Executive Summary

- Demand has recovered to pre-pandemic levels, and as out-of-home consumption starts to pick up, we could see more traditional consumption patterns.

- Imports into consuming regions have improved, suggesting stronger demand.

- London airports reached 0.62 in the week to July 19th, as airports become busier as people look to get a summer holiday.

- London stations have reached 0.72 up 0.03 on the week and this suggests an increase in commuting and internal travel. This is all but confirmed when you look at sales in the West End as the index increased to 0.77.

- Unemployment levels are rising in the 15-24 age bracket is high, and millennials consume large amounts of coffee. This could dampen demand in the near term, however, it is only a segment of consumers.

- The employment rate for 15–24-year-olds in Q2 2021 in the UK, US, EU 27 are 50.3%,49.8% and 30.8%, for the OECD the employment rate is 39.9%, according to the OECD.

- Demand for coffee is price inelastic and this suggests that as prices rise there will be a limited reduction in demand.

- In 1975, there was a frost in Brazil, and this caused the NY contract to rally to 333.60cts/lb in 1977, the delay was due to the limited communication channels and data availability, in 1994 when we had a draught the certs went to 25,000.

- Brazil exported 45.5m bags between July 2020 and June 2021, this could be revised higher in the coming months.

- Brazil output needs to reach 67m bags to cover local and global demand, using the 56.402m bags for 2021/22 there will be a 10.598m bag deficit in Brazil alone.

- From July 2020 to June 2021 Colombian exports declined 2% y/y with exports at 12.629m bags, down from 12.849m bags in the same period prior, for the Colombian coffee year, exports are flat at 9.479m bags compared to 9.498m bags.

- In Nicaragua, some of the low altitude trees have started to be harvest, but worker availability is a threat to picking.

- Ho Chi Minh stocks stand at 5,968,000 bags, as of the end of July, down 533,000 M/M but up 2,808,000 bags Y/Y.

- 1.1445m bags of ICE certified stocks is from Brazil and is semi-washed coffee, in our opinion this coffee will be consumed. Honduras coffee in stocks is now at 846,891 bags.

- The z-score for the current net position is 1.40, the record is 1.60, the long position z-score is 1.107 with the record at 2.73.

- The Robusta commitment of traders’ shows a net long of 23,037, down from -2,056 as of August 3rd. The long position stands at 25,680 which also declined from the week before.

Macroeconomic Outlook

Global Overview

Global growth accelerated in H1 2021, led by China and the US, as the vaccination rates picked up sharply and the lift of lockdown restrictions unleashed some of the pent-up demand. China, in particular, experienced a sharp rebound in manufacturing at the beginning of the year, and while we continue to see strong positive growth, it is moderating month-on-month. Commodity prices skyrocketed, driven by expectations of strong demand. Therefore, as we move through the second half of 2021, expect to see recoveries diverge, exemplified by some economies already hiking rates, while others continue to provide record levels of support. This divergence is further exemplified by the take up of the vaccine, as we see some economies struggle with the access and distribution of the jabs.

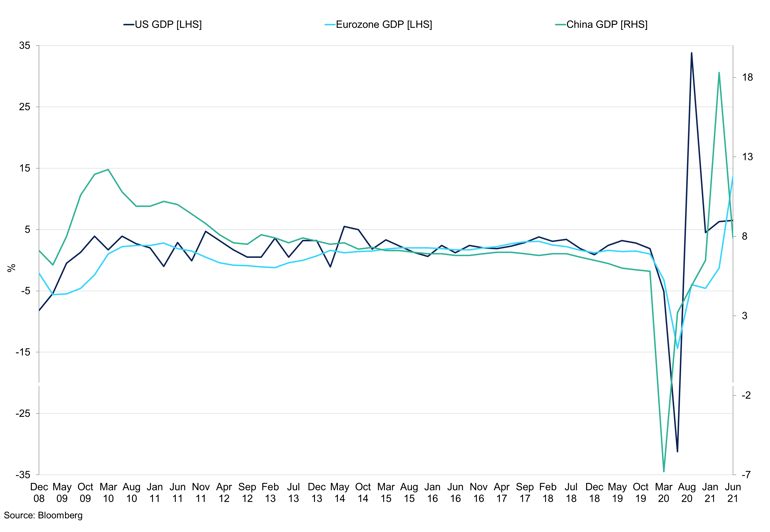

US, China, and Eurozone GDP Growth

Both China and the US experienced a moderation in growth following a strong Q1 performance; Europe, which lifted its restrictions much later in the year grew at a very strong pace as the economy recovered.

Strong institutional demand for US bonds is keeping the yields down, and while there is chatter surrounding the tapering of the bond-buying, the market is not likely to respond sharply until the Fed announces the concrete implementation of plans. While inflation pressures are present, especially from the manufacturing side, the Fed has managed to calm the market's expectations of the price gains this and next year. Even with the decade-high growth in the consumer prices seen in June, the markets did not respond sharply. For July, price momentum is expected to soften month-on-month, which could significantly impact the market perception of the market recovery. The recent adjustment for a more hawkish outlook has surprised the markets on the day, however, the response has been temporary, confirming that the markets are set on the longer-term future expectations. We believe that the inflation spike is mostly transitory, a combination of growth from a low base of 2020 as well as supply-side bottlenecks. We will watch out for the wages in the US and how they respond to tight labour market conditions.

U.S.

The second quarter was strong for US equities, as the S&P 500 reached a new all-time high in June, and this continued into August. Overall, the economic picture remained positive. Q2 GDP grew at an annualised 6.5% q/q, well below the estimate of 8.4%. Growth in consumption was especially strong, as pent-up demand surged to the service sector. Real income and spending both returned to the pre-pandemic levels, despite a fall in government stimulus payments, supported by a relatively high inflation rate feeding into wages. Manufacturing activity moved from 59.7 in March to 63.4 in July. Additionally, in late June, President Joe Biden also secured a deal on an infrastructure package worth about $1tr over the next eight years, falling short of the initial $2.3tr spending plan declared in March.

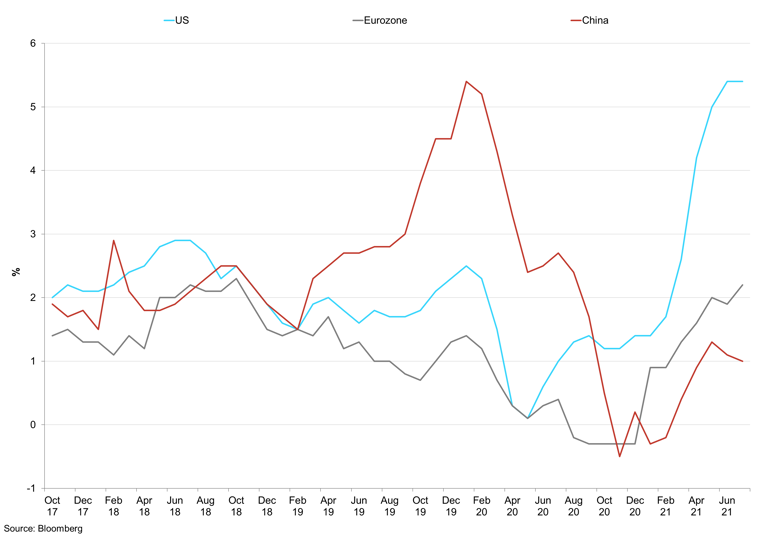

US, Eurozone, China CPI

Both Europe and the US continue to see strong year-on-year growth, supported by the low base growth last year.

We expect strong economic growth in the United States through the second half of this year. Real GDP growth of around 7.0% for 2021 is forecast by the IMF that would mark the best outcome for the US economy since 1984. Stocks growth continued to be robust in the second-quarter earnings season, and we expect the results for Q3 2021 to soften as the economic recovery softens.

Until recently, the US Fed reserve predicted that inflation in 2021 would be 2.4% and for the first interest hike to take place in 2024. Now, that opinion has changed, and the Fed brought forward the first two projected rate hikes to 2023, with the inflation forecast revised to 3.4%. Likewise, it expects GDP growth to jump from 6.5% to 7.0% and stated this change should be seen as a positive change, an indication that the committee sees greater economic growth than anticipated previously. It, however, expects higher vaccination rates in order to completely take the economy out of the pandemic. There were no changes to assets purchases and interest rates in the near term, however, the speculations about the tapering support have been rising.

The Fed indicated that the next change to monetary policy would only take place once the labour market tightens sufficiently to drive a greater risk of inflation. Indeed, the current unemployment level is at 5.93%, 2.33pps more than the pre-pandemic levels, and the Fed expects full employment not until the latter part of 2022. In regard to the inflationary pressures, the Fed believes that they are transitory. Indeed, as the economy reopens, some sectors, including hospitality and retail, enjoy a surge of pent-up demand from the consumers, however, the year-on-year gauge seems to be a poor representative of the growth in prices, given the substantial decline seen in the midst of the pandemic, the month-on-month estimation seems to be more reasonable as we watch the economy develop. Indeed, CPI is up 5.4% y/y in June and 0.9% m/m.

