Executive Summary

- We believe that coffee prices are set to rally for the remainder of the year

- Central bank balance sheets have risen sharply, helping to provide liquidity and supporting asset prices

- Risk aversion is starting to return but the sentiment is vulnerable to a downside correction

- It is too early to say for sure the impact on coffee demand due to COVID-19, we believe that at-home consumption will offset some of the loss in out of home consumption

- We think the speciality business may struggle due to the loss of employment and consumer income

- Furlough schemes have helped support coffee consumption in the near term, despite the rise in the savings ratio

- Once these schemes finish we expect a large proportion of furloughed employees to be made redundant

- Coffee consumption is inelastic but the recession may trigger a reversion to traditional blends, away from speciality

- Latin America is now the epicentre of the pandemic and Brazil’s handling of the virus has raised alarming questions

- We could see some downside to Brazilian consumption but a lot of this demand is on-farm and tricky to truly quantify

- The Brazilian harvest is continuing at a steady pace and exports remains supported

- Conilon shipments have been strong, keeping pressure on London spreads and flat price

- The Vietnam crop looks set to come in slightly under our estimate of 29m bag at 28 -28.5m bags

- We prefer using the options market for KC at the time of writing, as the traders may get hurt on the roll. See trading strategies section

- The roll yield for London remains intact and the managed money short suggests this could continue

Demand: The Current Climate

The global pandemic captivates financial markets, but the economic cost of the virus is still to be fully calculated. Equity indices have recovered 41% of the losses incurred in February and March as of July 2nd; fuelled by low-interest rates, and large liquidity packages from the Fed and other central banks, and the expectation of better economic data improving risk appetite. We expect this sentiment to continue as economies start to return to normal, but what will be the new normal and what of a second wave? In coffee, we have been focusing on what will be the impact on demand due to the lockdown and rises in unemployment. Throughout this report, we will outline how stimulus packages and savings ratios are impacting coffee consumption, and assess the price elasticity of demand for coffee.

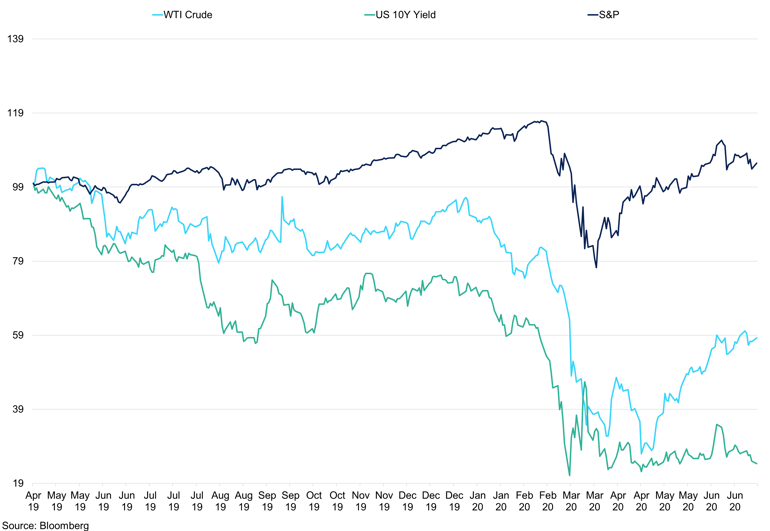

WTI Crude Vs U.S. 10yr Yield Vs S&P 500 Index (April 2019 = 100)

The recovery in the S&P 500 has been strong due to retail flows and liquidity measures from the Fed. Earnings capability in the next 12 months is weak, the S&P 500 and 10-year yield spread tells its own story.

