to be supported by the University of Michigan's preliminary gauge of consumer sentiment for the March period, which rose by more than expected and hit a year high of 83.

Europe

The eurozone economy has entered a double-dip recession, after the huge contraction of activity in Q2 2020, followed by a strong rebound in the third, growth again turned moderately negative in the fourth quarter. To support the growth in 2021, the European economies will continue to receive government support, with more fiscal support to households and businesses, thereby helping to stabilise the economy against disruption in key industries. However, as we approach the end of the year, the EU does not expect economic growth to reach pre-pandemic levels, while, at the same time, expects the stimulus measures to be removed.

This begs the question: is Europe going to face slower economic growth than it would have if the economic support was not taken away by the end of this year? This debate is opposite to the one in the US where investors worry about the excess of support provided to the economy that could overstimulate the economy in the coming years. This argument was one of the main factors leading to the rise in Treasury yields. While Christine Lagarde supports the view of additional support measures, countries, such as Germany, are likely to remain averse to accumulating more debt. The pace of the support will also depend on the rate of vaccinations across the bloc. While absolute numbers remain one of the highest in the world, the ratio of vaccinations to population lacks a similar pace. Likewise, while countries such as the UK that are seeing the effects of effective vaccine distribution have already planned the roadmap out of the pandemic, most of the countries in the EU are still playing it by ear.

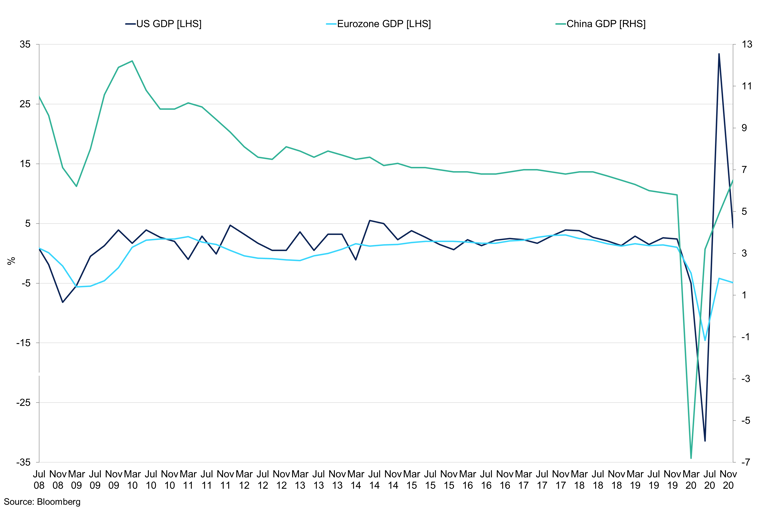

US, EU, and China GDP Growth

Economic growth softened in the last quarter of the year due to reimposed lockdown measures nationwide.

Europe's manufacturing side has shown considerable strength in the last couple of months. This is evidenced by the latest PMI figures released for the February period. The manufacturing PMI increased to 57.9, a record high, with Germany and France leading the way. The stellar performance reflects the continued strength in exports demand, especially from China. At the same time, the bloc is experiencing supply chain disruptions along with delivery delays and rising input prices. There is a potential for near-term disruptions, with companies finding themselves short of raw material. While manufacturing is helping to offset the setback in services, the composite index remains in the negative territory. The services PMI continue to underperform, with the latest statement seen at 45.7, a slight increase from 45.4 in January. Ongoing lockdown measures continue to impact the service industry, however, with restrictions easing closer to summer, we could see companies become more upbeat about the recovery prospects. Assuming vaccine rollouts can boost both the manufacturing and the service sides, we could see a strong recovery in economic growth in H2 2021.

In the meantime, the virus situation remains a potential threat, as countries such as Italy and Germany either reimpose or remain under severe lockdown measures, after the number of infections continues to rise. The vaccinations efforts continue to suffer setbacks as some vaccines, such as Astra Zeneca, spark fears over possible side effects, and the distribution side remains under pressure. Indeed, the EC president Ursula von der Leyen admitted to a delay in the vaccine rollout, setting a new goal to vaccinate 70% of the adult population by summer.

China

While most of the focus has been on the fiscal policies in both the US and the EU, China's attitude has also undergone a recent change, as local government debt poses a great risk for the economy. During the pandemic, China undertook a form of fiscal support different to its Western counterparts, as local governments and state-owned enterprises borrowed heavily through bond issuance. This rise in debt helped to fund investments that helped stabilise the economy during periods of stress. The government estimates that about a quarter of China's provinces now use more than half their revenue to service their debts. This poses the question of whether the central government will rein in the fiscal stimulus, potentially implying negative consequences for China's growth.

While the officials worry about fiscal policy, there are clear indications that the Chinese economy is decelerating. The PMI figures, in particular, point to that deceleration, with the manufacturing index falling from 51.3 in January to 50.6 in February, a moderate growth indicator. The decline in recent months reflects the continued restrictions in the rest of the world suppressing demand. Indeed, the index for export orders indicated a decline. Meanwhile, new outbreaks of the virus in northern China led to economic restrictions that had a negative impact on domestic demand. Likewise, China's services PMI fell from 52.0 to 51.5 in February, a low last seen in April 2020. While Chinese business optimism improved, there was a significant decline in export orders and a deceleration in domestic orders, in line with manufacturing. There was also a slowdown in hiring by service enterprises.

A small rise in new cases in the parts of Northern China had led to come mobility restrictions during the national holidays in February. We believe that while economic performance is moderating, it is unlikely to derail the strong V-shaped recovery, driven by the implementation of the vaccines throughout the country, as well as improved export demand from developed countries that are already seeing the benefits of vaccinations. At the time of writing, the markets are more concerned about the prospects of reining in the fiscal stimulus to curb the risk from rising house prices.

The renminbi continued to appreciate against the most peers, supported by the increased growth gap between China and the rest of the world. More recently, the capital inflow in China has been supported by a wide interest rate differential. Given the continued rise in yields in the US, that differential would decline, and impede capital flows to China. In turn, that could put downward pressure on the local currency, which would be inflationary. In the meantime, China's CPI declined by 0.2% y/y in February, while the PPI jumped by 1.7% y/y – the fastest since 2018. Recent reports of swine fever in parts of China have raised concerns that it could lead to higher pork prices, similar to the increases we saw in 2019-2020. However, policymakers have previously brushed off inflation caused by soaring pork prices as a reason for concern.

In other economic readings, China's merchandise exports for February surged about 154.9% year on year in US dollar terms, while imports rose 17.3%, according to customs data. Both sets of trade data beat economists' expectations and were attributed to last year's coronavirus-depressed levels. Even so, most analysts viewed China's underlying trade performance in the first two months of this year as remarkably strong across the board.

Brazil

Brazil's GDP contracted by 4.1% in 2020, the biggest annual recession since the beginning of recording in 1996, yet still one the most resilient performances in Latin America. In the latter part of 2020, the economy bounced back, growing by 7.7% and 3.2%, respectively. Household consumption supported the growth in both quarters, helped by the government welfare programme, which was worth more than 8% of Brazil's GDP. Employment continues to recover quarter-on-quarter; however, it still remains near record highs. In 2020, nearly 14m people were unemployed and 31m working in informal jobs with no social safety net. While the economy managed to avoid the worst economic forecasts, the pandemic still impacted the nation's growth severely and continues to dim the outlook. While we do expect the economy to return to an accelerated recovery period later on in the year, in the meantime, the rise in the number of virus cases and the acceleration of inflation expectations sets the country for significant deceleration. The economy is expected to grow between 3.6% in 2021, according to the IMF.

