Executive Summary

- Major central banks are reaping the benefits of the most aggressive monetary tightening campaigns in decades with inflation continuing to soften at a steady pace.

- Growing uncertainty regarding the path of the Fed’s monetary policy brings us into sentiment-driven territory, and until another meeting in July, we expect to see heightened volatility in the markets.

- While we remain cautious about the prospects of further hikes, inflation and labour market data should guide the market’s tightening expectations into the summer meetings.

- Higher soft agricultural prices are likely to further prop up the Brazilian economy in Q2'23, and we already have seen local currency benefit as a result of strong overseas demand.

- Since our last report in March 2023, coffee prices have remained broadly unchanged, above 170cts/lb, but the story remains centred around Brazil.

- We remain friendly for both contracts; however, given that 70% of the Vietnam crop is already sold and we still have five months until the new crop is out of the region, our view is more constructive for Robusta.

- Overall, the recent upside appetite for soft commodities, and in particular, sugar and cocoa, is helping to support coffee futures in the meantime.

- With 25% of the crop harvested, Brazilians remain price-conscious, selling on rallies than on weaknesses.

- At this stage, farmers are in a better financial situation to carry some stocks and warehouse them well.

- El Nino is forecast to exacerbate the weather conditions by the end of this year, going into 2024, which is around the flowering time for Brazil's 24/25 crop year.

- The Vietnamese coffee farmer has been very price conscious, willing to turn to more profitable plants when returns on coffee prove not rewarding enough.

- The tightness is set to remain sustainable in the meantime, and this should keep Robusta prices buoyant until the start of the new crop in October/November.

- Speculative positioning continues to run a long position, however, reduced from the recent high levels.

- We do not expect that industry will contribute much to the upside in the meantime, but given the need for further coverage, steady buying should take place instead.

Our View

Since our last report in March 2023, coffee prices have remained broadly unchanged, above 170cts/lb, but the story remains centred around Brazil. Certified stocks have seen a considerable decline, further drawing down on available inventory from the region. While this should have been supportive of higher prices, futures have remained broadly unchanged. As we head into the harvesting period for Arabica, we begin to assess the outlook for the 23/24 crop in this report. Robusta was the biggest market mover, gaining as much as $760/mt on the London contract. We remain friendly for both contracts; however, given that 70% of the Vietnam crop is already sold and we still have five months until the new crop is out of the region, our view is more constructive for Robusta.

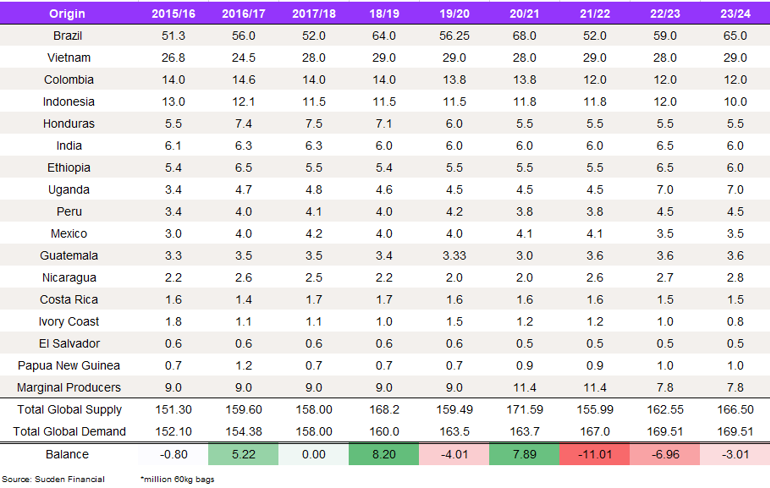

Colombia, although far from the 14m bags it produced in the past, is set to perform better in the 23/24 crop, reaching 12m bags. The third biggest producer has been importing coffee from Brazil, both Arabica and Conilon, and we expect these exports to continue. When it comes to Central America, we will update our numbers in October, when we have a better idea of what the crop is going to look like. Constant rain is still weighing on crop yields in Indonesia, which led us to lower our number by 2m bags. Given Indonesia’s contribution to the global Robusta crop and continued uncertainty from Vietnam, it should further strengthen the narrative of market tightness. In India, weather problems have weighed on the supply out of the region, and due to high prices, we do not expect Indian Robusta to be attracted to the futures market. Overall, the recent upside appetite for soft commodities, and in particular, sugar and cocoa, is helping to support coffee futures in the meantime.