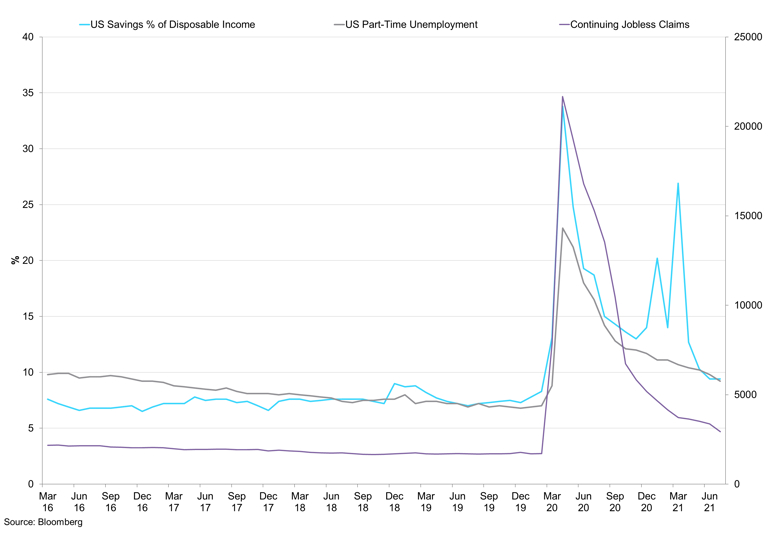

US Savings, Unemployment, Continuing Jobless Claims

Unemployment continues to decline as companies begin to rehire; likewise, the percentage of savings have decreased, driven by lower government support as well as higher spending habits in the recent months.

The Fed has left the rates and the asset purchasing programme unchanged for now, however, it hinted at approaching the decision to taper the purchases sooner than expected. Indeed, vaccination progress and strong policy support, alongside positive economic data, have caused employment to strengthen. The headwinds, however, prevail, as the path to full economic recovery is still largely dependent on the trajectory of the virus spread. A sharp pick up of infections we have seen in the country could once again weigh heavily on the service industry and soften the inflationary pressures we have been seeing for most of the year. On the other hand, an outbreak in Asia could disrupt supply chains even further, possibly leading to a reduction of capacity in factories and ports, putting pressure on manufacturing input costs.

The continuation of falling Treasury yields points to investors' belief of a lower-for-longer policy regimen, with the 10yr yield falling back to 1.20% levels. Moreover, the breakeven rate is lower than a few weeks ago as a response to the Fed statement. The 5yr breakeven rate is still higher than the 10yr breakeven one, reflecting investor belief in higher shorter-term inflation and lower long-term one, which is what the Fed expects.

Retail sales grew by 0.6% m/m in June, by more than forecast, as demand for goods remained strong and consumers shifted their consumption back to the service industry. In fact, retail sales have performed well so far in 2021, with the May figure 18% higher than in June 2020 and well above the pre-pandemic level. Therefore, consumers are spending more money than before the pandemic, and the consumption patterns are changing back to durables, but the lack of supply is causing people to purchase second-half items. Once again, most of the decline came in from automotive sales, which fell 2.0% m/m, which was mostly due to the semiconductor shortage. In the coming months, we expect demand to remain positive yet moderate month-on-month as a result of rising COVID-19 cases, however, with the government keeping the economy open in the meantime, retail sales should be supported on the downside.

Europe

Europe's vaccine rollout has continued gathered pace, with now half of the adult population fully vaccinated, and continued relaxations of lockdown restrictions along with travel supported the recovery. The EU's recovery fund should help continue to support member states, and we expect another quarter of strong growth performance in Q3. The region's post-lockdown recovery is likely to be strong, and GDP should bounce back by around 4.6% this year following last year's near 6.5% decline, according to the IMF. The presence of new variants poses a threat to sustained economic recovery throughout the year, however, we expect the number of hospitalisations and death rates to be low, putting less pressure on the healthcare system. As a result, EU member states began to reopen their economies, which particularly benefitted the service sectors.

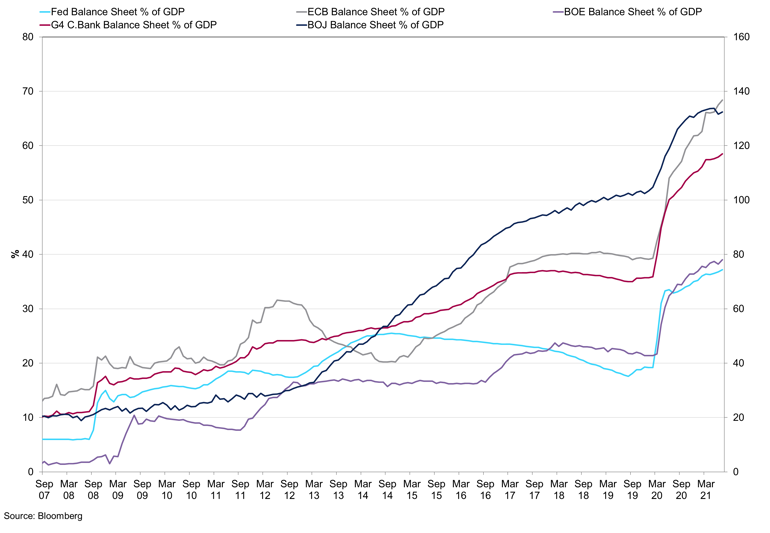

Developed Economies Balance Sheet

The ECB continues to pump a record amount of support into the economy, while other economies are beginning to consider the possibility of tapering bond purchases this year.

Economic data pointed to a strong rebound in activity in Q2, with the latest composite PMI reading at 60.2, the record high. The reopening of industries has supported this, and survey results, as well as tracking mobility, pointed to a rebound in consumption. Tourism, however, remains muted, despite the introduction of the vaccine passports, as rules surrounding the new variant complicate travel. Europe’s service sector has expanded sharply in July, with the Markit PMI picking up to 59.8, the fastest level in 15 years. However, supply chain disruptions and higher producer price pressures continue to persist. Regardless, the bloc’s indices have been mixed, showing buoyancy across the board. Confidence in the economic outlook reached the highest level since the data was first recorded in 2012, highlighting the outlook that, while higher costs persist, the manufacturers are confident about those pressures easing throughout the second half of the year.

From the monetary policy side, the ECB does not want markets to price in for Europe what they are going to be pricing for the US, either in terms of the end of quantitative easing or interest rate rises. This sentiment that Europe is behind the US in terms of recovery has been supported by President Lagarde, who stressed that the eurozone and the US economies are in different situations. The ECB held the monetary policy steady but tweaked the guidance to reflect the recent hike in the inflation target. The central bank committed to purchasing $2.2bn of bonds until March 2022, with this stimulus remaining for the time being. The interest rates have been left unchanged, but the inflation target has been set at 2% over the medium term, suggesting higher inflation is to be expected and will be tolerated by the bank. This means the ECB believes that more support is needed for the economy before monetary policy easing.

China

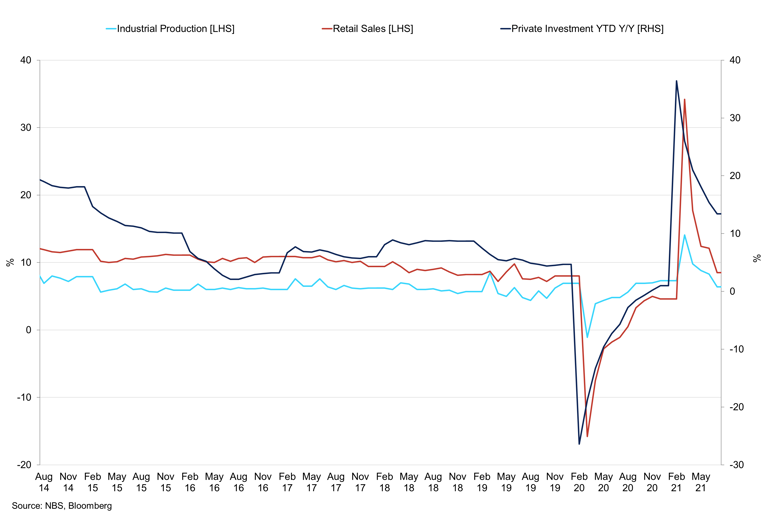

The Chinese economy continued to grow in Q2 with strong performance indices, however, fall short of expectations. Retail sales were up 12.1% y/y in June, the slowest rate of increase since December. The month-on-month growth of 0.70% is, however, is in line with the 4-month average, which means that the industry continues to recover at a consistent pace throughout the year. However, since May 2020, the economy was set on a path to recovery, the growth in 2021 has stalled, and we expect this trend to continue in the coming months. Likewise, from the industry side, industrial production grew by 8.3% y/y in June, the lowest since December 2020. The month-on-month performance has been deteriorating, with the April to June index at the lowest level since the same time two years ago, which is likely have been the result of supply chain issues that slowed manufacturers’ performance as well as a shortage of semiconductors for the automotive sector. In fact, automobile production was down 12.4% y/y in June.