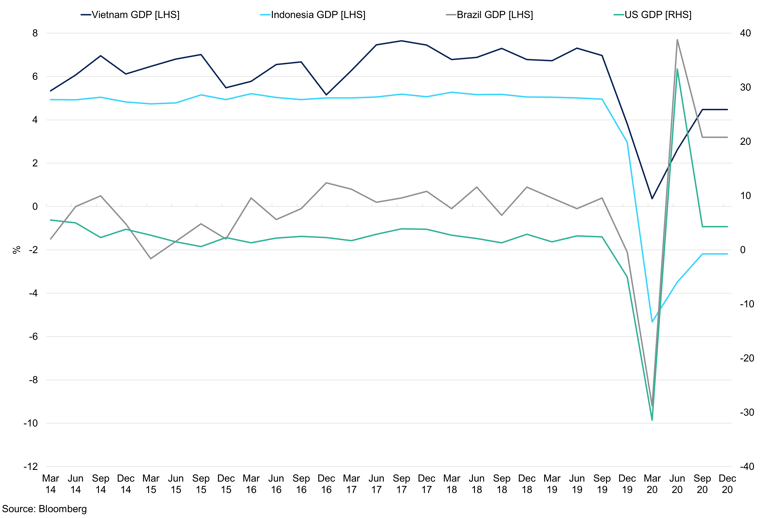

Producer Economies vs US GDP Growth

Vietnam and Indonesian GDP improved in the last quarter of the year due to continued lockdown restrictions.

The number of COVID-19 cases continues to surge, beating new highs, while the ICU occupation rates have surpassed 80% in 18 states, a critical level for the healthcare sector. Many state governments began pushing for tighter restrictions across the country; however, Bolsonaro has forcefully opposed these measures. President Bolsonaro’s rule came under bigger scrutiny later, as hundreds of leaders and economists blasted his handling of the crisis and call for a new policy approach. This comes at a time when his disapproval rating is at a record high, heightening the probability of tough campaign re-election next year. Indeed, a rise in new Covid-19 has forced the government into a fresh round of fiscal stimulus. In turn, Brazil approved an $8bn emergency aid package in March to help deal with the consequences of the second wave of infections in the country. The package, which is considerably smaller than the $50bn stimulus passed at the begging of the pandemic, was welcomed as it provided additional support needed for the households while also having a limited impact on the country's debt levels. The rollout of vaccines is another important factor. Despite a generally impressive record on vaccination campaigns, Brazil has struggled to roll out the jabs, hampered mostly by a shortage of supplies from China. While Brazil has the highest number of cumulative vaccinations in the world, edging close to 14m, the ratio of vaccinations to 100 people still remains low, in line with the world average. The health ministry said it had contracts for 365m vaccine doses, after signing for an additional 54m vials from China, and hoping to conclude a deal for 10m doses from Russia.

Brazil's inflation surged to a four-year high of 5.2% last month, and bond market forecasts for price increases are nearing the upper-bound of the central bank's target range of 5.5%. The government is set to boost consumption through another round of cash handouts of as much as $7.9bn, after injecting $57bn last year, threatening more price pressure. This has led economists to bet on a weaker currency, faster inflation and higher interest rates, according to a central bank survey. For 2021, the CB survey showed expected inflation for 2021 to shot up to a new high of 4.6%, significantly above the bank's target of 3.75%. It is the 10th rise in a row and is accompanied by an expectation of higher interest rates. Indeed, the Brazilian central bank is expected to deliver a 50bp rate hike on March 24th to shore up local currencies. Likewise, we have seen CB stepping up a pace of FX purchases to calm the markets that were moved by turmoil in the inflation expectations. Central bankers are staring down a weakening currency that's fuelling faster inflation but also mindful that being too aggressive with their first interest-rate hike in six years could curb desperately needed economic growth. As a result, they pumped the equivalent of $3.2bn into the market. The strategy worked, helping the real break a four-week losing streak while also fuelling a debate on whether the interventions were aimed at easing pressure for a more aggressive cycle of rate hikes.

Indonesia

For the year 2021, the IMF forecast the region to grow at 4.8%, versus a decline of 2.1% seen in 2020. However, it also suggests that income per capita in the ASEAN-5 economies will still be 6% lower in 2024 than the pre-pandemic levels. Indonesia was reluctant to take action against COVID-19 that would undermine the economy in the short term, relying on the effective health response while imposing minor economic restrictions. The country experienced a shallower recession than other South East Asian economies, however, still failed to contain the spread of the virus. At the time of writing, Indonesia administered 273m doses of the vaccine, which is 2.1 out of 100 people in the total population. To accelerate the adoption of the vaccine, the government has made it mandatory for all eligible citizens to take the vaccine.

While the fiscal response in the region was no match to its western counterparts, it has been very expansionary, especially when compared to the previous crises, and has played a crucial role in maintaining household incomes through the pandemic. While this current crisis has required fiscal policy to play a leading role, the actions of the central bank in the region were also crucial. Indonesian CB stepped up to purchase significant quantities of domestic government bonds in the secondary market along with directly finance a large part of the government's budget deficit.

Maintaining adequate macroeconomic support will be crucial. The prospects of higher global interest rates in the future, especially when the tightening of the monetary policy is before than previously expected, could significantly hamper borrowing costs and put pressure on the local currency that will make it harder to maintain the expansionary policy stance needed for recovery. This is especially worrying following the destabilising of Indonesian financial markets in 2013 prompted a sharp tightening of policy rates.

In February, Indonesia's CB cut its benchmark interest rate to a record low of 3.5%. It has also lowered its growth outlook amid fears of the resurgence of COVID-19 cases. Inflation is forecast to remain low, and the rupiah's maintained stability. With room for further cuts limited, the bank could rely on alternative measures like quantitative easing and macroprudential policy to boost growth. The economy's growth fell by 2.07% in 2020, the level last seen in 1998 during the Asian financial crisis.

Policymakers are worried about Q1 2021 growth, as additional curbs were reimposed in the country to maintain the spread of the virus. Recent economic indicators point to a worsening environment. Retail sales continue to decline, with the latest reading of -16.50% in February; consumer confidence also remains near multi-year lows at 85.8, falling to recover after a fall seen in March 2020. The trade side, however, is seen improving, with exports and imports rising by 8.56% and 14.86% in February, the latter is a November 2018 high. With US yield on the rise, the CB is less likely to trim its policy without undermining the relative yields of domestic financial assets. For 2021, the bank forecasts a growth of 5.3%, which has been downwardly revised, even as the vaccine rollouts boost the global economic outlook. Consumer prices rose by 1.55% y/y in January, below the 2-4% government target, and economists expect† inflation to remain weak in Q1 at 1.62%, down from a previous estimate of 1.82%.

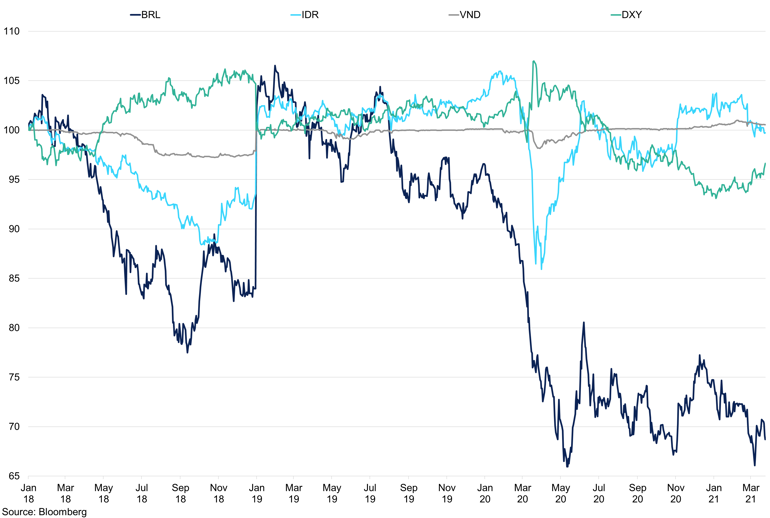

Producer Economies Local Currency vs Dollar

The Brazilian Real continues to suffer, as it struggles to recover from May 2020 levels.