When we draw similarities from the Great Financial Crisis to ‘The Great Lockdown’ for coffee demand, first we must assess the price elasticity of demand for coffee. From the beginning of October 2008 to end of September 2009 the price of the 2nd Month KC contract changed -5.45%. Using our consumption numbers, demand increased by 2.38% in the same period. Using the price elasticity of demand equation where the percentage change in quantity demanded ÷ percentage change in price (2.38%/-5.45%) you get -0.44 which is less than 1 and therefore inelastic. For the 2010/11 crop season when prices increased 24.92%, the price elasticity is 0.098, again inelastic. What this means is that the change in price has little impact on the consumption of that good. Does this mean that there will be little impact on demand due to the coronavirus? Not per se.

The US unemployment rate was at its peak for the GFC in October 2009 at 10%, the personal saving ratio as a percentage of disposable income was 6.2%, which was just off the year’s high of 8.2%. Before 2020, the savings percentage peaked at 12% in December 2012 but at the time of writing the U.S. savings percentage is 23%, after falling from 33% in April. An assumption that people’s expenditure, less mortgages and rent has fallen as restaurants, shops, and bars are shut and if Americans have been able to get a mortgage break this will also increase the savings percentage. However, while the savings percentage has increased, so has unemployment but surprisingly the figure fell in May to 13.3% from 14.7% the previous month, according to the Bureau of Labour Statistics. The percentage of unemployed, part-time, and marginally attached to work (those who are currently not working nor looking for work but indicated they have looked for work in the last 12-months), reached 21.2% in May 2020. The US average hourly earnings have fallen in the last couple of months, from 6.7% y/y in May to 5% in June. This represents lower-paid workers coming back to work after the initial redundancies, continuing jobless claims fell to 19.2m as of June 20th.

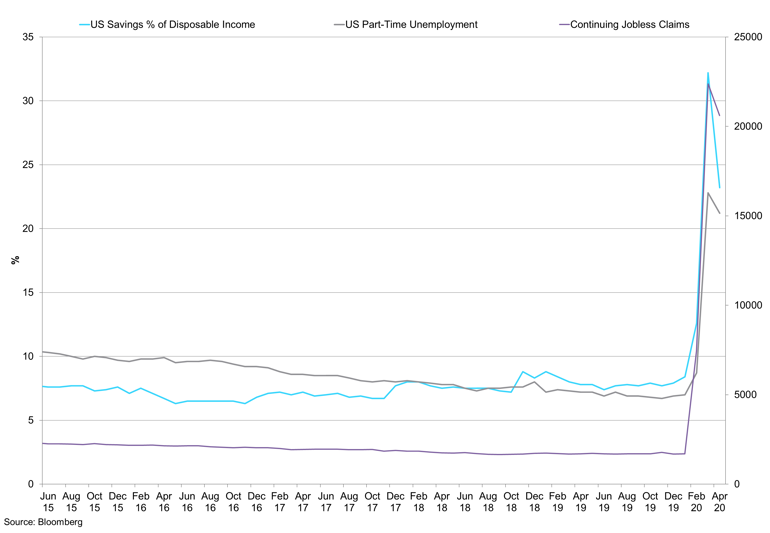

U.S. Savings % Vs U.S. Part-Time Unemployment % Vs Continuing Jobless Claims

The savings ratio has surged higher due to the uncertainty surrounding future employment and fixed costs such as mortgages.

The $2trn coronavirus rescue package passed by the Senate will be partially used to pay wages for some workers who remain on their payroll, but also included a retention fund for small businesses. In an attempt to help to prevent mass unemployment, however the unemployment level increased significantly in the last few months. According to the U.S. Labour Department data for the year-end 2019, the average person receives $378 a week in benefits. However, this is not truly reflective as Mississippi paid an average $213 a week, whereas Massachusetts pays $555 a week. The economic relief act on March 27th improves unemployment benefits by adding $600 a week to existing state benefits through to the end of July and states now pay half the average weekly payment, bringing Massachusetts and Mississippi to $878 and $707 a week. The relief bill allows benefits to be received for up to 39 weeks; there is also an investigation into fraudulent unemployment claims. We, therefore, have two categories, those workers who are lucky enough to be in full employment and receiving a normal salary who are saving as costs fall but also those who are now receiving benefits and are saving out of necessity. Another stimulus cheque from the government would help consumers but the rising cases and halting of states re-opening their economies is a concern.