China has been focusing on suppressing the virus locally rather than nationally to prevent an overall standstill across the economy. However, the recent outbreak in the area of one of the major business ports may have significant consequences on the economy’s trade. Indeed, port and shipping delays drove the prices for Chinese goods even higher in foreign markets. However, as of June, the country’s exports surged by 20.2% y.y, driven by the reopening of China’s largest ports. Shipping rates for containers have continued to rise steeply in the weeks since Yantian Port reopened. The increase is widely expected to keep going as stores in the US, in particular, race to restock for returning shoppers.

China Retail Sales vs Industrial Production vs Private Investment

We have seen some moderate growth coming from China in recent months, as the economic recovery loses pace.

The factory gate prices, also known as producer prices, increased by 0.5% m/m in July, still below the May level after a government crackdown on commodity prices took place. Annual rates stayed relatively high and underlined continued strains on the economy. These high levels reflect the fact that strong domestic and foreign demand fuelled increases in global commodity prices, leading to higher producer prices. Indeed, while producer prices in China continue to rise, consumer price increases remain modest, which means the prices have not yet been passed down. China’s CPI was up 1.0% y/y in June, up 0.3% m/m.

Chinese stock markets have struggled over the last couple of months, in part due to increasing regulation on technology companies. The sources that powered China’s recovery, strong exports, property investment and industrial production, remained solid in the first quarter of the year but showed a moderation in Q2 2021. As a result, headline GDP growth slowed to 12.7% from 18.3% in the previous quarter. This is largely driven by the strong base growth in the second quarter of 2020.

The PBoC’s surprise cut in lenders’ reserve required ratio has rocked the markets, left investors speculating on what further steps are coming to bolster the economy. However, the government explains this cut as part of its liquidity operations. The RRR cut should free up around $154bn of liquidity to support interbank liquidity and capital markets as means of repaying matured loans. We believe that debates about the shift in monetary and fiscal policy will continue as the economy sees its growth moderate.

Brazil

Brazil grew at 1.2% q/q in Q1, just below 2019 levels, however, slower than expected compared to the previous two quarters, as intermittent lockdowns in March weighed on economic activity. The surge in cases has dented service sector performance, with service PMI declining from 47.0 in January to 44.1 in March. Likewise, retail sales contracted by 3.9% y/y in February, the lows last seen during the peak of the pandemic in 2020. Most of the growth in Q1 came from business investment, with gross fixed capital formation growing by 4.6% in the quarter. Indeed, the beginning of 2021 has been muted for Brazil, as the rising number of COVID-19 cases alongside fears of growing inflationary pressures have added concerns to the expected recovery in economic growth, further deepening the government’s debt burden.

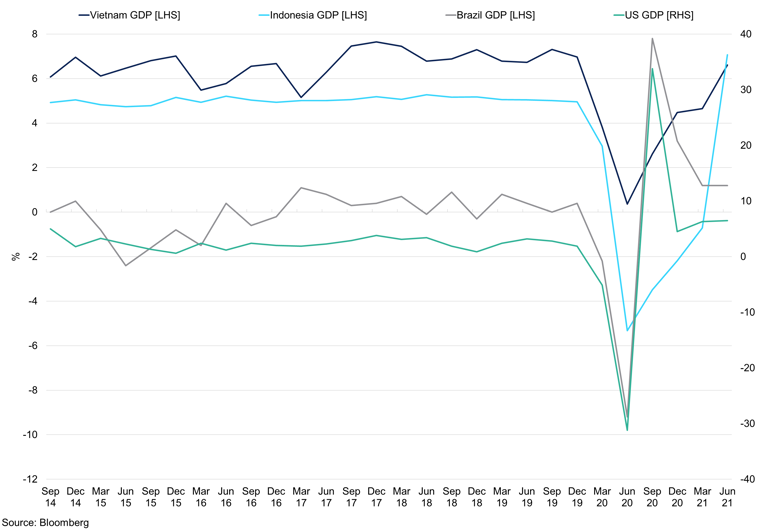

Producer Countries GDP Growth

Indonesia and Vietnam saw strong GDP growth in Q2 2021, driven by the relaxation of lockdown measures.

In July, the picture changed drastically, as the Brazilian economy began to recover, and equities are now outperforming wider emerging markets YTD. The economic recovery still has more room in Q3, after the temporary headwinds from partial lockdowns. This is reflected in the acceleration of high-frequency activity indicators, such as retail sales, which grew by 23.7% y/y in April, the record highs. The rally in global commodity prices, especially in coffee, has been supportive for Brazil, benefitting the external accounts and providing support to the real.

A surge in COVID-19 cases at the beginning of the year has again soured sentiment for Brazil and weighed on economic activity. However, with the cases now seen declining, the pandemic still follows a volatile trajectory, and vaccination numbers are low relative to the population size. As of August 5th, only 21% of Brazilians are fully vaccinated, with another 51% having received at least one jab. From the economic standpoint, inflationary pressures are rising, and it is unlikely that private consumption will witness a strong surge in growth soon. Inflation has been growing over the past year, growing by 8.35% m/m/y/y in June, and has been above the upper limit of Brazil’s target range of around 3.75% since October 2020. While food and fuel have contributed to a general pick up in inflation, the central bank will likely be worried about core inflation, which moved up to 4.7% in June, last seen in May 2017.

The CB has responded to the pick up in consumer prices, taking up the rates by the most in almost two decades to 5.25% from 4.25% in August; this was the fourth consecutive interest rate hike. It also expects to keep the new pace of rate hikes from 75bps to 100bps at next meetings, with the key rate eventually surpassing a neutral level that economists estimate at 6-7%. Indeed, Brazil’s central bank has been among the most aggressive in the world, boosting rates by 325bps since March. The hawkish message will likely lead markets to price in an even steeper increase in rates at future meetings. However, the path to a near-term recovery lies in faster vaccination rates to control the spread of the virus, therefore allowing consumers and businesses to return to normal patterns of consumption. Regardless, the CB is now more confident in the 2021 growth outlook, as it raised its forecast to 4.6% for 2021, up from 3.6%, in line with the market expectations. Stronger-than-expected data measures to preserve jobs and high commodity prices all suggested a favourable outlook for the economy. Growth in H2 2021 is expected to intensify, driven by industry and service sector growth. The CB has also raised its outlook for household consumption to reach 4.0% in 2021 from the previous forecast of 3.5% and for fixed business investment growth to 8.1%. It, however, cut its outlook for government consumption to 0.4% from 1.2%.

While the recovery in most of the sectors has been strong, the nation remains heavily unemployed, with 14.65% of the population without a job in Q2 relative to the pre-pandemic levels of 11.27%. This level is down quarter-on-quarter but still is relatively high to long term averages. And although employment is also at record highs, it is not enough to catch up with the growing number of available vacancies, which should weigh on near term consumer sentiment and spending. The prevalent problem surrounding the labour market has significantly increased President Bolsonaro’s disapproval ratings, which have passed 50% for the first time in July, posing a significant threat to the election win in 2022.

Indonesia

In the Q2, Indonesian economy emerged from the recession, reporting the strongest annual growth rate in under two decades years. Southeast Asia’s largest economy grew 7.07% y/y in the quarter, its first expansion in five quarters, supported by the low base of growth in Q2 2020. Surging exports and a rebound in consumption and investment, and increased government spending boosted activity. However, analysts warned economic recovery would suffer a setback due to a recent surge in COVID-19 infections.

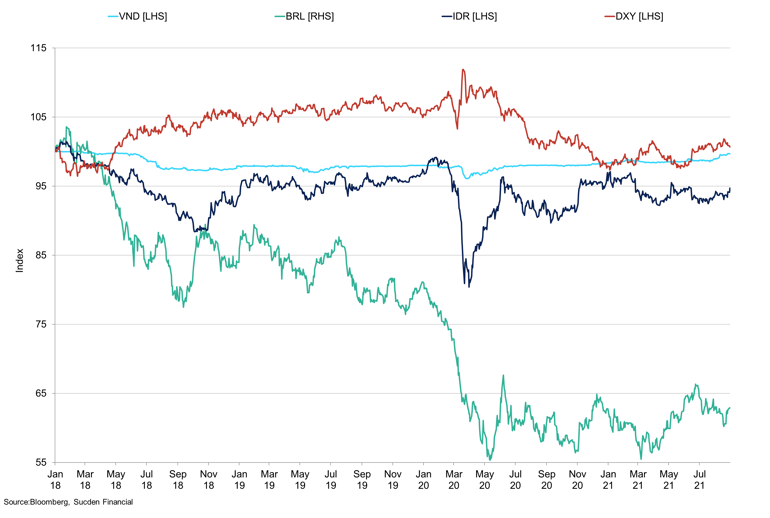

Producer Countries Currency

Most producer currency pairs have been trading sideways for the majority of 2021, only with BRL breaking out of its comfort level in July.