Vietnam

Vietnam's economic growth throughout the pandemic has been a stellar example for South-East Asian economies. Indeed, it is one of the few economies to experience positive growth in 2020, which was driven by efficient and successful public health response. For 2021, we believe that the key to a countrywide recovery will remain weak unless the spread of the virus is not under control. In this respect, the regional outlook remains promising, especially as Vietnam managed to control its biggest wave so far. However, new and more contagious COVID-19 variants are still a threat, and vaccine rollout in emerging economies is likely to be slow. The rapid suppression of the second wave of COVID-19 cases in January has helped to support Vietnam's outlook for economic recovery this year, according to the World Bank.

Vietnam's fiscal response constituted around 3% of the GDP in December 2020, according to the IMF, well below the global average of 13.5%. Further monetary and fiscal policy support may be needed to assist the recovery of private demand. Meanwhile, Vietnam has approved three types of vaccines. The government also approved a resolution to purchase a total of about 150m doses.

The world's international trade has fared surprisingly well during the pandemic, and this has been especially beneficial for the region, as it is heavily trade-driven, contributing 210% to GDP. Just as the international trade suffered during the global downturn, it has also benefitted significantly as some countries started to lift restrictions, and the Western government released huge fiscal packages. Indeed, a surge in demand for PPE, electronics, and other working from home products has significantly benefitted Southeast Asian exports. By mid-2020, the region's exports had fallen by almost 16%, but by January, this had recovered to be slightly higher than the pre-pandemic level.

The trade outlook looks to be more promising. As mentioned before, the economy benefitted from increased demand for PPE and electronics. While this trend could potentially decelerate in 2021, as seen by a February decline of 5% in exports, global recovery and lifting of restrictions could accelerate the global recovery in trade. Demand coming from the US will be particularly important. The recent passage of the $1.9tr stimulus bill has taken the total scale of the country's fiscal stimulus planned for this year to 13% of GDP. The exact path to recovery is uncertain, given the uniqueness of this recession. However, combined with significant pent-up savings, a surge in US demand appears to be in the pipeline this year.

Corporate Results

Starbucks

Starbucks comparable-store sales fell by 5% in the quarter, driven by a fall of 5% in the US and a rise of 5% in China. The company opened 278 net new stores, a 4% y/y growth. Revenues, however, continued to decline marginally due to the impact of the pandemic, including reduced customer traffic, operating hours, and temporary store closures.

Americas saw net revenues fall by 6%, primarily due to a decline in comparable-store and product sales. These declines were slightly offset by net new store openings. In the US, in particular, even with pandemic-related business disruption in the latter half of the quarter, over 60% of US company-operated stores offering limited seating in Q1. US stores with drive-thru options saw a slight improvement in out-the-window times. They drove over half of the net sales in Q1, increasing more than 10% from pre-pandemic levels. Mobile orders represented 25% of US company-operated transactions in Q1, up from 17% before the pandemic.

According to the company statement, Starbucks' share of total packaged coffee grew significantly in the quarter, with dollar sales up nearly 14%, nearly twice the category average. The Global Coffee Alliance with Nestlé helped finish the calendar year 2020 as the number-one coffee brand across the entire coffee category. Indeed, one in two consumers in the US now prefer Starbucks versus anybody else's coffee in the marketplace. In addition, consumption of our US ready-to-drink coffee products in partnership with PepsiCo grew 18% in the quarter.

Business in China recovered in Q1 in line with company expectations, and it remains on track to achieve full sales recovery by the end of Q2. The company delivered a positive 5% comparable-store sales growth in Q1, driven by the rapid re-acceleration of new store development. In Q1, the company opened almost 160 stores and crossed the 4,800-store milestone. The number of 90-day active Rewards members grew to 15.4 million in Q1, a record increase of 51% y/y and 14% q/q. Starbucks remains Chinese consumers' first choice in the away-from-home coffee category and is the most talked-about coffee brand on social media in China.

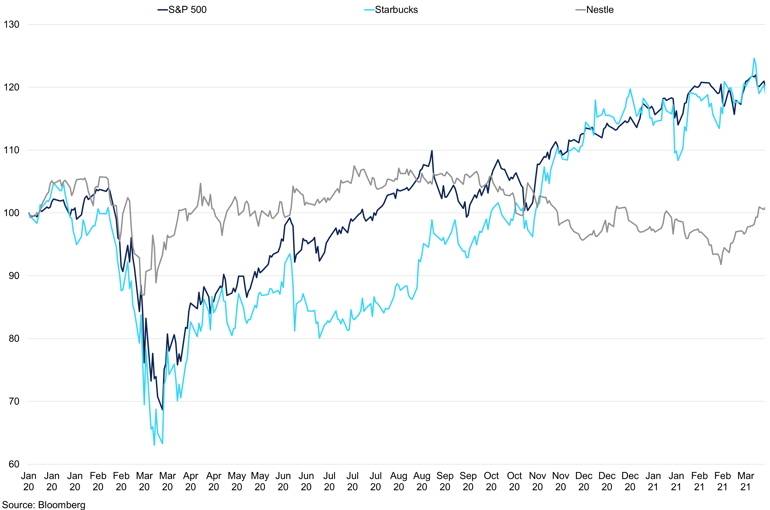

Starbucks vs Nestle vs S&P 500 Stock Prices

Starbucks continues to trace the S&P whereas Nestle broke the trend to correct back to March 2020 levels.

Nestle

Organic growth reached 3.6% in 2020, a third consecutive year of improvement and also the highest level in the last five years, supported by strong momentum in the Americas and sales development in EMENA. The company's 2021 outlook is to continue to increase in organic sales growth towards a mid-single-digit rate. Coffee reported mid-single-digit growth in the year, boosted by strong consumer demand for Starbucks products, Nespresso and Nescafé. Sales of Starbucks products reached CHF2.7bn, generating incremental sales of over CHF400bn in 2020. Retail sales posted high single-digit organic growth, reflecting elevated demand for at-home consumption. Sales in out-of-home sectors declined significantly

In the Americas, organic growth was 4.8%, with North America posting a mid-single-digit growth. Beverages, including Starbucks products, Coffee-mate and Nescafé, posted double-digit growth. Zone EMENA recorded its best organic growth in the last five years at 2.9%, with strong momentum seen in Russia, Germany, the UK and Israel. China posted negative growth due to the Chinese New Year, highlighted by declines in out-of-home sales and limited consumer stockpiling.

JDE Peet’s

In-home organic sales growth reached 9.1% in 2020, a historically high level, whilst away-from-home continued to fall, yielding a total organic sales growth of 0.2%. Despite renewed lockdown measures during Q4, organic growth sales came back to positive growth in H2 2020. Single-serve and beans saw the greatest increase in at-home organic sales, exemplified by 71% growth in commerce during the year. Value market share also increased for categories such as beans, capsules, and pads. While APAC started its path to recovery in 2020, the US remained affected by non-return to offices and universities. In the rest of the world, mostly Europe, there was a recovery in Q3 but affected by renewed lockdowns in Q4. For medium- to long-term targets, JDE Peet's forecasts a 3-5% organic sales growth, with the same range for fiscal 2021.

Because in Q4 of last year, new movement restrictions and lockdowns were announced across most markets, the recovery of the Away-from-Home channel was stalled with similar challenges and impact in H2 as in H1. The emerging markets were pretty resilient and kept overall a good growth momentum in 2020, while the strongest uplift came from the developed markets where home was recast as the new coffee shop with consumer more than ever looking for a high-quality cup of coffee at home. From a channel perspective, the company saw a surge in e-commerce for in-home consumptions going by just over 70% in 2020.