Macro Overview

Global Outlook

While the global economic slowdown is underway across developed and developing countries, the growth outlook for 2023 has improved since March as more economies are set to avoid recession. Major central banks are reaping the benefits of the most aggressive monetary tightening campaigns in decades, with inflation continuing to soften at a steady pace. Still, underlying price pressures are proving upwardly sticky, which strengthens the narrative of higher interest rates for longer. The banking sector turmoil, caused by the collapse of Silicon Valley Bank (SVB) in March, has uncovered financial sector vulnerabilities, proving that risks to the global outlook are skewed to the downside. At the same time, China's economic rebound seen earlier this year lost momentum in Q2 2023, painting a grim picture for the world's economy. Growing uncertainty regarding the path of the Fed's monetary policy brings us into sentiment-driven territory, and until another central bank's meeting in July, we expect to see heightened volatility in the markets. Global growth is forecast to slow, and the IMF expects growth of 2.8% this year, relative to 3.4% in 2022.

IMF 2023 Growth Projections

Most of the developed world is set to stagnate this year.

Source: IMF

US

The US economy continues to show signs of resilience, with economic growth in Q1 2023 revised up to a 1.3% annualised rate, up from an initial estimate of 1.1% reported last month. Consumer spending, which accounts for more than two-thirds of US economic activity, increased more than expected in April by 0.8% MoM, suggesting that overall consumption remains robust. Retail sales, a key indicator of the consumer's propensity to spend, rebounded 0.4% MoM in April following two months of declines. Sales at food services and drinking places increased by 0.6%, indicating that consumer demand remains resilient despite a challenging macroeconomic environment. Rebound in consumer spending comes at a time of persistent labour market strength, which could encourage the Fed to keep interest rates higher for longer. While the unemployment rate was expected to increase, it fell to a 53-year low of 3.4% in April, indicating that tighter credit conditions are yet to have an impact on the economy. In May, US job growth accelerated as employers added 339,000 jobs, up from 253,000 the previous month.

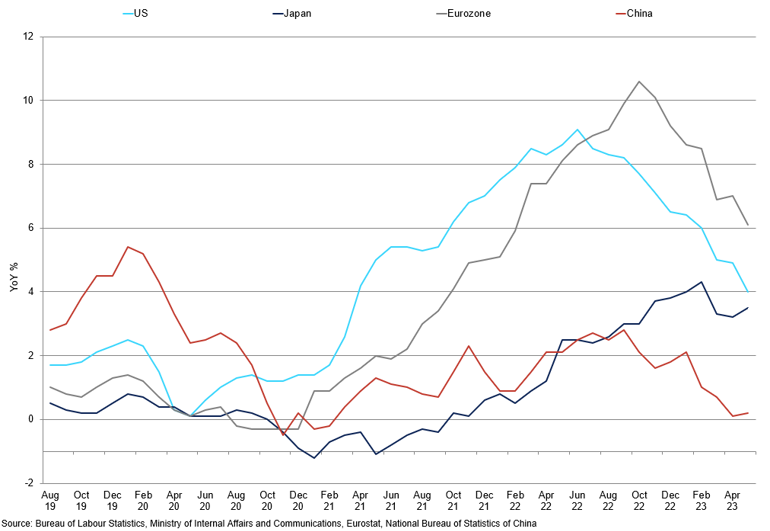

Developed Nations' CPI Performance

US and Europe continue to soften into 2021 levels, while Japan and China's pricing pressures are seen ticking higher.

At the same time, albeit softening, inflation remains above the Fed's target, with the last CPI figure at 4% YoY compared to 4.9% in April. It marks the smallest increase since March 2021, proving that the two-year-old cycle of monetary tightening is having an impact on price pressures. Still, the Fed does not reject the possibility of two more interest rate hikes in H2 2023. At their last meeting in June, Jeremy Powell announced that the federal funds rate might reach 5.6% by the end of the year, leading markets to price out the interest rate cuts that had been expected in November/December time. By adopting such hawkish rhetoric, while keeping the interest rate unchanged for now, the policymakers are giving themselves space for further tightening in case coming data points to strong price pressures. The statement has caused the 10-2-year bond yield spread, a gauge of economic recession, to decrease further into the negative territory at a time when business activity is slowing down, bringing inflationary fears forwards.

Europe

The eurozone economy has managed to avoid a contraction in Q1 2023, growing marginally by 0.1% q/q, but the outlook remains bleak. In particular, countries like Germany and Norway, the bloc's biggest nations, posted negative growth in the first quarter of the year, putting them on course for a technical recession. Retail sales fell by more than expected, falling by 2.6% y/y in April, with Germany posting the biggest decline. This underscores the fragility of the European Union's economic performance in the face of further tightening from the central bank. The ECB increased rates by 25bps in June, in line with expectations, and indicated that further tightening is likely. We anticipate another 25bps jump in July, bringing the deposit rate to 3.75%, and see risks skewed on the upside for the September meeting. While we remain cautious about the prospects of another hike in September, inflation and labour market data should guide the market's tightening expectations into the meeting, adding to the volatility.