Indeed, despite the above-expectations outcome, markets are downgrading their outlooks for 2021 due to the COVID-19 resurgence and mobility restrictions imposed last month. In July, Indonesia recorded the highs of 50,000 cases and 900 deaths; the vaccination rates remain low, with 20% of the adult population receiving one dose of the vaccine. Consumption and industry activity was relatively robust in the second quarter due to temporarily relaxed curbs from previous virus waves and spending around holidays, with retail sales surging by 14.7% y/y in May and manufacturing still expanding, with the Markit PMI reading at 55.3 in the same month. However, with curbs recently reinstated amid the new outbreak, these indicators are beginning to weaken. Major cities will remain under the strictest curbs until mid-August, with the government shifting its goal to controlling the pandemic. As a result, Indonesia’s CB has cut the forecast for 2021 economic growth to 3.8% from 4.6%. As of August, the cases have been declining, however, the government continues to implement a more restrictive form of lockdown, which could significantly hamper growth for Q3. Some of the more frequent data is already pointing to a softening of economic activity, with the manufacturing PMI falling to 40.1 in July, the lowest since June 2020.

To support the recovery, the CB stated that the rates are to remain low for longer and ample liquidity is provided until the economy recovers. The BI has cut its key rate by 150bps to a record low of 3.50% in February and has kept it unchanged while injecting over $55bn of liquidity into the financial system during the pandemic. Rather than cutting rates further right now, BI stated that they would maintain this low-interest rate and push banks to pass it on. From 2022, the policy will change, as BI could begin tightening monetary next year, including any moves on interest rates, given the economic recovery remains on track to recovery and policymakers see signs of growing inflation. The bank’s exit strategy is similar to other economies, where liquidity is gradually reduced, and the bank would start considering the interest rate action.

Vietnam

Vietnam grew at 6.6% in Q2 2021, up from 4.7% seen in Q1, the strongest since Q4 2019, however, below market expectations of 7%. The industrial sector grew by 10.3% during the quarter, and manufacturing continued to be a key factor in overall economic activity. Growth in industrial output was supported by the recovery in global markets as well as favourable weather for agricultural products; increased government spending also helped drive the expansion. Exports rose 17.3% y/y in June, while imports climbed 33.5%. Manufacturing expanded 11.4% in H1 2021.

The cases picked up sharply in the last month, beating the long term average of 10 per day to reaching 16,000 as of August 3rd. As a result, officials extended strict measures in Ho Chi Minh City and other provinces in the south for two more weeks to provide safety measures around the areas with a higher number of cases while maintaining the normal order in others. Looking ahead, this could significantly complicate the recovery in Q3 and H2 2021. Vaccinations continue to grow, albeit remain low, with 8.7% of the adult population being vaccinated as of early August. On the other hand, robust foreign demand should continue to provide fuel for the manufacturing sector to act as the source of economic growth. For 2021, growth expectations stand at 6.9%, down 0.1 percentage point from last month’s forecast.

In June, consumer prices rose 2.41% y/y, below the government’s upper limit of 4% in 2021, not enough to warrant a rate hike. The Bank of Vietnam stated that it would keep the policy rates unchanged for the second half of the year and pursue more flexible monetary and currency policies as it remains watchful of inflation pressures. However, according to government officials, the revival of demand locally and globally could push inflation as high as 7.8% by December, driven by higher oil prices and recovering global and domestic demand. That would be its highest level since 2012, far beyond the 4% target for this year.

The US has reached a deal with Vietnam to resolve a dispute over Vietnam’s currency that had soured economic relations between two countries during Trump’s presidency, a move that could prevent the threat of tariffs on the nation due to its currency practices.

Corporate results

Starbucks (the quarter ending on June 27th 2021)

Starbucks delivered a record performance in Q3, as the company sales recovered alongside the easing of lockdown restrictions worldwide. As a result of good quarterly performance, the company raised their full-year financial outlook. Global comparable store sales increased by 73%, driven by a 75% increase in comparable transactions.

Americas increased its comparable-store sales by 84%, with the US seeing an increase of 83%. It has also experienced an increase in operating income to $1.3bn from business recovery, as a combination of lower COVID-19 related costs relative to 2020, pricing and benefits of the Americas Trade Area Transformation, which was partially offset by investments in wages and benefits alongside the increased supply chain costs. The pandemic-related costs incurred in 2020 were significant, and service pay for store partners, partially offset by government subsidies.

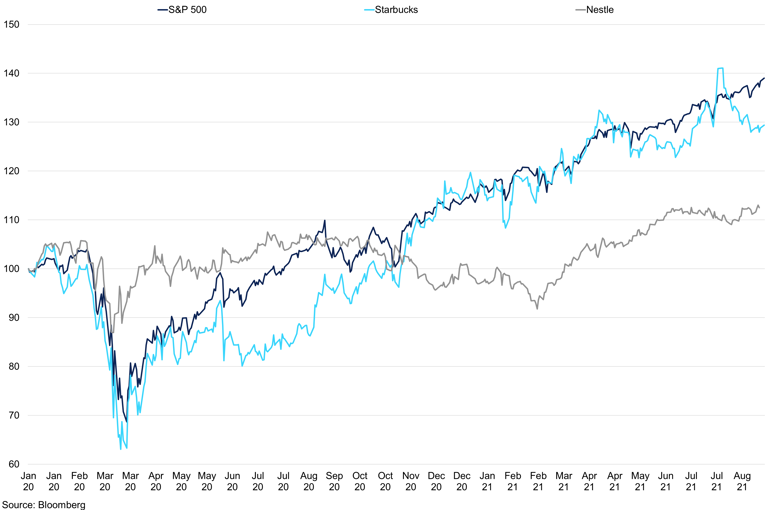

Starbucks vs Nestle vs S&P 500

Starbucks continues to follow S&P 500 index quite closely, whereas the Nestle shares have been seen tailing off in recent months.

The company opened 352 new stores in Q3, a 3% y/y. US and China stores comprised 62% of the company's global portfolio at the end of Q3 2021, with 15,348 and 5,135 stores, respectively.

Internationally, a similar benefit has been felt, primarily driven by higher sales relative to the pandemic levels, including temporary royalty relief to international licensees and higher wages in the prior year and, to a lesser extent, labour efficiencies across company-operated markets and favourability from higher temporary government subsidies. International comparable store sales were lower than in the Americas, growing by 41%, with China growing by 19%.

Additionally, comparable store sales improved, led by a strong performance in the US, as well as significant growth in net new stores in China, where it reached over 5,100 stores during the quarter. The company added over 1m new active Starbucks Rewards members in the quarter. With over 24m active members now representing 51% of all spend in the US stores and up 8pps over pre-pandemic levels. As drive-through represents 47% of transactions and mobile ordering for in-store pick-up/delivery/curbside at 26%, the company is well-positioned for continued recovery.

Nestle

Organic growth reached 8.1% in the first half of the year, supported by continued momentum in retail sales and return of growth in out-of-home channels, increasing pricing and market share gains. By product categories, the biggest contributor to growth was coffee, fuelled by strong demand from Nescafé, Nespresso and Starbucks, with the latter posting a 16.7% growth and sales reaching CHF1.4bn across 79 markets. E-commerce sales grew by 19.2%.

Nestlé continued to expand the reach of Starbucks coffee and tea products outside brand retail stores. Nespresso saw a 14.6% organic growth, reflecting continued expansion of the Vertuo system and robust demand. Growth was fuelled by new consumer adoption, a return to positive growth in boutiques and out-of-home channels, as well as innovation.

The report showed slower growth in the APAC regions comparing to other locations due to the continued economic difficulties and struggles after the impact of the pandemic; high single-digit growth in Malaysia and Vietnam was offset by a decrease in the Philippines. In the AOA regions, Nestle recorded a 6.8% organic growth.

For 2021, organic sales growth is expected to be in the 5-6% range, with the underlying trading operating profit margin at 17.5%, reflecting time delays between cost inflation and pricing. Sales were mostly driven by the AMS region, with EMENA and OAO the following suit. North America posted mid-single-digit growth. Beverages, including Starbucks at-home products, Coffee-mate and Nescafé, saw high single-digit growth.

JDE Peet's

Total organic sales grew by 4.2%, supported by in-home momentum, fuelled by single-serve and beans growing double-digit. E-commerce grew by 30% for in-home channels. Away-from-home picked up, despite the relatively high growth base in H1 2020, with reopenings taking place in Q2 2020.

Although inoculation programmes worldwide continue to support the gradual relaxation of lockdown measures, the COVID-19 situation remains highly volatile and uncertain as spikes in infections continue to lead to new lockdowns. This continues to cloud outlook regarding the timing and the pace of the recovery in our away-from-home channels. With that, the company expects organic sales growth of 3-5% in FY21, assuming a gradual recovery in away-from-home.

In H1 2021, total sales increased by 4.2% on an organic basis. In-home channels continued to deliver strong organic sales growth of 4.9%, while sales in away-from-home remained relatively stable (+0.7%).

Whilst most countries contributed to positive sales growth, a particularly strong performance came from countries like South Africa and Brazil. Various markets in the APAC region entered into new lockdowns in the course of H1 2021, which, in many cases, were stricter than the lockdowns seen in 2020, therefore, further impacting the away-from-home channels. As a result, sales performance in various markets in South-East Asia declined; however, China delivered strong double-digit performance. In the US, as the country started to reopen in the first half of the year, consumption started to shift back to the coffee stores.