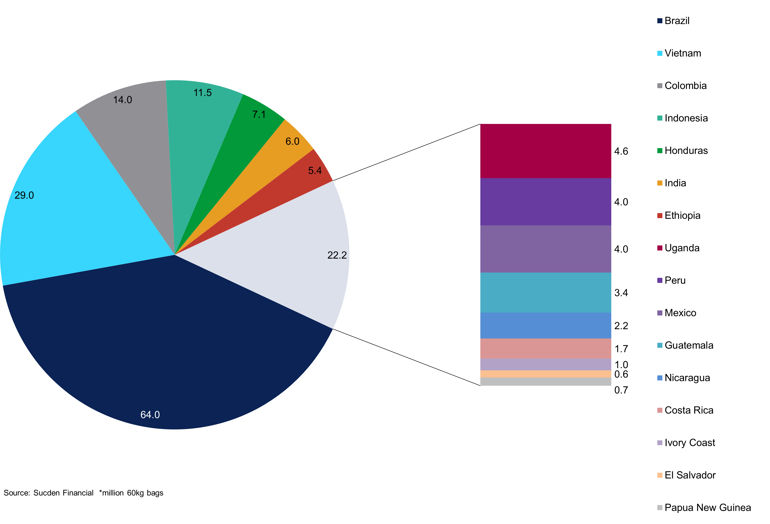

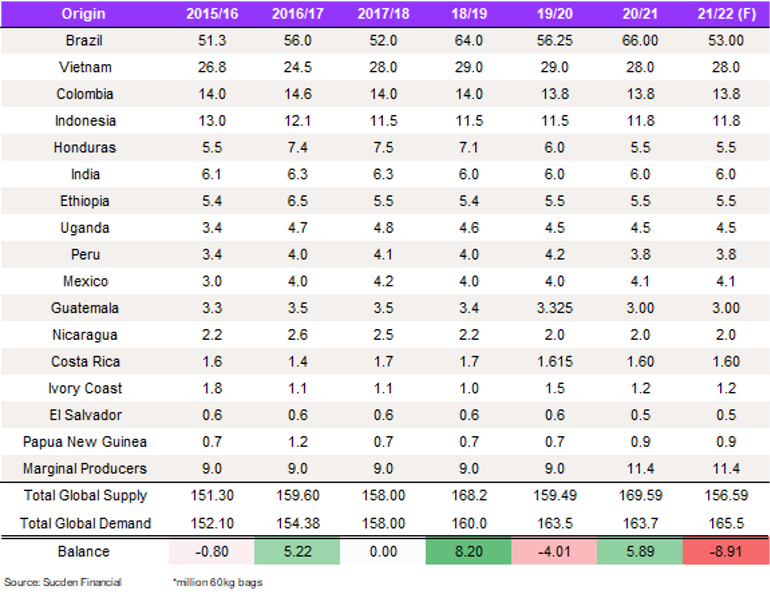

Supply and Demand Balance

Source: Sucden Financial

In our recent crop update, we provided insight into why the market has not rallied without looking back. Patience remains the message, and we expect the deficit to really emerge in the coming months. Our final scenario model for demand last year showed a worst-case scenario drop off in consumption of 1.8m bags, this brought our final demand figure to 164m bags. The drop off in demand has come from those on low incomes in the US, and Europe but also reduced consumption in Brazil. US and Canadian demand stand at 33.5m bags, with European consumption at 51.5m bags. When modelling coffee demand this year, looking at traditional variables will not show a clear picture especially with GDP growth, and employment. Under our business as usual scenario, consumption will recover to 165.5m bags for 2021/22, which is marginally below our original demand figure for 2020/21 which was 166m bags.

At-home consumption continues to dominate the outlook and will do for the foreseeable future. We expect higher at-home consumption to remain the norm in the long run as offices relax home working policies. This could see roast and ground coffee continue to gain market share, however as we move into a deficit year and reduced availability of fine cup and washed arabica, how will blends change? Research suggests that the coffee pod and capsule will reach $25.48nm in 2025, a CAGR of 7.3%. We expect this trend to have been intensified due to COVID-19, especially in Q1 2021 with lockdown restrictions in Europe. JDE’s financial results suggest that that the in-home sales grew at 9.1%, compared to a decline in out of home consumption of 30% in H2 2020. They believe out-of-home consumption will rise by 3-5% in 2021 which will provide headwinds to in-home consumption. Coffee machine sales are expected to reach $10,454m in 2020, according to Statista, and this will keep pod demand well supported going forward. However, we expect consumers to reduce their at-home inventory due to more time in the office and also reduced pressure on the supply chain. We have previously highlighted that pod coffee increase the efficiency of demand by reducing wastage, we expect this to remain the case. We continue to be cautious about consumption when furlough schemes finish, and unemployment rise but as mentioned in I previous report coffee is relatively inelastic which will minimise consumption drop off.

Asia pacific consumption will continue to grow, China remains the key market in the long run and can significantly change the fundamental balance. The strength in the Chinese recovery will support Chinese consumption of coffee, but concrete numbers from China is hard to come by. Sales data from Starbucks shows that comparable-store sales were up 5%, as the average ticket increased 9%. China comparable store sales benefit from value-added tax exemptions of 5%. The company opened 600 new stores in China, and we expect this trend to continue. Average per capita consumption stands at 0.1kg in 2021, this is considerably below major economies such as Germany, France, the US where average per capita consumption is 4.7kg, 3kg, and 3.5kg. Scandinavian countries consume considerably more coffee on a per capita basis. According to Statista, revenue in the coffee segment reached $14,349m in 2021, and the market is expected to grow by 8.9% CAGR between 2021-2025. We highlight the very low base that consumption is coming from, roasted coffee remains the largest segment in China. AJCA data outlines that re-exports of roasted coffee from Japan to China was 119,927kg (net weight), increasingly from 17,013kg in December 2019. Soluble re-exports for December 2020 reached 87,750kg net weight, up from 51,783 kg in net weight for December 2019. While this is data is isolated, the trend continues to show a large amount of coffee re-exported from Japan to China and Hong Kong.

As they move out of lockdown restrictions in the UK, and vaccination rates across Europe increase, this will support out of home consumption. However, as we head into a deficit year for washed arabica and fine cup coffee, will we see a change in the trend of blends for roast and ground and pods. Our S & D breakdown sees a potential decline in arabica availability from Brazil alone 17m bags, when you factor in the damage in Central America, in conjunction with low availability of washed arabica in inventory, there is little option to maintain blends of washed arabica. Imports for November 2020 into the European Union were down year on year by 1.6% to 6.524 60kg bags, November to November 2019/2020 figures show a decline of 3.2% to 77,803 60kg bags from 80,343, according to the ICO. Imports into the U.S. were down 8.6% y/y from November to November 2019/2020, imports into the U.S. reached 28,352 60kg bags, this includes 2,146 60kg bags for November 2020. Imports for major consuming countries are down y/y and this indicates weaker consumption for 2020. The just in time supply chains were tested last year, we expect this could see some roasters run at a higher inventory in the near term, especially with consumption set to rise this year as out of home consumption improves.

When we look at exports from member and non-member ICO states, exports of Arabica were up 3.7% from October 2020 to January 2021 to 27,001 60kg bags.41, 876 60 kg bags between October and January. It is not surprising that Brazilian milds have seen a large increase in this period, with exports at 16,062 60kg bags up 21.8% in October to January. Exports from Brazil will start to tail off as we approach July, then we will start to see the extent of the deficit, we believe exports for Arabica coffee will fall significantly, but the Conillon coffee shipments will be elevated.