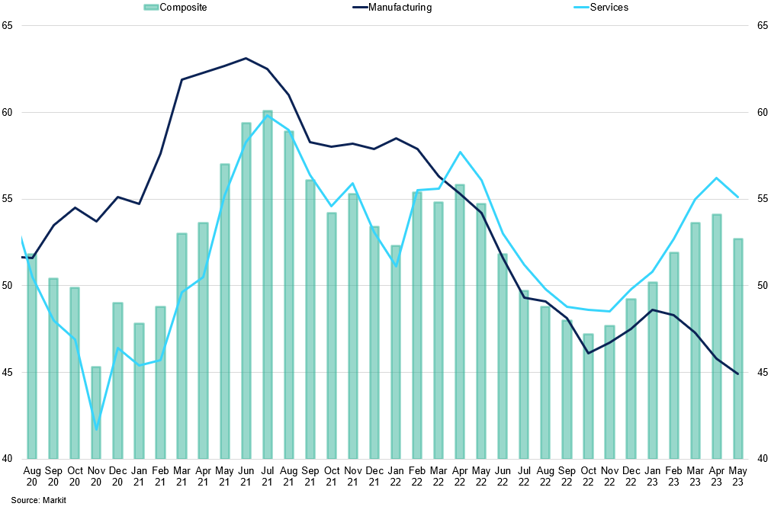

Manufacturing vs Services Eurozone PMI

Both industrial production and services softened last month.

Moreover, the upward revision by policymakers in relation to inflation forecasts increases the risk that the end of the tightening cycle might be slightly beyond what markets have anticipated. In May, CPI continued to slow, growing at 6.1% on a year-on-year basis. This marks the lowest level since February 2022; however, it remains upwardly sticky, with core performance remaining high at 5.3% y/y. While the near-term outlook is seen improving from the Q1'23 lows, elevated energy prices and, in turn, persistent inflation should yield a modest gain in activity this year. Given the less robust fundamental picture in comparison to the US, we expect the euro to deteriorate in the latter half of the year.

Brazil

Brazil's economy expanded by 1.9% QoQ in the first quarter, beating expectations and lifting the 2023 growth outlook from 0.9% to 1.3%. While manufacturing PMI remains in contractionary territory, at 47.10 in May, robust service sector performance boosted the composite reading to 52.30, suggesting that overall consumption in the region remains robust. While retail sales continue to soften, with YoY growth at 0.5%, they remain in line with the 2-year average, suggesting the consumer sector is healthy. Overseas demand remains relatively robust, highlighting the strong underlying fundamentals in Brazil. The export volume index reached an all-time high of $33.1bln in May, up 11.6% from the same time last year. Higher soft agricultural prices are likely to further prop up the agricultural part of the economy in Q2'23, and we already have seen local currency benefit as a result of strong overseas demand, with USDBRL at 4.80 at the time of writing. China's reopening theme could see commodity prices, and in particular, oil, shoot higher, driving the growth in producer price performance. Still, growth for 2023 is set to recede sharply to 0.8%, down from 3.0% in 2022. Inflation is poised to decline until the end of the quarter, especially given the round of tax reductions enacted last year. However, expectations are set to increase once again in the latter half of the year, with inflation growing to the 6.32% level in Q3'23, according to the central bank data. If these expectations materialise, this should reaffirm the policymakers' rhetoric of higher-for-longer rates for most of the year. The next central bank meeting is scheduled to take place on June 21st, and we expect rates to remain flat at 13.75%, the highest among the major developing economies. The BCB has kept the rates unchanged at current levels since August, hiking 11.75% since the end of 2020 and keeping the rate unchanged right through the election process. Brazil has done most of the damage before the Fed and the ECB, driven by historically high inflation. Even with the threat of inflation subsiding, abundant fiscal support is likely to keep rates elevated for longer.

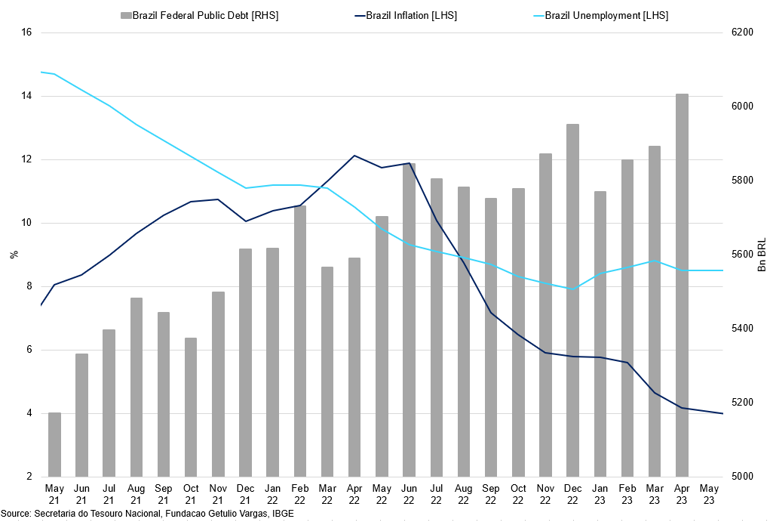

Brazil Inflation vs Unemployment vs Federal Public Debt

Similarly to many developed countries, price pressures continue to soften in Brazil.