Demand

Coffee consumption has been improving in line with the re-opening of the global economy and the number of vaccinations in key consuming regions. As of August 2nd, the UK had 57.8% of the population have been vaccinated with 85.5m doses given, the European Union have administered 474.6m doses which represents 49.5% of the total population, G7 has given approximately 805.8m doses which equates to 48.3% of this region’s population fully vaccinated. The US has administered an impressive 342.9m vaccines and now 49.9% of the population have received both doses. However, the delta variant has spread across the US even though the number of confirmed cases has fallen, this is attributed to less testing and could help to explain some of the declines in the UK. Vaccination rates have started to slow as the younger generation are less willing to get the vaccine, however, governments have started to implement the need to a vaccine for nightclubs, bars, and pubs. The UK government have started offering incentives for the younger population to get the vaccine.

Producing regions are generally behind the curve when it comes to vaccinations, with 19.7% of the population having had both doses. Peru, Indonesia, Honduras, Nicaragua at 16.6%, 7.9%, 3.2%, 2.5%, respectively. This presents headwinds to harvests, husbandry if these regions see another wave of cases. However, for demand, Brazil is the only real threat to our global consumption number as the other origins have a lower demand figure. ICO figures suggest that for March indicate that arrivals are increasing, Europe reached 6,808,000 bags beating the October 2020s figure of 6,805,000 bags, this indicates consumption is improving. We anticipate these figures will continue a higher trajectory in the superseding months as consumption improves. The U.S. imports reached 2,418,000 bags in March, up from 2,228,000 bags in February. The trajectory of imports for consuming regions will continue to climb in the superseding months as economies open. The delta variant does present headwinds to growth expectations if we see a reversal of some restrictions. We see this as unlikely at this time as governments are suggesting rhetoric of living with the virus. We continue to emphasise the risk is of low vaccinations in emerging countries.

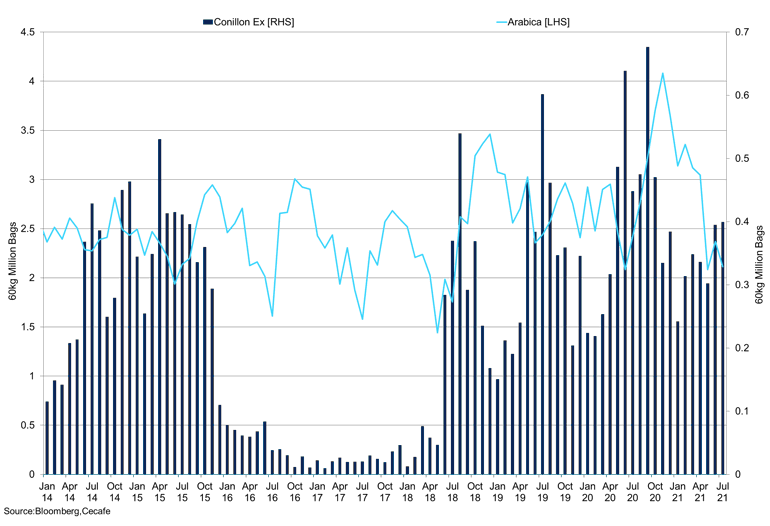

Brazil Conillon vs Arabica Exports

Brazil Exports have been falling as the crop year comes to a close.

As reported in the corporate earnings data above shows, organic coffee sales have been strong with Nestle, in particular, showing strong growth. Ready to drink beverages are expected to be a growth area for Nestle, as they look to strengthen their partnership with Starbucks. The new collaboration between the two companies will intend to bring ready to drink beverages to market in 2022. Due to the strong global demand for coffee and sales beating forecasts we have increased our global consumption number. However, there are still threats to demand in the long run as unemployment levels will edge higher in Q4, but we expect them to fall again in 2022 as companies grow. We have seen robust demand from millennials and generation z in recent years however, these are the age brackets most impacted by covid-19. Indeed, the employment rate for 15–24-year-olds in Q2 2021 in the UK, US, EU 27 are 50.3%,49.8% and 30.8%, for the OECD the employment rate is 39.9%, according to the OECD. For reference, the employment rate for 25–54-year-olds for the US, EU 27, and OECD are 77%, 79.5%, and 76.8%, respectively. Lower employment for the 15-24year-olds could impact consumption when you factor in higher prices. Even coffee is inelastic, we expect some drop-off in demand because of higher prices as companies pass on costs to the consumers. We do not expect a significant decline, in-fact consumption will increase in the 2021 calendar year. In the U.S. data from Opportunity Insights shows that high-wage workers (>60k per year) employment is 7.4% above where it was in February 2020 as of May 5th 2021, contra to this low-wage employment ($27k per year) is down 21% in the same period. The higher employment in high-income brackets will prompt a positive multiplier effect and in time lead to higher low wage jobs.

The Pret Index created by Bloomberg outlines the transactions at Pret A Manger Ltd at airports in London and New York as well as major shopping locations in London, Hong Kong and New York. The index saw sales in stores rise by 1/5th in the week to July 29th. The index works on a scale of 0 to 1, with 1 being pre-pandemic sales, every point (0.01) represents 1%, London airports reached 0.62 in the week to July 19th, as airports become busier as people look to get a summer holiday. London stations have reached 0.72 up 0.03 on the week and this suggests an increase in commuting and internal travel. This is all but confirmed when you look at sales in the West End as the index increased to 0.77. Intriguingly sales in the City are only at 55% of pre-pandemic levels as workers continue to work from home. While this index is not solely coffee sales, the index gives a strong indication of where consumption is at. In recent reports, we have indicated a shift from coffee consumption to residential areas, and also in-home, and the index helps to confirm this with London suburb consumption at 1.02 as of July 29th. The index also covers New York and midtown and downtown sales are still low compared to pre-covid, at 0.52 and 0.4 respectively. Downtown sales indicate that workers are still not back in the office and google mobility data indicates that’s sales in London City are recovering faster than New York’s financial district.

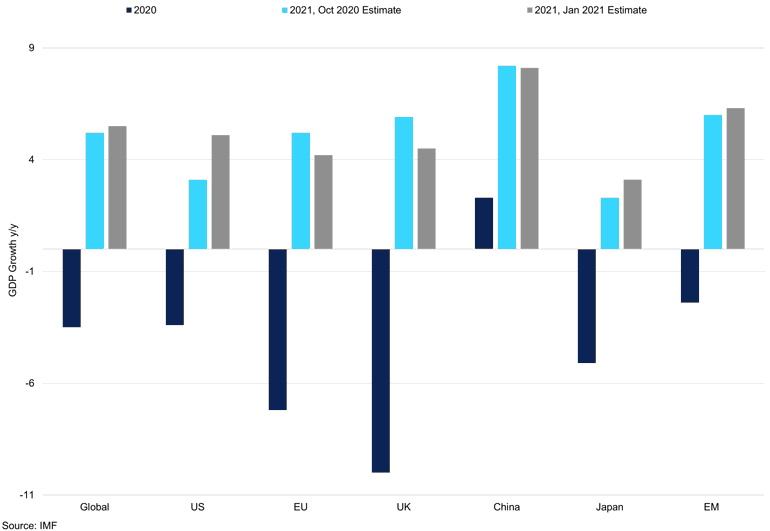

IMF Economic Growth Forecasts

IMF is forecasting robust economic growth this year, but unemployment is a headwind to demand.

As a result of strong sales results, and improving Pret Index, and rising imports into consuming countries suggests that demand is strengthening. As a result, we have moved our consumption number from 165.5m bags to 167m bags for the 21/22 season. Demand in the US, despite the Pret Index from New York, is improving and home consumption is higher and has offset the weakness elsewhere. Starbucks and Nestle results indicate this, but we do see some drop off in consumption as a result of higher prices and unemployment levels. We see demand resumption in major consuming areas in the remainder of the year, we do not see new variants as a major threat to demand as this path is well-trodden now. As mentioned, higher prices will be a concern in the long run especially as the damage from the frost and drought are still being quantified. Consumption is expected to remain high and we would expect the certs and inventories to draw quickly. Asia pacific demand will continue to grow in 2022, and this is represented in the JDE, Starbucks, and Nestle’s earnings results.

In our previous demand reports we have highlighted that coffee demand is inelastic, we highlighted that in the 2008/2009 and 2010/2011 seasons the price elasticity of demand was -0.44 and 0.098, respectively. Higher prices this year and next will prompt a moderate decline in coffee consumption, however, we do not expect significant demand destruction in major economic regions. Brazil is an area where demand may soften, however, we know a large proportion of this coffee is consumed on farms, but with the crop lower in 21/22 and 22/23 this will reduce carryover, local stocks and availability for Brazilian consumption. In order to maximise earnings farmers will sell as much coffee as possible, it is also worth factoring in that producers have sold coffee they do not have, and will not only default, but reduce origin consumption to limit losses.