Supply

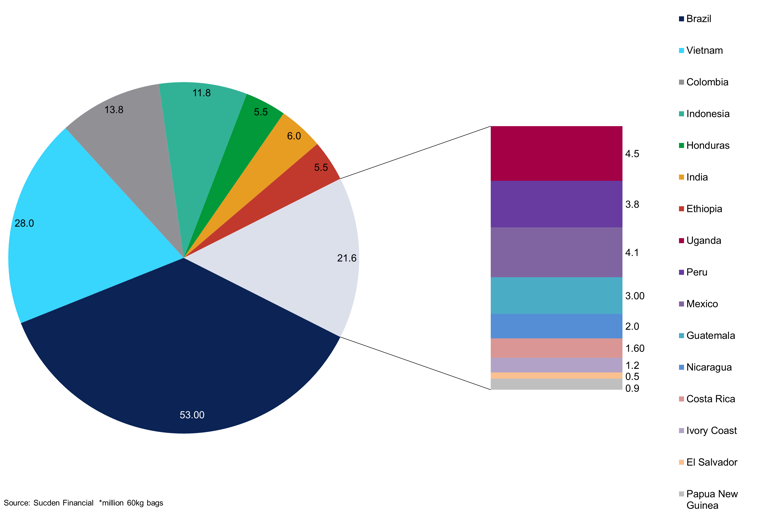

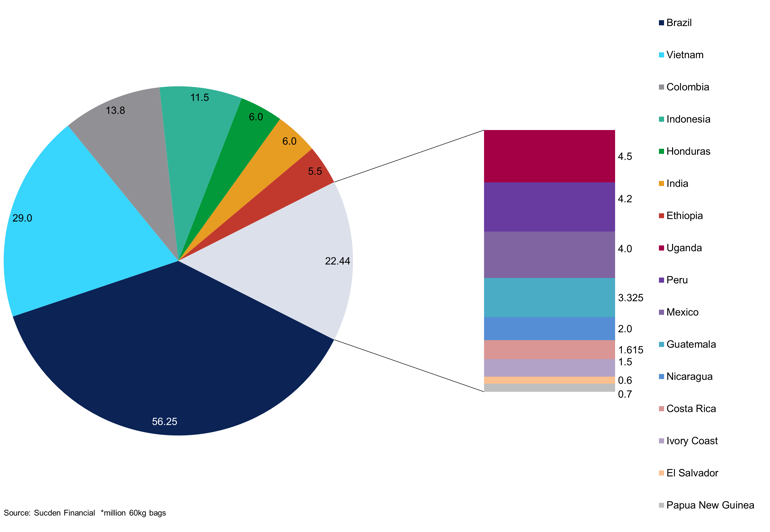

In our crop update, we moved our Brazilian crop number to 53m, this is a split of 20m Conillon and 33m Arabica. The reduced availability of Arabica will play out after July when we enter the new season, shipments will be drop off. Our crop number for 20/21 was 66m bags, with a split of 48m bags Arabica and 18m bags Conillon. For 21/22, our arabica number is 33m bags, this is a reduction of 15m bags, assuming a maximum semi-washed arabica is 3m bags, this leaves 12m bags of unwashed Arabica. This is a lot of coffee to make up elsewhere, and we don't see it being done. Our crop forecast for 2021/2022 globally stands at 156.59m bags, with a preliminary deficit of 8.91m bags. This is under the assumption that demand increases back to 165.5m bags, there is a propensity for demand to grow by 2m bags to 166m, which would increase our deficit slightly to 9.4m bags. The change in the balance sheet helps to confirm our bullish stance on the coffee market, Arabica. We have been saying for some time that the tightness is in the Arabica market, the washed Arabica, and the fine cup market. Differentials are still strong for this coffee, and we do not expect the market to decline. At the time of writing, Colombian coffee excelso is +48/cts FOB, Honduras is +19cts/lb FOB. We expect the flat price to hit 150cts/lb in the coming months, and this could cause differentials to soften marginally, however, the lack of Colombian coffee will mean it is quickly consumed.

Brazil

The market has been relatively quiet, total shipments remain above 3m bags, with Arabica shipments reached2.68m bags. Conillon shipments have also fallen to 312,296 bags, with green exports at 2.99m bags for February. The volatility in the NY contract has kept business relatively quiet; even with the recent rally, producer selling was subdued. We have seen some business above R$800, but in recent weeks most of the trading was done between R$780-790/bag for fine cup qualities Duro qualities range between R$710-720/bag and R$730-750/bag, local prices remain preferential, and we expect this to remain the case with farmers getting more and more greedy. The export business continues to soften with volumes through to March 15th at 1.535m bags with boarding at 487,761 bags. Brazilian coffee continues to be well priced, but the certified stocks remain the cheapest coffee around, we could see more semi-washed coffee certified. We still believe the semi-washed coffee will start to decline from April onwards, and if the March emissions and boardings are anything to go by March exports will be considerably lower than February's. This may mean producers have higher on-farm inventories in the near term, but what we hear from the shipping market is reduced container availability in Brazil, and we continue to look at some delays in the coming weeks.

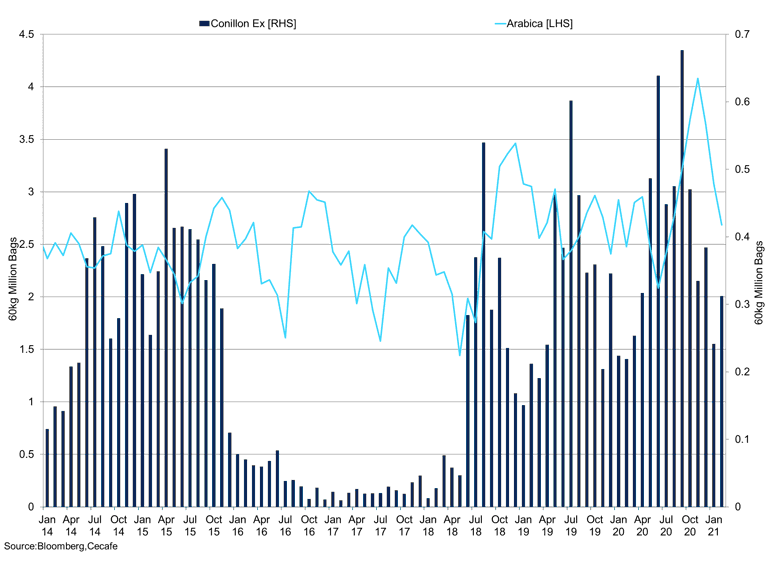

Brazil Conillon vs Arabica Exports

Exports will fall into the new crop year, but we expect fewer Conillon shipments to remain elevated next crop year.

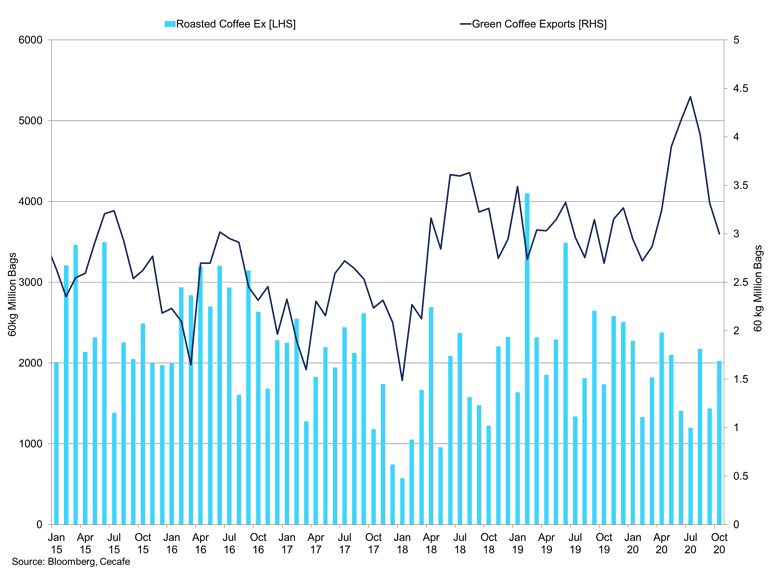

Brazil Roasted vs Green Coffee Exports

Roasted coffee shipments have been trending lower for months, and Green coffee exports have fallen sharply.

ICE inventory for Brazilian coffee stands at 847,434 bags as of March 15th, coffee pending grading has declined significantly since the beginning of February when pending grading was 156,000 bags, as of March 15th gradings were 28,631 bags. As mentioned, semi-washed certified coffee has value at current prices, with the differential at -12cts/lb at the time of writing, we do expect this coffee to be taken up in the next 12-18 months. However, we largely expect shipments to fall in the coming weeks. As we look to the new coffee year from Brazil, we maintain our bullish stance on the crop, and we will start to see this play out in the coming months. Better prices will help farmers, and while we will then head into an on year for the crop, the weather will need to be very good and the yields high to help offset the loss of coffee from this year.