Corporate Results

Starbucks

Starbucks beat expectations for quarterly performance in the last few months. Global comparable store sales increased by 11%, with North America up by 12%, whereas international saw an increase of 7%. Out of the international sector, China’s growth was up by 3%. The average ticket – or cost per order – rose by 4%, while comparable transactions increased by 6%. This suggests that customers visited more often and spent more per trip. Consolidated net revenues as a whole grew by 14% to $8.7 billion, thanks to robust growth of store sales. Inflation is not seeing a measurable reduction in customer spending or evidence of customers trading down. Members have been driving most of the traffic, resulting in a record of 56% of transactions. At the same time, the chain opened 464 new stores in Q2, ending the period with 36,634, 61% of which are comprised of the US and China.

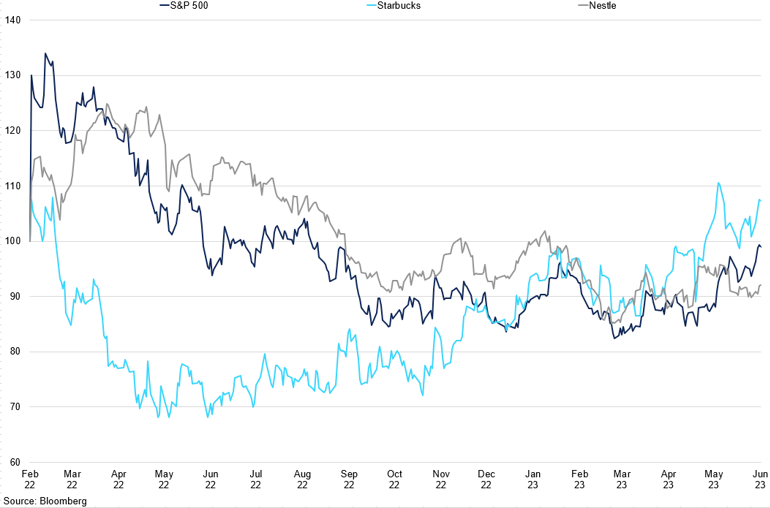

Starbucks vs Nestle vs S&P 500 Performance

Starbucks continues to outperform S&P 500 index, whereas Nestle shares have been seen tailing off in recent months.

Nestle

Nestle’s organic growth was up by 9.3% in Q1 2023, with RIG of -0.5%, impacted by capacity constraints and portfolio optimisation activities. Cost inflation has led to pricing increasing by 9.8%, with coffee products achieving sales growth globally amid a slowing at-home coffee market following the pandemic. While pricing was the biggest contributor to growth in developed countries, positive RIG drove organic growth in emerging markets. The company implemented price increases but still said that they managed the inflationary pressures through disciplined cost control and operational efficiencies. Coffee sales saw growth at a high single-digit rate, with solid growth across geographies, supported by positive sales developments for Nescafe, Starbucks, and Nespresso. In both North America and Europe, the beverages category saw high-single-digit growth. Starbucks by Nespresso and other Nespresso capsules saw their market share increase in the retail segment. In China, coffee saw a sales decrease, as a positive sales development in soluble coffee was offset by negative growth for ready-to-drink coffee. For the rest of the year, the company expects organic sales growth between 6% and 8% and an underlying trading operating profit margin between 17% and 17.5%.

Luckin’

In 2022 the company turned a profit for the first time since its establishment in 2017, with revenues exceeding $10 billion. Since the infamous accounting fraud in 2021, which cost Luckin Coffee a $180 million penalty, the company has been pursuing a strategy of rapid expansion in third- and fourth-tier cities in China. In H1 2023, Luckin’ is set to become the first coffee chain in China to reach 10,000 stores. According to Luckin’s earnings report for Q1 2023, net revenues increased by 84% YoY to $646 million. The company opened 1,137 new stores, resulting in a 13.8% QoQ store unit growth, amounting to 6,310 self-operated stores and 3,041 partnership stores. The company’s business expansion has led to a 57% increase in total operating expenses, coming to $547.3 million.