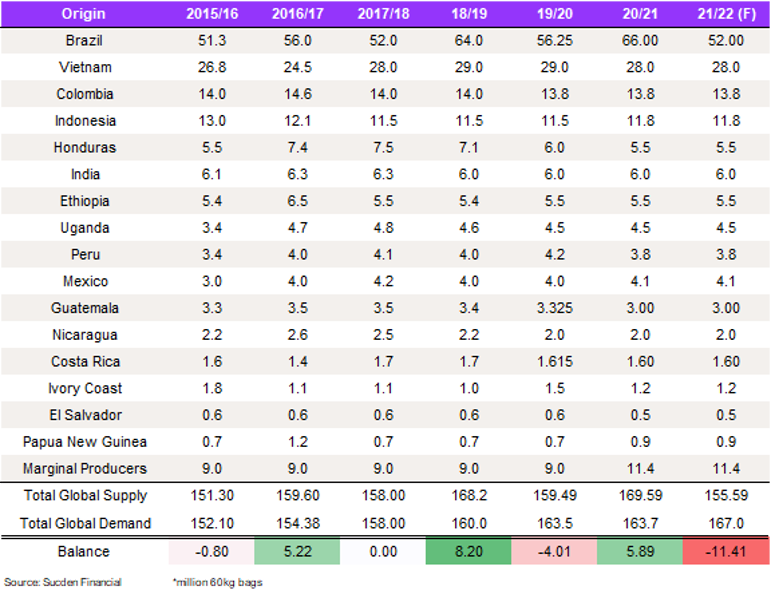

Sucden Financial S&D Balance Sheet

Supply

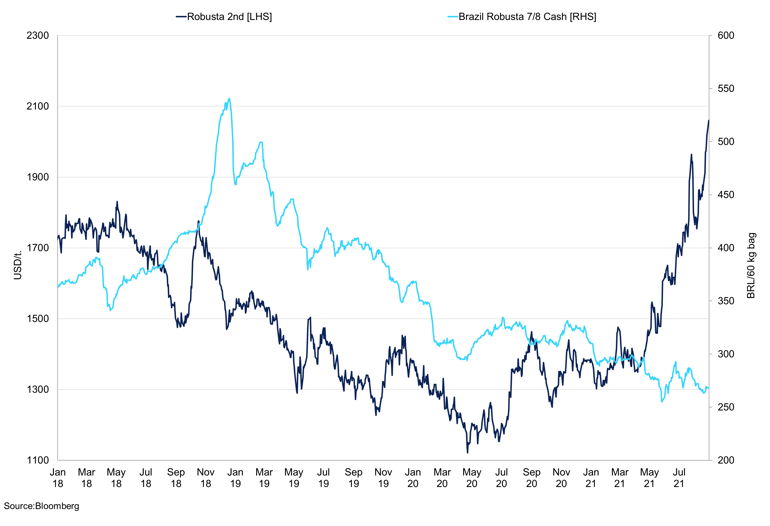

Brazil Robusta 2nd Month vs Brazil Robusta 7/8 Cash

Robusta local prices have remained low compared to London prices.

In our April report, we highlighted that weather in Brazil has been less than preferential for a record crop, but we indicated that there was a long way to go. What superseded this was a period of draught and frost, something that has never happened before. In 1975, there was a frost in Brazil, and this caused the NY contract to rally to 333.60cts/lb in 1977, the delay was due to the limited communication channels and data availability, in 1994 when we had a draught the certs went to 25,000. The draught and frost caused significant damage to Brazil’s crop, as things stand, we see 10m bags of damage to the 2022/23 crop. Some regions of the Cerrado have seen up to 60% damage, with the total region around 30%. In our opinion, the damage will go into next year as well as the yield is damaged, young trees will be impacted more. It is also worth considering that in September and October in the last 2-years weather has been dry impacting the flowering. If this happens once again, we will see the yield fall further. Considering the 22/23 crop was meant to be an on-cycle and the Arabica crop could have been 49/50m bags, as things stand our crop for Arabica crop number is 39m bags, with Conillon at 21m bags. This brings our total figure for 2022/23 to 60m bags, this comes off the back of a 32m bag Arabica crop in Brazil.

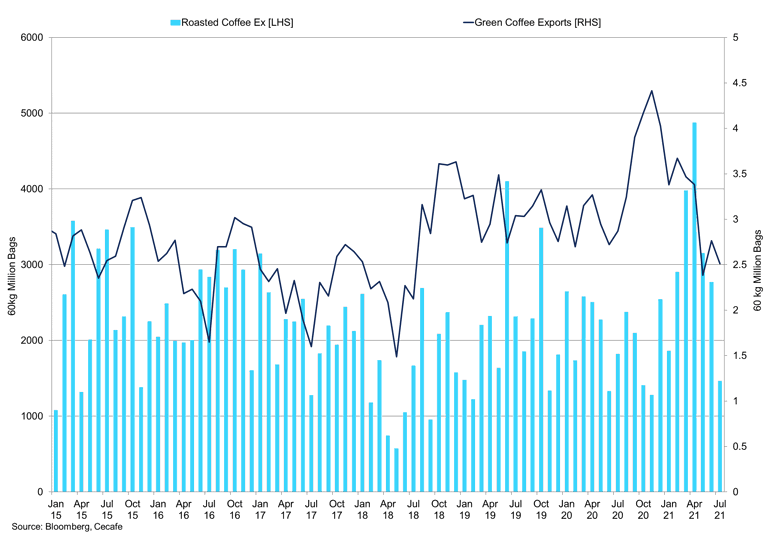

Brazil Roasted Coffee vs Green Coffee Exports

Green coffee exports have declined and as we enter into the deficit year, they will remain low.

For the 2021/22 season, our Brazil crop figure is 53m bags for Brazil with a 3.4m bag carry-over taking total availability to 56.402m bags. Brazil exported 45.5m bags between July 2020 and June 2021, this could be revised higher in the coming months. The breakdown of the 45.5m bags was 36.917m bags Arabica, 4.7m bags Robusta, and 3.936m bags soluble, this is approximately 60% of global Arabica exported worldwide. As a result, Brazil output needs to reach 67m bags to cover local and global demand, using the 56.402m bags for 2021/22 there will be a 10.598m bag deficit in Brazil alone. From January to December 2020 Brazil shipped a total of 44.7m bags, which was 35.62m Arabica, 4.927m Robusta, and 4.131m bags of Soluble, between July and December in 2020 shipments reached 24.732m bags, 19.835m bags of Arabica, 2.78m Robusta, and 4.131m Soluble. Shipments from Brazil will fall year-on-year, as of June exports have totaled 20.86m bags, 19% of this coffee has been shipped to Europe, shipments have trended lower in since February, and we expect exports to edge lower in the near as the new crop filters through, however this is likely to be for a brief period. Farmers are not offering any product and Brazil Swedish prices have edged lower to -19 from -20 the previous week, local Arabica prices are at R$1,015.3/bag at the time of writing, this is just off the high of R$1,067.27/bag, Robusta prices are considerably lower at R$615/bag. Our global figure at 155.59m bags, with demand improving, we moved out global consumption figure to 167m bags, meaning an 11.41m bag deficit for the 2021/22 season.

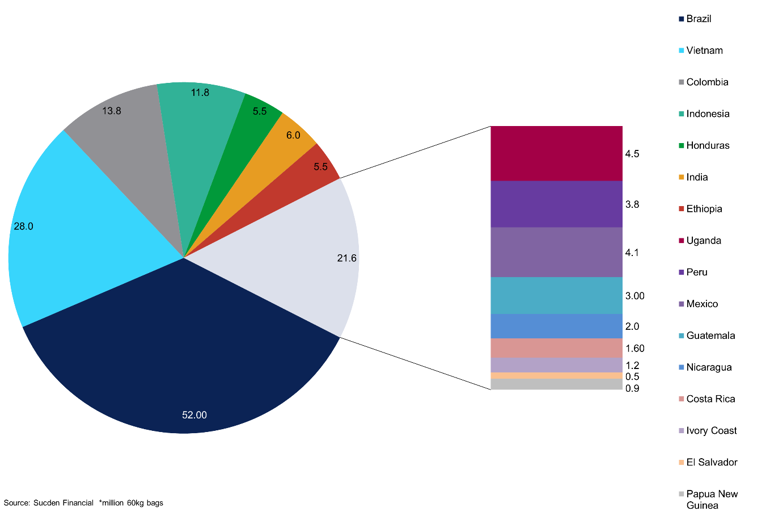

Sucden Financial Supply Pie Chart

Colombian and Central America

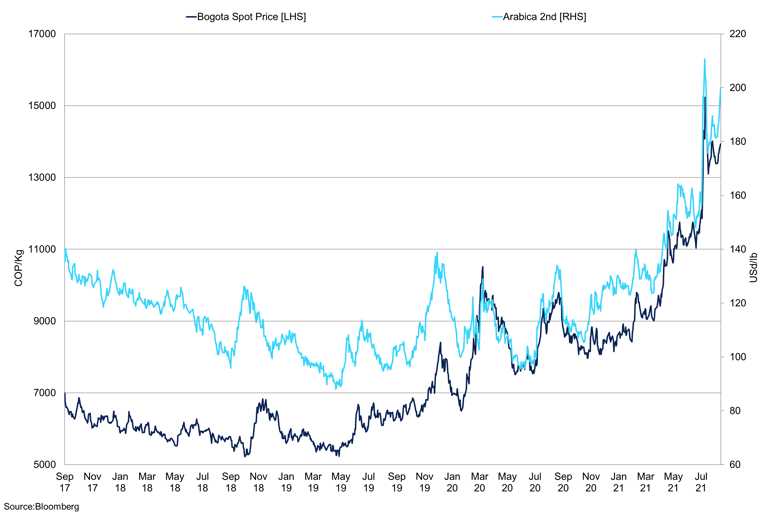

Colombian Bogota Spot Price vs 2nd Month Arabica

Local prices have rallied significantly in line with the C contract. Diffs also remain firm.