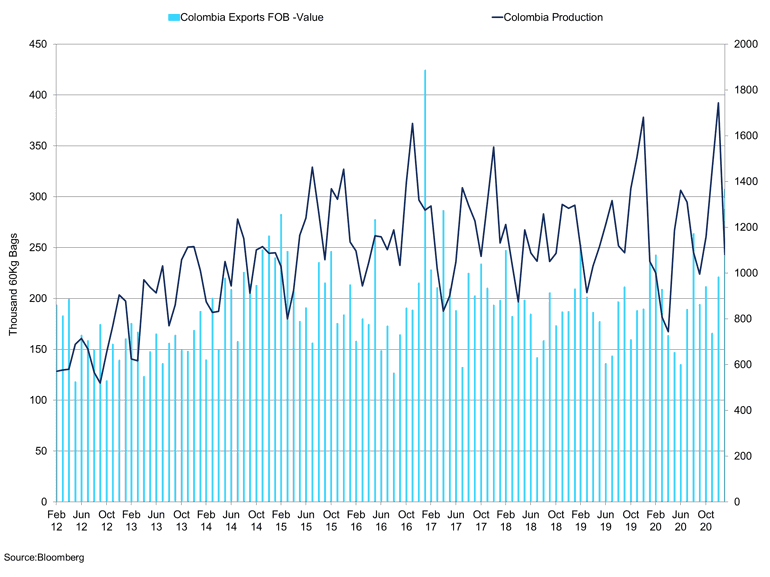

Colombia

Spot prices in Colombian coffee have risen in recent months, and stand at 9,194COP/lb, this is just off the high at 9,794COP/lb. Colombia, like other EM currencies, benefitted from risk appetite following the approval of vaccines and the hunt for yield. In the first few weeks, the dollar has started to rally, as US treasury yields strengthen, prompting inflows of funds into the yields. The dollar has continued to rally, putting pressure on EM currencies, this will give farmers preferential prices. However, when the farmers look to invest these profits in new equipment and fertilizers, their peso will be less competitive. We expect funds to be re-invested into future crops, which will improve yields, we expect this to increase the return of the 2022/23 crop. Our crop number for 2021/22 is 13.8m bags, lack of pickers in the fields could cause this figure to edge lower, but weather has been beneficial, so we expect the quality of the crop to be good.

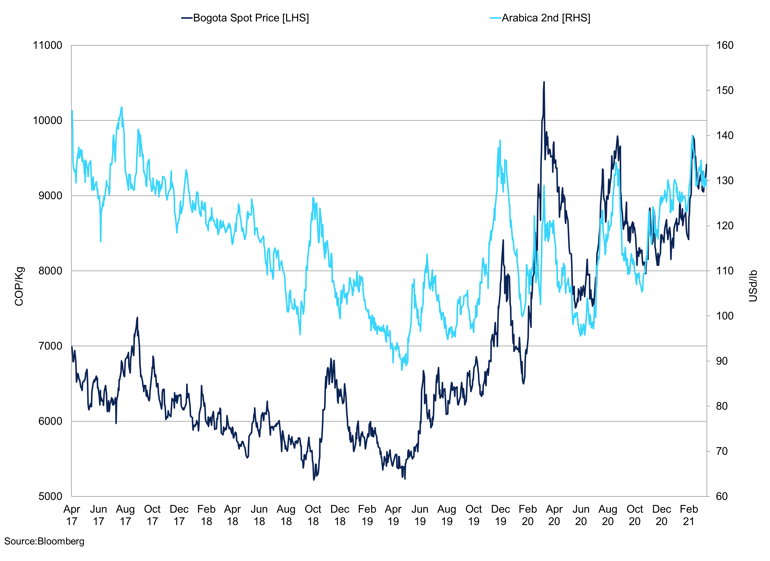

Bogota spot vs Arabica

Weakness on the Peso has been trending lower since April 2019, we do not expect the currency to strengthen.

According to Federacion Nacional de Cafeteros de Colombia, production in February reached 1.17m bags, up 11% y/y, so far, this coffee year output is down 1% y/y at 6.5m bags, compared to 6.6m bags in 2020. Production in the last 12 months, between March 2020 and February 2021 is down 3% to 14m bags from 14.4m bags. The drop off in Colombia production has been mirrored in the export market, shipments in the last 12 months are down 5% to 12.7m bags down from 13.4m bags. This coffee year, exports are up by 1% to 6m bags from 5.9m bags, in February, we saw shipments rise 18% to 1.275m bags from 1.078m bags the previous year. This coffee will go straight to the industry as Colombian coffee in ICE warehouses remains very low at 105 bags.

Colombia Exports FOB vs Production

Colombia exports are weaker than the same time last year, with output marginally softer.

Central America

Our crop number for Honduras remains at 5.5m bags for both the 2020/21 and 2021/22 seasons. The weather has been slightly drier recently, which would have helped pickers in the fields. Labour shortages, as well as the hurricanes, have hindered picking in recent months, but we do not envisage these issues continuing. Although there picking is taking place, and the harvest will continue to April, despite the improved picking conditions, exports will remain low on a year-on-year basis. February shipments were stronger than previously anticipated, with exports at 761,658 bags compared to 759,009 bags the previous year, exports for the year are down close to 30% y/y. We reiterate our stance that, Honduran coffee in stocks will fall sharply in H2 2021 when the deficit is more apparent.

Elsewhere in Central America, we have maintained our crop numbers for Nicaragua and Guatemala at 1.6m bags and 3m bags, respectively. Both origins will see strong demand for their coffee in the coming months, although we continue to hear reports in Guatemala of problems with the exports due to port capacity. This could present some headwinds to shipments in the longer run.

Vietnam

We maintain our crop number for Vietnam at 28m bags for the 2020/21 crop, for the 2021/22 season, we expect to see a similar crop number. It is early to call the 2021/22 crop with high certainty; input prices are higher this year which could reduce husbandry, but farmer margins at current levels are decent. With Dak Lak Robusta coffee at 33,000VND/kg and grade 2s around 100+, there is a reduced incentive to plant new coffee in Vietnam, we continue to reiterate that other crops may be more attractive crops. Trades have been around 32,000/32,5000VND/kg recently, farmers continue to hold out for higher local prices and did not sell heavily into the recent rally, we expect the crop to be nearly 65% sold at the time of writing. This has led stocks in Vietnam to remain high, Ho Chi Minh stocks have increased in recent months, with February levels at 6,428,000 bags, up 550,000 bags M/M and 777,000 bags Y/Y. We expect issues in the freight market to dissipate and support exports in the coming months, after a slow start.

Exports from Vietnam in Q4 2020 averaged 85,000 tonnes, which is down from the previous year when exports averaged 123,000 tonnes. Exports from Vietnam were last year, especially in the H2 2020, this year's shipments have remained low at 120,000 tons and 110,000 tons for January and February, respectively. The availability of Robusta coffee will improve as shipments start to rise, and local inventories start to drawdown. The Robusta October 2021 to October 12th month calendar spread has widened out to -$95/t as of March 18th after reaching -$83/t as of February 23rd, 2021. With the larger Conillon crop, and shipments from Vietnam improving, we do not expect considerable tightness in the Robusta, and the spread will remain wide enough to carry coffee. We do not see the tightness in the Robusta market and expect this to remain the case, Vietnam diffs are 100 over a time of writing which is softer than in recent months.

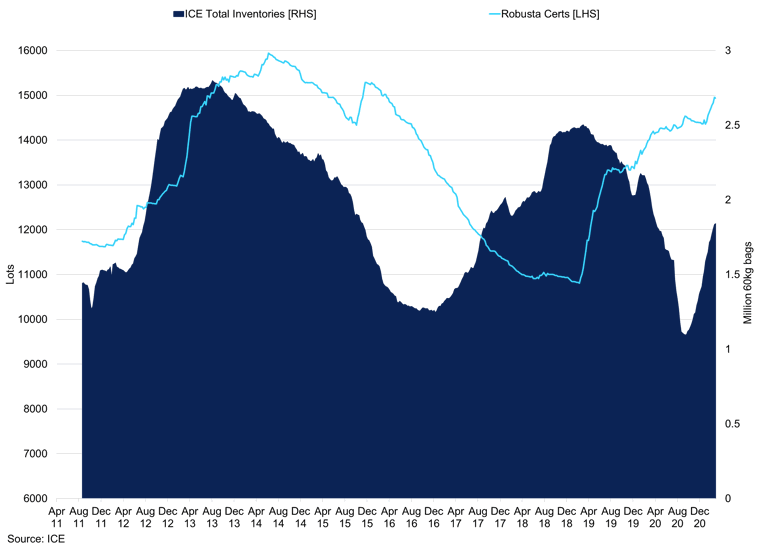

ICE Inventories by Key Origins

Semi-washed Brazil coffee has caused inventories to rally, we do expect this coffee to be consumed in the next 12-18months.