Supply

Brazil

Since the latest report in March, our outlook for Brazil has not changed considerably, and we have seen prices fluctuating between the 175-190cts/lb area. In the week ending June 13th, specs have increased their positions, now net long at 16,801 lots, suggesting continued appetite from the specs. While fundamentally, we remain constructive about the KC contract given tight fundamentals in Brazil; as of now, we struggle to see prices break above 190cts/lb. We have seen greater selling take place at these levels, keeping the upper ceiling stable. However, the flow out of Brazil has not been as big as we have seen in the past. At the time of writing, 25% of the crop has been harvested, and Brazilians remain price-conscious, selling on rallies than on weaknesses. We believe sales from the region will be executed on an orderly basis. At the same time, we do not expect the prices to fall drastically below 160cts/lb, as there is little hunger from both the specs and the producers to sell the market lower. We would expect decent buying from the industry into lower levels, which should help maintain prices in current ranges.

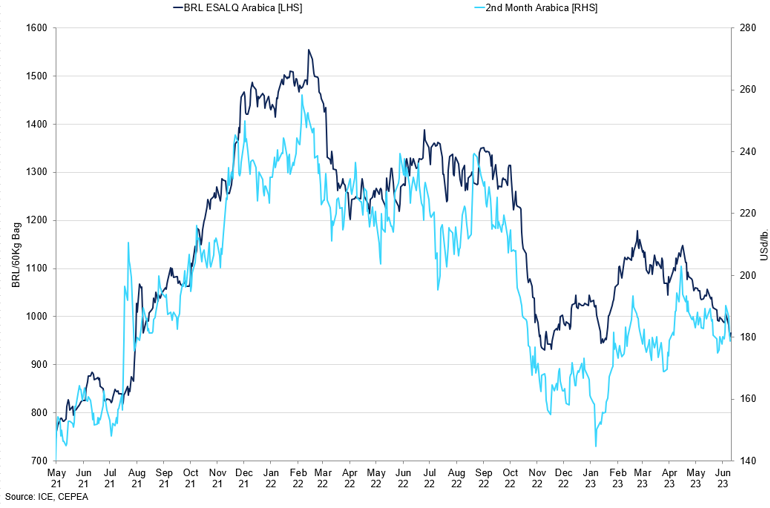

Brazil ESALQ Prices vs 2nd Month Arabica

Both indicators have continued to soften so far in 2023, finding support in recent months.

For the 23/24 crop, our Brazil number is 65m bags, with 44m for Arabica and 21m for Conilon. It marks a 10% increase over the previous crop. When it comes to Arabica, we expect market to remain relatively tight and will keep an eye on the movement over the next couple of months to see whether exports pick up in the July-August time. In April 2023, Brazil exported 2.5m bags, a drop of 12% m/m and a 10% decline y/y. It is a relatively low number given the highs of 3.7m bags seen in the past, and expect that any shipment below the 2.7-3.0m range would create the case for a tighter market. Certified stocks in Brazil are down by more than 200k since mid-March, and are poised to draw down further, given the solid consumption outlook. With high differentials for Central America, Brazil is not pressured to sell at too low a price, which led roasters to buy hand-to-mouth. At the same time, at this stage, farmers are in a better financial situation to carry some stocks and warehouse them well; our carryover number for the upcoming crop is set at 4m bags. Currently, the average price of a 60kg bag of Arabica coffee stands at around BRL1,000/bag. Ultimately, producers in Brazil will pay attention to the flowering for the 23/24 crop in December to assess the yield potential of the next crop; volumes should pick up from January onwards, with more upfront selling into the new year. As of now, the OI data suggests little forward market activity.

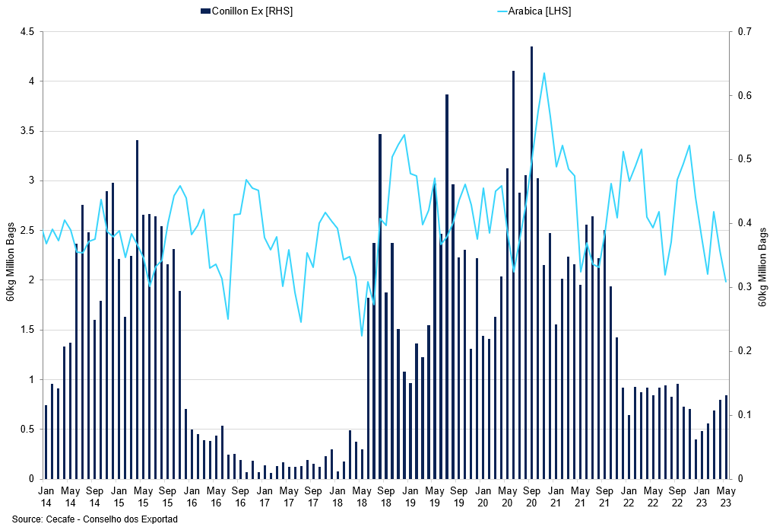

Brazil Arabica vs Conilon Exports

Arabica exports out of the region have been slow, while Conilon is beginning to increase marginally.