In Europe, furlough schemes will improve the recovery of the economies once consumers have more certainty to spend. In Europe it is reported that more than 40m workers have been furloughed across the top 6 economies, an almost identical number to the U.S. We are also seeing unemployment rise in tandem with the furlough schemes, forecasts suggest that the EU 20 unemployment rate has increased to 9.25% as of July 2nd 2020. These workers remain at risk, and when the scheme finishes the unemployment rate may skyrocket with some estimates at 40%. The furlough scheme which is expected to cost European governments $110bn, between March and May has been incredibly beneficial but as companies have to start covering the cost, we expect redundancies to increase. While figures for the Q1 European savings rate are yet to be released, Q4 2019 saw the savings rate increase to 10.5% according to Eurostat. This would have increased in recent months.

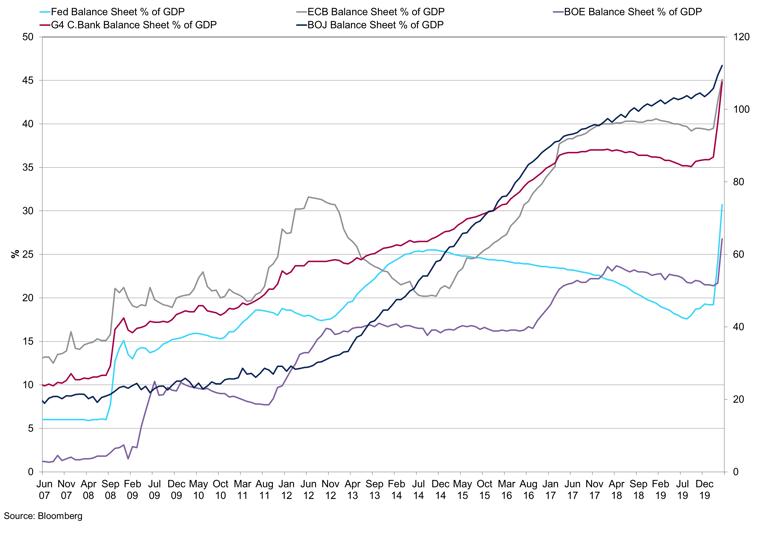

Central Bank Balance Sheet as a Percentage of GDP

Central Bank balance sheets have increased significantly as they fight the impacts of COVID-19. Further balance sheet escalation is likely.

The increase in savings percentage as well as unemployment is not enough to outline whether or not U.S. consumption will fall or rise, we needed to outline if coffee is seen as a luxury or normal good. The analysis above suggests that it is not a luxury purchase anymore and therefore demand is less responsive to a relative change in price. However, a survey in 2019 by the Fed indicated that approximately half of U.S. households do not have emergency savings; nearly 60% of respondents said they do not have funds or weren’t able to borrow from friends, family to cover 3 months of living costs. This outlines the downside risk to consumption but it is also too early to predict a significant drop off in consumption for this year as we do not know what the new normal will be and how many of those unemployed will find work again. Therefore, we believe coffee will still be consumed, but concede there will be exceptions to those who are pushed into poverty. U.S. personal income increased 10.5% in April as citizens received their stimulus package but spending fell 13.6%. The reduction in net spending epitomises the threat to out of home coffee consumption, but the question remains how much can consumption recover in H2 2020.

One thing we believe will change is that the type of coffee consumed, e.g. less expensive speciality coffee and more soluble/ filter coffee. This is where we think we could see a shift in consumption patterns, a move back to more traditional coffee and blends will use Brazil, Vietnam, and Colombian beans. While this could impact demand for speciality coffee, the market is not priced on these varieties - we know the markets are predominately priced on Brazil, Vietnam and Colombia. In our previous report, we outlined the difference between out of home and at-home consumption. This reinforces the outlook that the type of coffee consumed is paramount.