Source: ICE, Bloomberg

Inventories

GCA stocks saw a modest draw of 52,600 bags in February, reverses the flows of the previous month. Total stocks were 5.79m bags, we saw builds in Baltimore, LA, Norfolk, Laredo, Houston, Miami, and Jackson. The largest draws were in NY, Seattle, San Francisco, and Nola. Savannah went form no inventory in March 2020 to 322,480 bags; this remains a trend we watch closely, but it suggests improving cover from roasters in the area. ICE inventories continued to increase as well, reaching 1.834m bags in, Antwerp continues to hold most of the stock, with 95% of inventory in Europe, bags passed in the week to March 15th were lower than the previous week at 22,730 bags.

ECF released an update of the coffee in their warehouses reached 862,798 bags as of December 2020, up from 753,688 bags in January 2020. The breakdown saw net increase of 38,086.29 tons for Robusta, 31,503.34 tons for Natural Arabica, and finally Washed Arabica gained 39,521.1 tons. The increase in inventories is notable but was not exponential, suggesting that European consumption did not fall off a cliff, it is also worth remembering that this exchange and non-exchange inventory. ICE inventories for Arabica certified stocks have trended higher in recent week months, in line with the on-cycle and softer macro environment. While consumer inventories are high, stocks are high of the wrong coffee. Washed arabica stocks are low, and not enough to fill the on-coming deficit, but we do expect the semi-washed coffee to be consumed in the next 12-18 months. In our opinion, the inventories will continue to start to fall in May, which will aid the bullish narrative.

ICE Certified Stocks

Inventory levels have been increasing for both markets, putting pressure on prices in recent weeks.

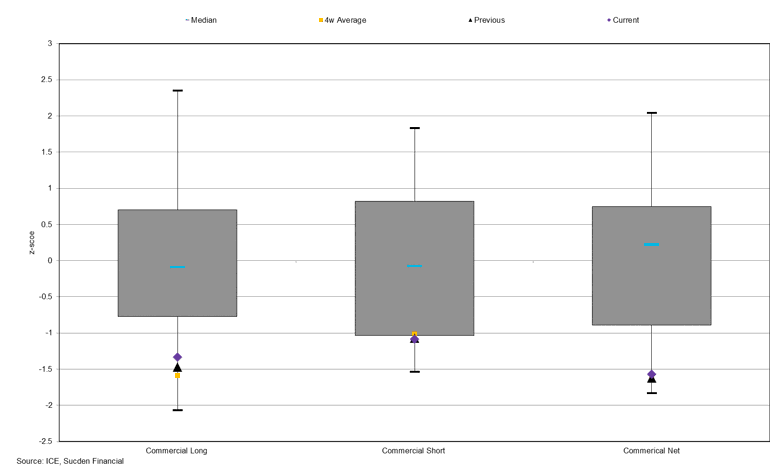

Commitment of Traders

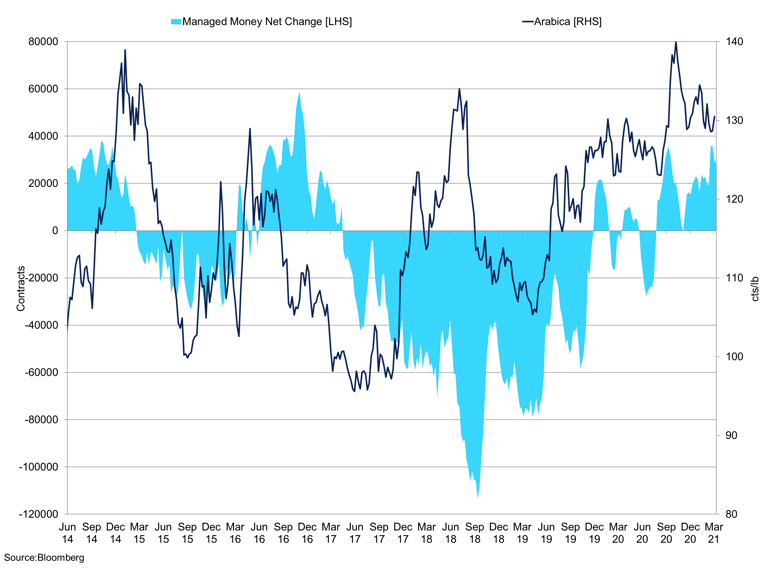

ICE Arabica Managed Money vs 2nd Month Price

The flat price has not maintained the rally despite the managed money change remaining positive.

We have seen the investment funds moderate their net length in the last few weeks, in the week to March 19th the net position has declined to 48,371 contracts. We saw 100 long contracts added, but also 2,081 shorts were added. Total OI and traders were higher in the same week to 331,430, up by 2,359. Even though we have seen the net position fail to kick on, once normalized, the current z-score stands at 1.52, not too far off the maximum of 1.79. However, what is key is the OI and traders z-score is negative and well below the maximum. We see this as bullish in the long run, the max z-score is 2.80, but the current z-score is -0.1905, it remains above the 4-week average. Recent volatility has caused markets to whipsaw, but the fundamental picture looks bullish. Longer-term traders have struggled due to the volatility and lack of clarity. The semi-washed Arabica, rising or flat inventories, and the weakness in the reasis has not given traders confidence in the rally, which may have caused speculators to look elsewhere for alpha, especially with yields rallying. Once inventories and Brazilian shipments start to decline, we expect an inflow of funds into the coffee market as the large deficit emerges. The non-commercial long z-score stands at 2.12, shy of the maximum of 2.69, the absolute position is 70,862. Price action since, suggests the net position has declined as traders lose patience.

The Commitment of Traders – Normalised Historical Commercials Positioning

The commercial short position has a z-score of -1, the net position is close to the record low outlining sentiment in the market.

On the commercials side, the gross commercial short remains near the record high at 199,079 contracts as of March 19th. The pullback in prices has been kind to those who have hedges between 120-125cts/lb. The net commercial position is a 54,264-contract short, but when you look at the commercial long, the current position of 144,815 contracts is near the historical low of 130,636 contracts. The large amounts of producer selling that has been done on the forward crops remains a risk, however, the market has been kind to these traders. Roasters who failed to believe the rally has been given a chance to cover further out. Currencies have favoured producers, and they become more and more greedy with local prices above R$800/bag. We expect producers to cover their shorts above 142cts/lb which will trigger a break of 150cts/lb, a big level in the options market, especially with September expiries due to the reduced time decay.

In the Robusta market, managed money positions stand at 18,693, as of March 22nd, down 1,705 from the previous week. The recent net position of 28,473 was the highest since 2017, the majority of the change in position was due to a 199% increase in long positions in February. The number of shorts has declined in the last few weeks, declining 76.43% to 6,624, the short position has increased to 11,038 contracts. We maintain our view the Robusta market will remain in surplus for next season and do not expect to see large net positions accumulated in the London contract. Producers liquidated short positions after reaching 96,482 on March 2nd, as of March 16th the net position stood at 79,909 contracts. The pullback in prices has prompted less producer selling, which has caused the commercial net position to reach -27,929 as of March 16th.

Trading Strategy

- The market fails to gain a conviction on the upside, and this brings the Arb closer to range in where we see a good entry point. Between 60-65cts/lb is a strong area, with anything below 60cts/lb even better.