Overall, we are friendly the NY contract, given Brazil's presence in the market. It is important to remember that any weather problem in coffee-producing countries around the world could widen the current deficit. One of the big risks for Brazil and other Latin American countries is El Nino, a weather phenomenon characterised by irregular sea surface temperatures that lead to higher air temperatures and storms along the coast of Central and South America. El Nino is forecast to deteriorate the weather conditions by the end of this year, going into 2024, which is around the flowering time for Brazil's 24/25 crop year.

Vietnam

Robusta prices rallied since our last report, jumping above $2,700/mt in June, the highest price level in 15 years. Internal prices have climbed to record highs of VND64,000/kg; the differentials are tight, and the fundamentals point to a tighter supply/demand balance. The Vietnamese coffee farmer has been very price conscious, willing to turn to more profitable plants when returns on coffee prove not rewarding enough. Durian, which is one of China's most valuable fresh fruit imports, has become particularly popular among farmers in the Central Highlands, who increasingly grow it alongside coffee and pepper farms, and we have seen some replacement with durian taking place in coffee’s stead. Moreover, the fertiliser costs continue to affect Vietnamese farmers, negatively impacting the coffee crop. From the demand side, Vietnam's domestic consumption remains unchanged, at 3.0-3.5m bags. If losses in consumption materialise in the US and Europe, they should be easily offset by robust consumption from producing regions.

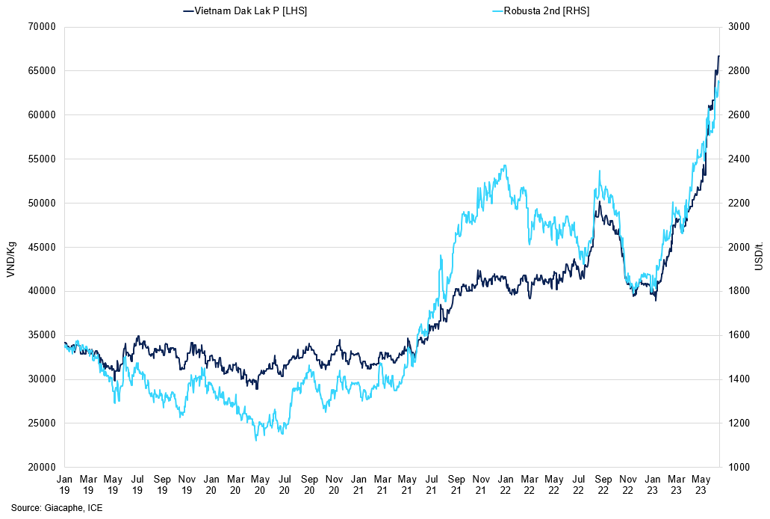

Vietnam Dak Lak Prices vs Robusta 2nd Month

Both prices have rallied strongly in recent months, superseding highs not seen in more than 15 years.

In response to the cost-of-living crisis, the industry has turned more towards Robustas for less expensive blends; however, current weather problems in Vietnam and Indonesia have added a layer of uncertainty to the supply/demand balance. Our Robusta number has been downgraded to 28m for the 22/23 crop year, which is 2m bags below our original expectation earlier this year. For 23/24, our view is at 29m bags, with internal consumption estimated at 3.0m bags. Exports in the current crop 22/23 have already reached 22.471m bags, which leaves 3.529m bags for the five months of the crop cycle remaining. The strength in the spreads underlines the reason we believe prices will remain strong: Sep-Nov is at 93, Nov-Jan – 74, and September-September - at 209 premium. The tightness is set to remain sustainable in the meantime, and this should keep Robusta prices buoyant until the start of the new crop in October/November. With conillon prices BRL700-800/bag, and robust demand from Brazilian roasters, it is difficult to see conillon being shipped to Europe at this stage. Currently, roasters remain behind on paper coverage, and hence, the industry should continue to purchase on dips. While there has been some progress in investments and renovation of coffee plantations in reaction to the rise in prices, we do not expect it to affect supply in the coming crops, as new plants will take time to give higher yields. In the meantime, we see a bigger risk from El Nino, which has a different effect in Southeast Asia compared to Latin America, potentially bringing long periods of drought.