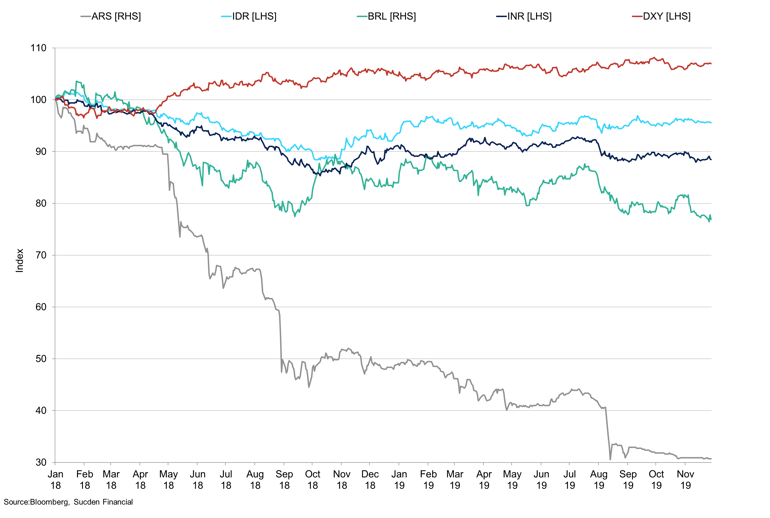

Emerging Market FX index (January 2018 =100)

Emerging market currencies have struggled in recent years against the dollar. However, dollar strength is starting to wane.

Theories of consumption loss in Brazil have merit; however, they may not be as drastic as reported. Disappearance in Brazil has always been hard to fully quantify due to farm consumption, uncertainty surrounding origin stock levels, and coffee often being given for free e.g. at petrol stations. It is important we do not let these factors take away from the fact the economic, social and health issues in Brazil are severe. It is for these reasons that we concede that coffee consumption in Brazil will suffer as more citizens fall into poverty, however, the ready availableness of coffee domestically may mean the loss of demand is not as drastic. There have been 41 impeachment filings against the incumbent Jair Bolsonaro, a large proportion of these requests came after Sergio Moro, a former ally was denounced. The threat of impeachment is prevalent, however, impeachment in the current climate is not conducive to the situation in Brazil and it seems challengers are waiting. According to a survey from Datafolha on May 25th 2020 on the evaluation of President Jair Bolsonaro, 43% of respondents said he was very bad; of that number 56% had a higher education, 65% students, and 48% live in the Northeast. 33% of the respondents said he was good/ very good, 56% of were entrepreneurs, and 42% earning more than ten times the minimum wage.

Brazil is being hit hard by the pandemic, and the economic stability is weak. Brazil’s attempts to join the Organisation for Economic Cooperation and Development are ongoing and have gained support from the U.S., the only country to support the membership thus far. Membership would be beneficial for Brazil but is a long way off; indeed the economic despair is prominent. Brazil’s economic Chief has suggested that there is an economic depression on the horizon, as the BCB cut interest rates to 2.25%. The legislation was recently passed to allow QE; however, we expect the BCB to exhaust previous tools before opting to start asset purchases or QE. The scale of the stimulus will be limited by the government deficit and we expect the economy to struggle for the remainder of 2020. Unemployment reached 12.60% as of June 18th, 2020, IPCA inflation y/y was 1.9% as of May 20th. Consumer confidence and industrial confidence continue to weaken at 71 and 78.4, respectively. The real recently benefited from risk appetite but remains just off historical lows, the prospect of a second wave in China and the U.S. has halted risk appetite.