- In the Arabica market, we favour selling July 2021 120 puts, which will yield 3.20cts as of March 29th vs a July 2021 150 call which costs 2.25cts. The put will put you long at 116.80cts/lb.

- Robusta, we remain neutral on Robusta and would sell the market as it approached $1500 with the downside of $1300. We see a surplus in the Robusta market and don’t expect strong gains.

Appendix

Sucden Production Chart 21/22

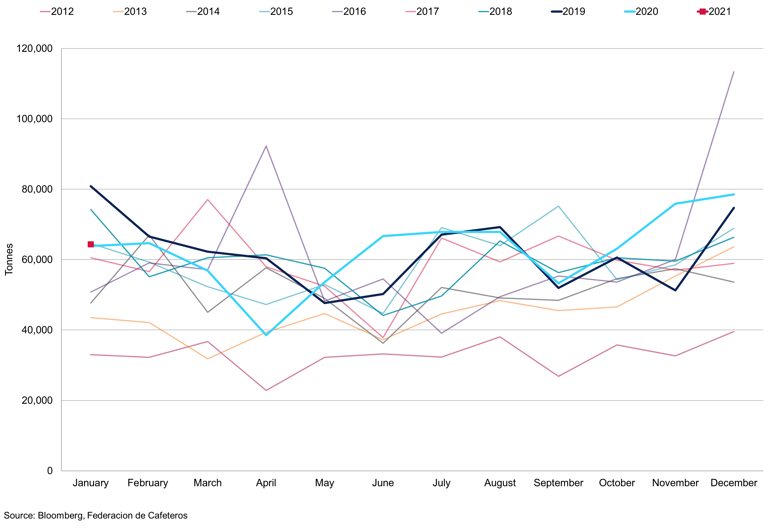

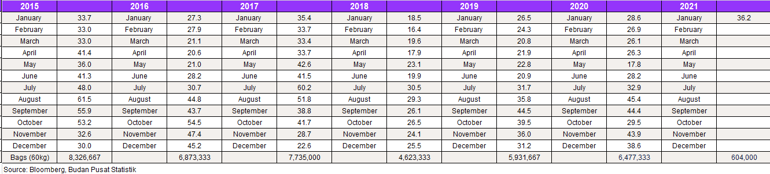

Brazil Coffee Exports

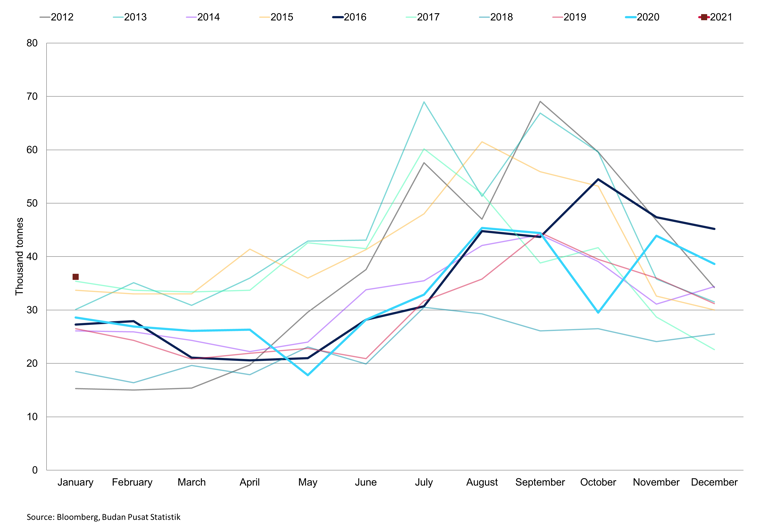

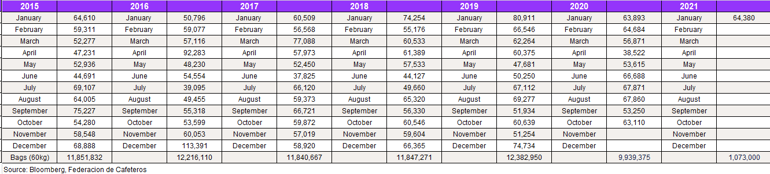

Vietnam Coffee Exports

Colombia Exports

Indonesia Coffee Exports

Brazil Coffee Exports

Vietnam Coffee Exports

Indonesia Coffee Exports

Colombia Coffee Exports

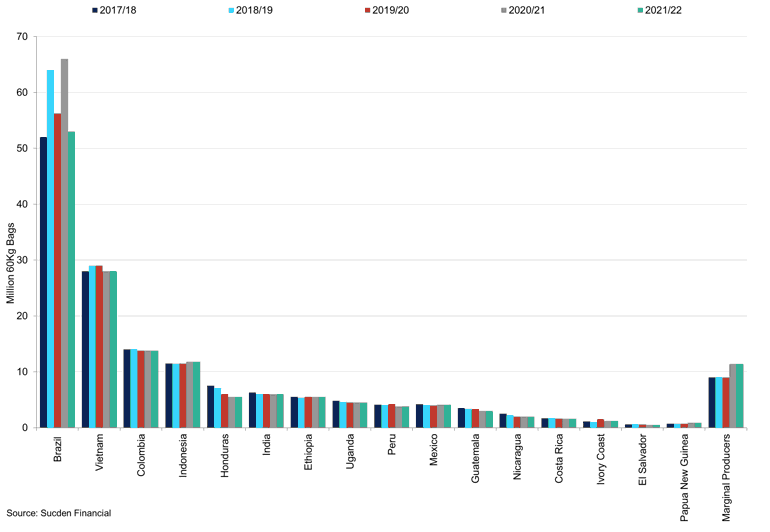

Global Coffee Production 21/22 Bar Chart

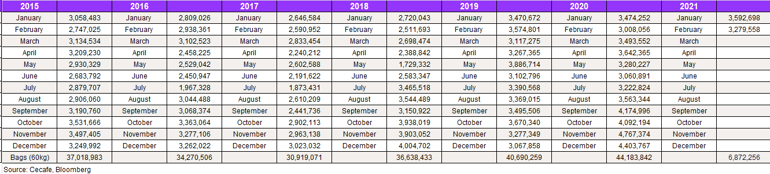

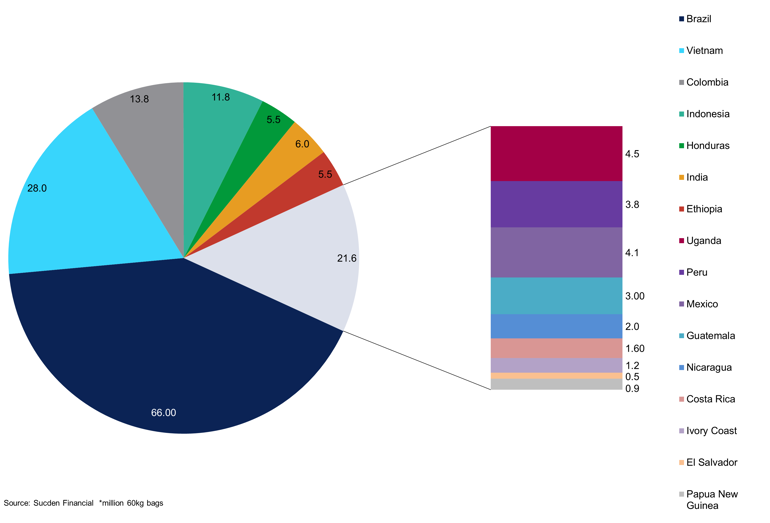

Global Coffee Production 2020/21

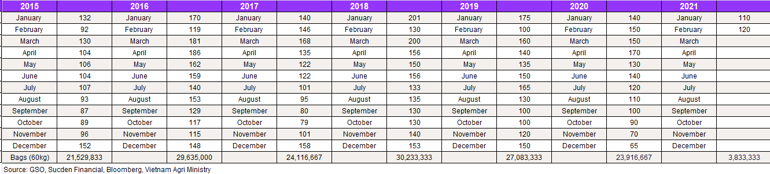

Global Coffee Production 2019/20

Global Coffee Production 2018/19