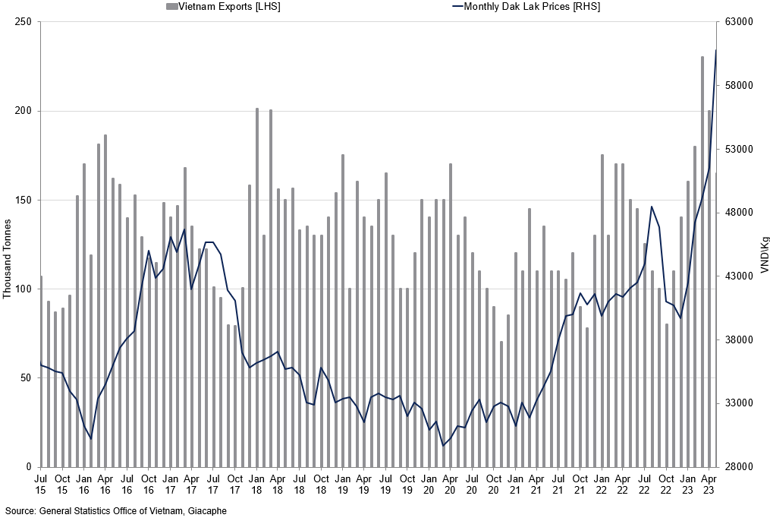

Vietnam Exports vs Monthly Dak Lak Prices

Vietnam exports have been seen lower despite prices posting new highs.

Inventories

Since our last report, we have seen a substantial decline in certified stocks, with a drawdown of more than 230k bags. Arabica's story remains centred around Brazil, and we should see further drawdowns in the coming months. While around 10,000 bags are pending grading in New York as of June 15th, it is not significant enough to impact the fundamentals, in our view. Arabica is down by 213k bags, Honduras by 17k bags, and Peru by 4k bags since March. We expect exports to remain in line with current levels into H2'23 but still softer on a year-on-year basis. Instead, the industry will continue to sell what they need on a hand-to-mouth basis, and after the first flowering assessment in December, we could expect more shipments from Brazil if the outlook for the new crop is positive. Robusta remains the biggest mover in the market, and until we see the new crop in Vietnam, Brazil is not likely to pressure the market. Robusta has been graded regularly, and the stocks were building slightly until May, when they started declining, now standing at 7848 as of June 11th.

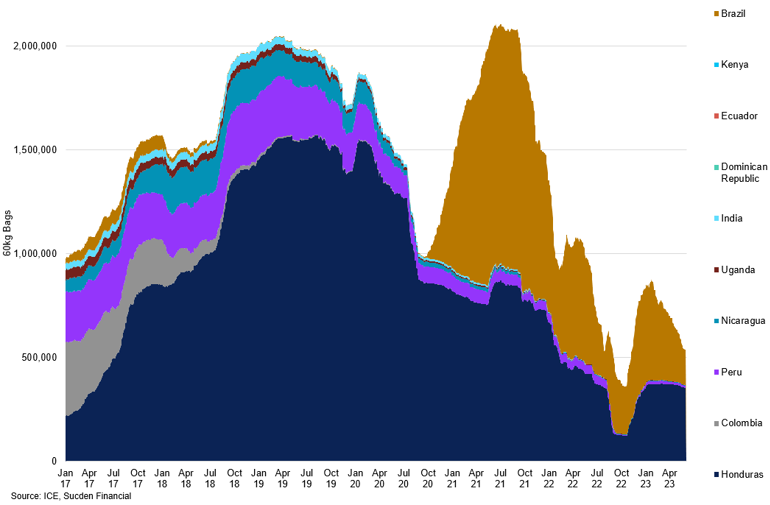

Inventory by Origin

We continue to see further drawdown of coffee from key producing regions in the meantime.

Commitment of Traders'