Supply

Since our last report, we see little change to the supply outlook at this point. Indeed, Brazil’s harvest is on schedule but cold weather snaps have started early. There has been no damage at the moment and we continue to watch this in the coming weeks. At the time of writing, the Brazilian harvest is starting to slow, according to Cooxupe the harvest is 22.9% done vs 43.5% in 2019, there is a significant risk of delays which will likely have a negative impact on quality. With the chance of a disruption to the crop high and with inventories already falling may help support prices in the longer run, especially with an off-cycle on the horizon. The longer harvests will reduce coffee quality, and this impact will be felt when we move into the off-cycle and there isn’t higher quality coffee, especially if Central American crops are low in the coming years as outlined in our previous report.

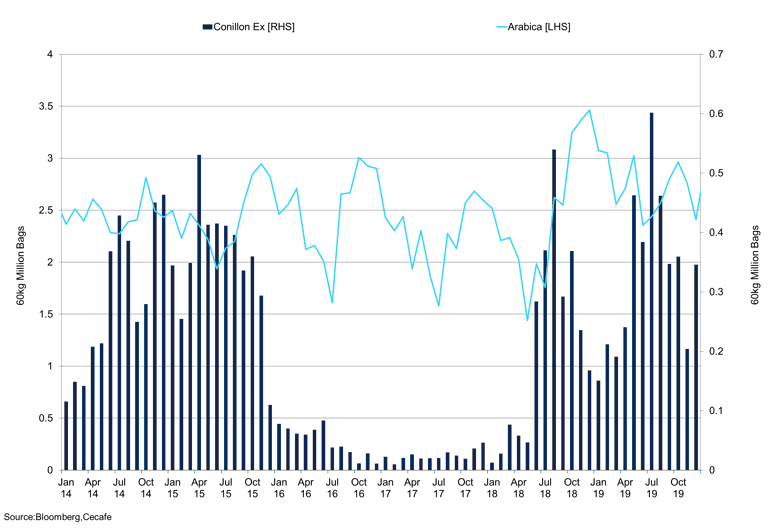

Brazilian Conilon and Arabica Exports

Conilon shipments have remained elevated in recent months despite COVID-19.

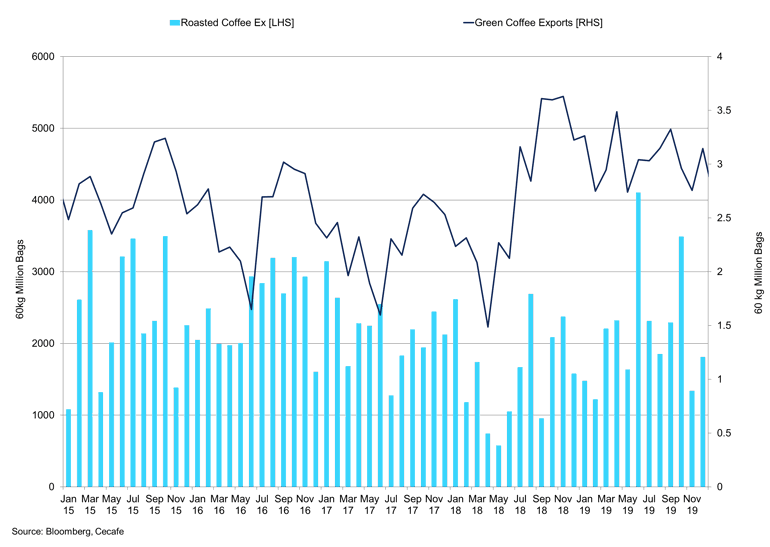

Brazil Green vs Roasted Coffee Export

Total shipments out of Brazil have been strong even with lockdowns in place.