Exports in June were down year-on-year by 11% reaching 986,000 bags, down from 1.11m in June 2020. From July 2020 to June 2021 exports declined 2% y/y with exports at 12.629m bags, down from 12.849m bags in the same period prior, for the Colombian coffee year, exports are flat at 9.479m bags compared to 9.498m bags. As mentioned in our previous report, Buenaventura which exports 60% of Colombia’s coffee saw significant blockades, the logistical work being carried out will last no longer than 40 days. This should see exports start to improve after these works. In July we expect production to improve marginally, back above 1m bags but still down year-on-year. Differentials in Brazil are still high at 50 over, and there is no real prospect of this falling in the immediate term despite exports and production edging higher, local business is still quiet. With exports down from Colombia and Brazil also struggling, this helps to confirm the deficit in the Arabica, in our opinion, the certified stocks will draw sharply in the coming months as roasters who don’t have enough product buy this coffee. We could also see a change in blend, with more Robusta and semi-washed Arabica used, even though local Conillon prices in Brazil have reached 11 over.

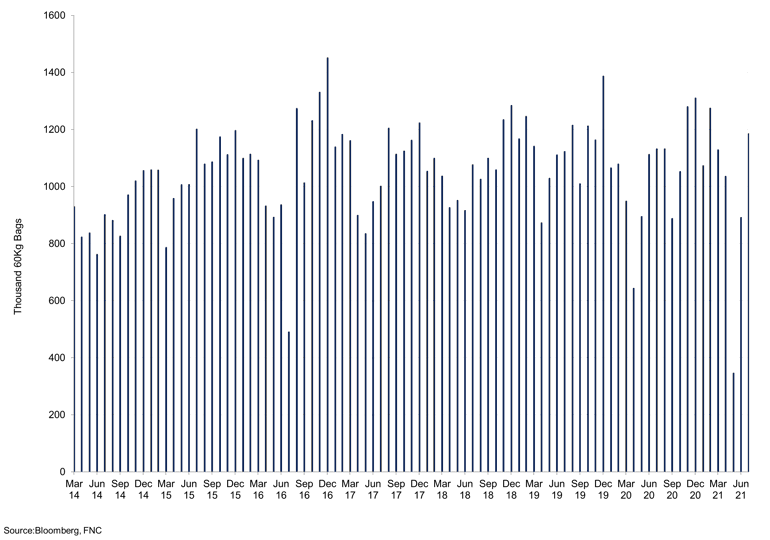

Colombian Monthly Exports

Blockades and logistical problems have caused Colombian exports to decline.

Honduran exports have started to recover, with shipments up 123% y/y in July, cumulative shipments have now reached 5.286m bags, up 2% y/y. We expect this to go to straight to industry, with demand improving and supply elsewhere declining. We hear that farmers are preparing for the new crop, and while COVID remains a threat, and this could present headwinds to shipments. Honduran differentials have stayed at 20 over in recent weeks. Outside of Honduras, Central America has seen some disruptions with Costa Rica nearly completely sold and most set of export. Exports were down 9.8% y/y in July due to lower availability, exports were 124,843 bags in July according to ICAFE, down from 138,386 bags in July 2020. July data was the first time in 4-months of rising shipments, shortage of labour did slow the harvest and cap exports. In Nicaragua, some of the low altitude trees have started to be harvest, but worker availability is a threat to picking as we could see migration to the U.S. or other Central American countries. The crop is expected to be good quality and we maintain our number at 2m bags for the 21/22 crop but given the good bean development, this could edge higher in the coming months, assuming there are no picking issues.

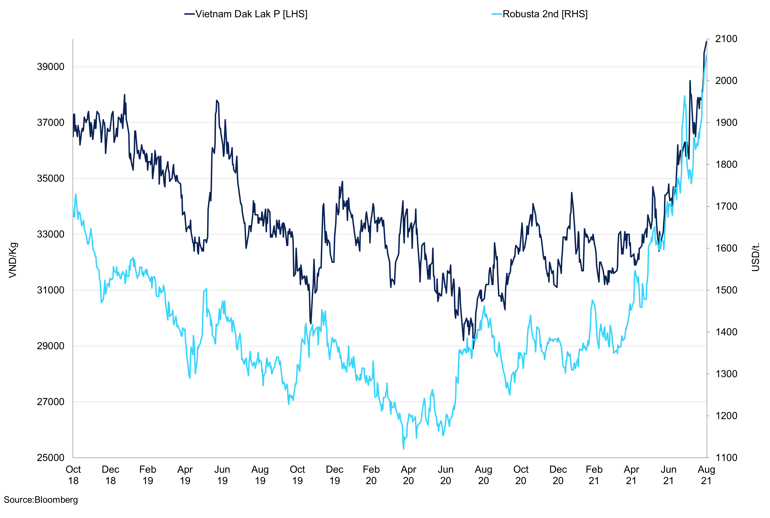

Vietnam Dak Lak Robusta Price vs 2nd Month Robusta

Robusta prices have been well bid but we do not see a deficit in this coffee.

Vietnam

Vietnam grade 2s are trading around – 60 FOB for nearby shipments but the market remains quiet, diff have weakened as the flat price has rallied suggesting an efficient market. The rise in COVID cases and lockdown has slowed exports, this has compounded the issues with high shipping costs and container availability causing the exports to stay low. July exports were 110,000 tons, marginally lower than the same month in 2020 when shipments were 120,000 tons. Ho Chi Minh stocks stand at 5,968,000 bags, as of the end of July, down 533,000 M/M but up 2,808,000 bags Y/Y. The year-on-year figure shows how problematic the lockdown, high shipping costs and low availability of freight has been. There is demand for Vietnam coffee but more on the gap-filling side of things. Local prices have edged lower after testing appetite above $38,000VNK/kg, price trade at 36,500VND/kg. We will see more orders for the new crop in the coming months, but we are yet to see if this crop is impacted by the lockdown, there is a threat from reduced husbandry. We maintain our number for 21/22 at 29m bags for Vietnam, this in conjunction with the Conillon crop in Brazil will keep the market the Robusta market in surplus for this year. As mentioned, we expect some changes to blends with more Robusta being used to counteract the lower Arabica availability.

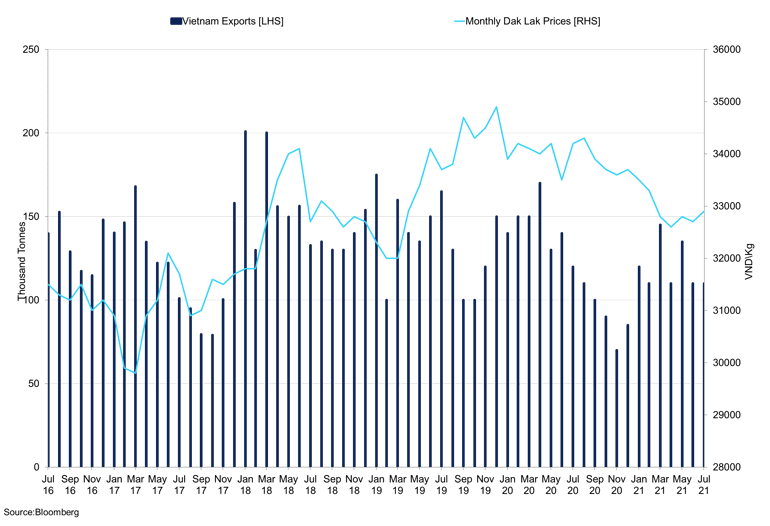

Vietnam Exports vs Monthly Dak Lak Prices

Vietnam exports have been hampered by container and logistical issues.

Inventories

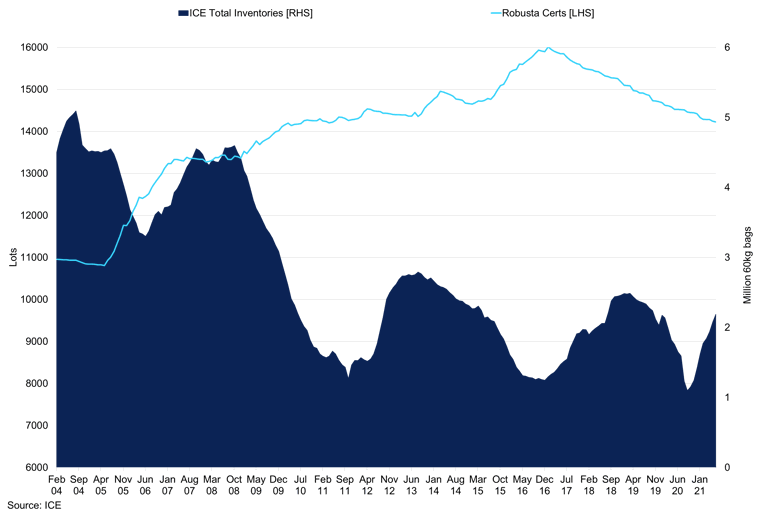

ICE Total Inventories vs Robusta Certs

Certs have increased due to the semi-washed Arabica from Brazil, but inventories are historically low.