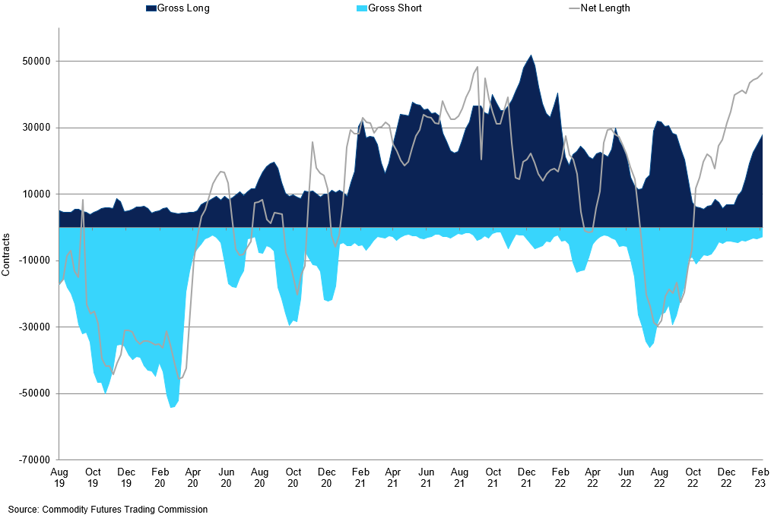

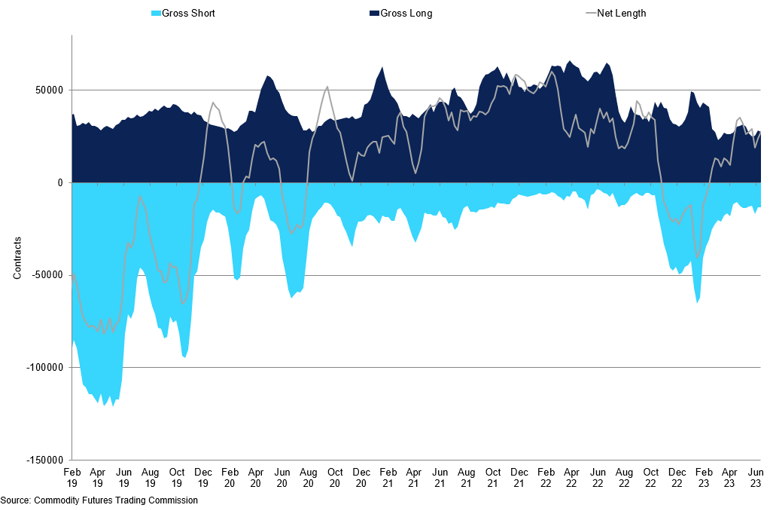

The net length of the managed money for Arabica jumped higher to 16,051 contracts in the week ending June 13th, that is up from the lows of -43,940 in January. This was accompanied by higher prices, rising to test 189cts/lb. When prices are testing the 170cts/lb level, we expect to see higher speculative momentum. In June, we have seen volumes increase, and expect that most of the rise was supported by the growing number of long traders, which is now at 103, while shorts declined to 70. Speculative positioning continues to run a long position, however, reduced from the recent high levels. In current price ranges, we expect the specs to pick up momentum from the lows of 160-170cts/lb; however, at the same time, we struggle to see strong appetite on the upside above 195cts/lb at the moment. We believe there is no strong sentiment for funds to enter unlike in Robusta.

Arabica Managed Money Commitment of Traders’

Specs have reduced their positions slightly in recent weeks, but we believe that more buying is to be done.

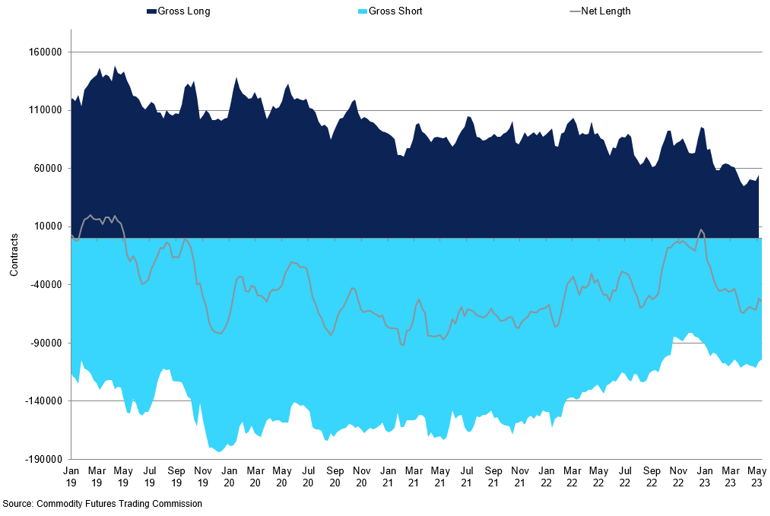

We do not expect that industry will contribute much to the upside in the meantime, but given the need for further coverage, steady buying should take place instead. Commercial positions were net short at 68,863 in the week ending June 13th. Long positions have fell into 45,735 in June, given roasters are still behind the curve and there is still a bit of positioning to be covered; we expect most of the buying to take place on the dip. Short side has sold a bit more, at 114,598 on June 13th. Brazil is price conscious, and we expect farmers are reluctant to sell and put pressure on the market in the meantime.

Arabica Producer Commitment of Traders’

Steady buying should take place given the need for further coverage from the industry.

For Robusta, managed money saw a significant increase in the net length in recent weeks reaching 46,051 contracts as of June 13th. The funds have seen the rally in Robusta and increased exposure; the number of long traders increased to 58. The fundamental tightness is keeping the supply/demand sheet balance buoyant, especially given that we have 5 more months of the crop year. The roaster still remains the biggest buyer, but the momentum is slowing, with commercial longs increasing to 67,276 on June 13th. The overall picture remains strong, differentials remain tight; however, funds are now cautious to enter the market.

Robusta Managed Money Commitment of Traders’