In our previous report, we suggested there may be a tail off in Brazilian exports due to the virus, but we know now that at the time of writing this was not the case. Exports have stayed elevated, with total coffee exports in April at 3.3486m bags according to Cecafe. This involved 2.676m bags of Arabica, 313,145 bags of Conilon, and 1,752 of roasted coffee. These figures remained robust for May despite the threat of lockdown and COVID, total exports for May were 2.9788m bags. Conilon shipments were once again significant at 484,064m bags, arabica exports totalled 2.1987m. Total green coffee exports were 2.6828m, there remains some risk to June. We are hearing reports of requests for shipments to be delayed, but with differentials remaining firm this will come at a cost. Indeed, due to strong differentials, it is unlikely that participants will ship coffee unless you have a home for it. The harvest continues at a steady pace despite the pandemic, however further north in Colombia and Central America lockdowns have made it tricky for crop surveys to outline how coffee trees are fairing.

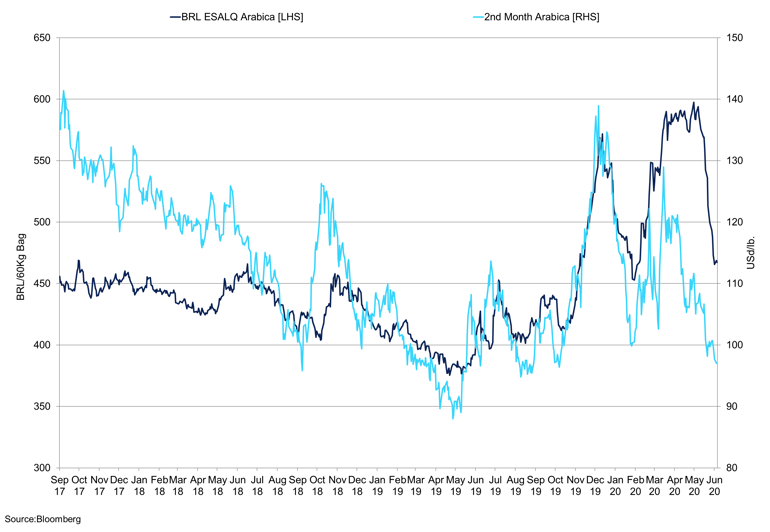

Local Brazil Coffee Prices vs 2nd Month Arabica

Local prices have fallen sharply in recent months and at current prices, we believe it is the speculators selling.

When prices moved back below 100cts/lb, the recent leg lower is speculative selling and we think the market is oversold at current levels. We do not envisage producer selling below 100cts/lb, the real has bounced off the lows but remains historically very weak. The recent rally has been USD weakness as opposed to BRL strength. A significant rally in the BRL is not in our base case for 2020; however, we expect producer selling to re-enter the market above 105cts/lb. Diffs remain firm and at current levels we may not see much demand, however, if these prices continue into the end of July will we see Robusta used?