ICE inventories have been rising in recent months and stand at 2.15m bags as of August 11th, in recent reports we said that we expect inventories to draw in line with lower exports from Brazil and robust demand. However, stocks continued to climb, we maintain our view that stocks will fall as we enter the deficit year, we have heard of large proportions of sales of certified stocks and we expect roasters who have not covered or bought enough product to purchase this coffee. 1.1445m bags of ICE certified stocks is from Brazil and is semi-washed coffee, in our opinion this coffee will be consumed. Honduras coffee in stocks is now at 846,891 bags, we see people re-grading coffee and some of it has a time penalty but once again, even though Honduran exports have improved with the current deficit at 11.4m bags and the prospect of another low crop next year, because of the frost, and an off-year after that, we do not anticipate much coffee to head into inventory. GCA stocks have been falling in 2021 and stand at 5.779m bags, in our opinion stock withdrawals will increase in pace in the coming months. EU certified stocks have also been declining and now stand at 14,282 lots, Ho Chi Minh stocks are higher on the year as mentioned above this is due to higher shipping costs and lower freight availability. With Arabica availability lower for the 21/22 season, we may see more Robusta used by roasters who look to adjust their blends.

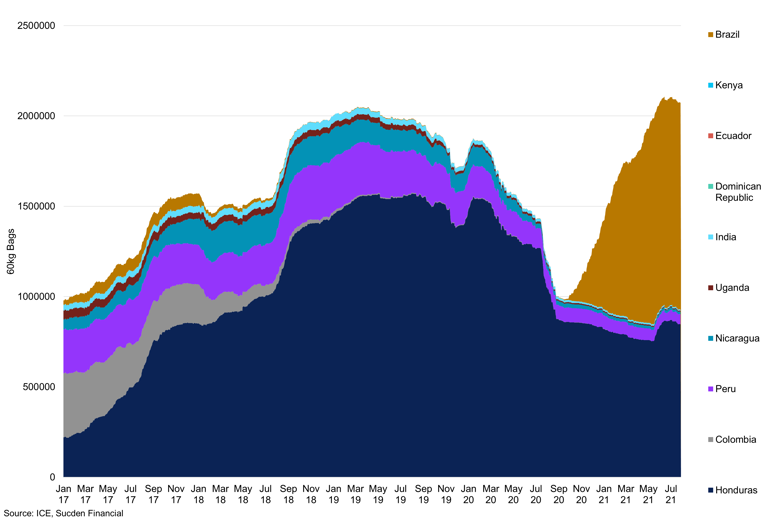

ICE Arabica Certified Stocks By Origin

Brazil and Honduran coffee represent the vast majority of stocks.

The commitment of Traders’

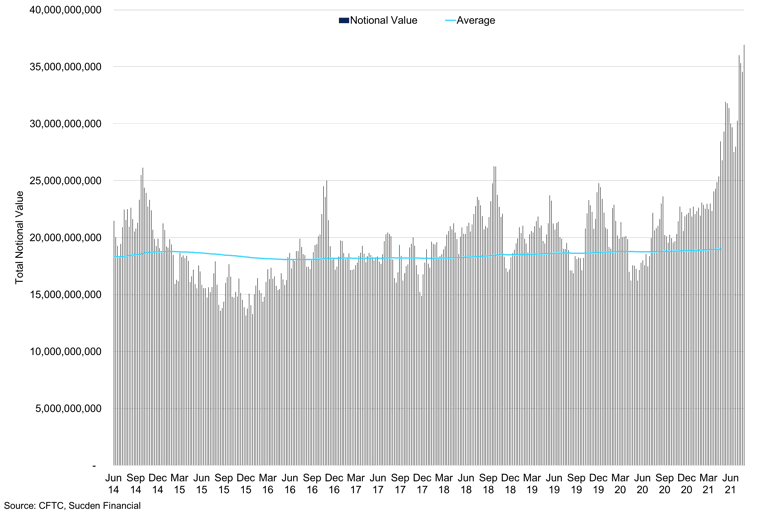

Notional Exposure by the Coffee Market

Exposure has increased due to the rally in prices but the funds have the capacity to add.

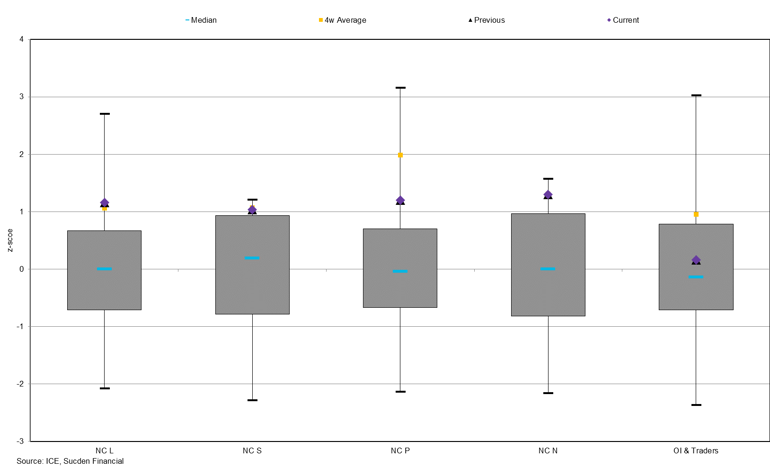

The non-commercial net position stands at 30,644 long, as of August 24th, spreading stands at 112,570 contracts, an increase of 2,728 contracts. The number of traders declined moderately to 155, which is marginally lower than the July high of 178. We expect this is due to some traders being stopped out when prices sold off sharply after testing appetite above 200ts/lb. The non-commercial long position has also declined since July 20th when it stood at 52,889. In June the long position stood at 61,482 contracts, this suggests that there is plenty of spare capacity from the fund community to push prices higher. Even though the fundamental outlook is bullish, the higher margins being charged by the exchange in conjunction with high volatility suggests that traders need to have deep pockets, and as a result have stood on the sidelines to some extent. We expect this to change but would favour deferring a position down the curve. The z-score for the current net position is 1.29, the record is 1.60, the long position z-score is 1.16 with the record at 2.70. The OI and number of traders z-score is at 0.15 which is significantly lower than the record at 3.03.

Arabica Non-Commercial Normalised Report

There is ample capacity on the upside for the long position, and the OI is above the 4-week average.

The commercial short position stands at 191,033 as of August 24th, a slight decline from recent record highs. The large gross short is something that will continue to present issues going forward as the majority of this is Brazil hedging and there is coffee being sold by producers that they don’t have. Producers have also sold forward, and we expect defaults to occur. The net commercial short is 96,284 contracts, as the long position is 94,749 contracts. Roasters are behind the curve and need to cover, but also will buy certified stocks. The z-score for the short position is at -0.85.

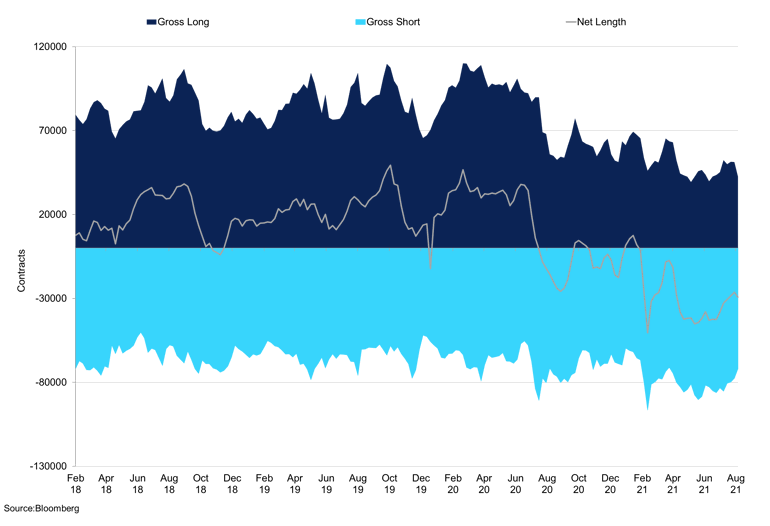

Robusta Producer/Merchant Commitment of Traders

The commercial short has remained high in recent months but the net position has declined.

The Robusta commitment of traders’ shows a net long of 19,801, up by 1,224 as of August 24th. The long position stands at 22,859 which also increased from the week before. The futures and options position combined has a net position of 20,598 contracts. The producer net-short is 36,326 as of August 24th, down 7,444 contracts from the week before. Combined futures and options net position stands at -29,284 contracts, with the net long at 42,563 compared to a short of 71,847. The fundamental outlook for Robusta is less severe, but we expect greater uptake this coffee.