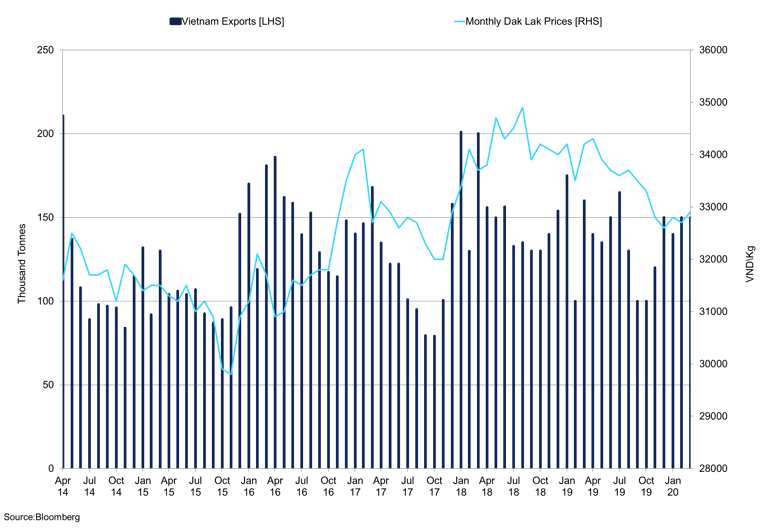

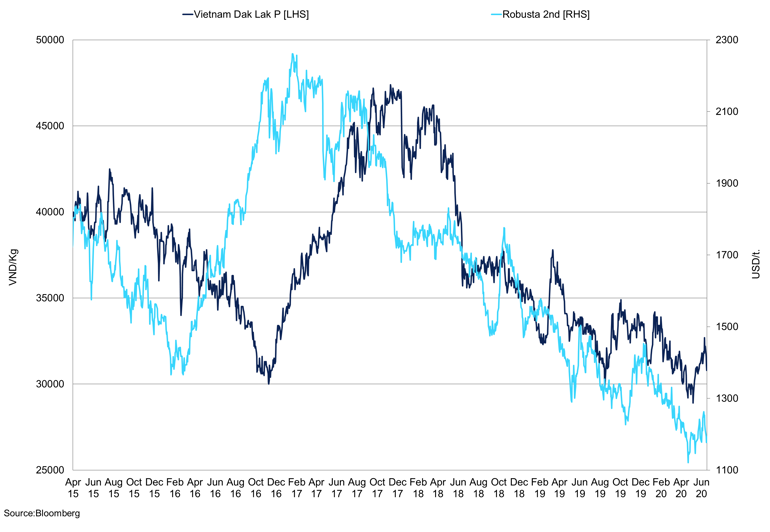

Vietnam Exports vs Monthly Dak Lak Prices

Local farmers hold out for higher prices with reports of the weaker crop.

We were concerned about dry weather in Vietnam; however, these fears have largely dissipated in recent weeks as soil moisture returns to favourable levels. There is some damage to the crop and there is some downside to our crop number of 29m bags, we could see this revised to 28m bags. However, exports from Vietnam have remained resilient so far this crop year down -2% from October to May at 18.5m bags, exports in May were 2.3m bags down 8.7% y/y according to the ICO. Differentials continue to offset low exchange prices and we expect that to remain the case.

Vietnam Dak Lak Robusta Prices vs 2nd Month Robusta

Rallies in the London contract have been sold affirming the recent trend.

Commitment of Traders

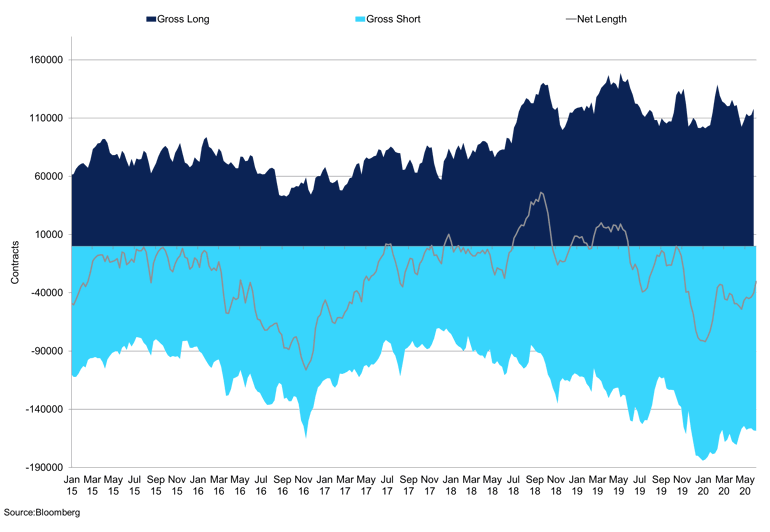

The Arabica Non-commercial net positions stand at -27,669 contracts as of July 2nd, we have seen open interest increase in recent sessions as prices sell off suggesting that we are seeing more shorts in the market. The open interest for futures and options combined has fallen from 346,000 contracts on June 12th to 321,408 as of July 2nd, significantly higher than 283,000 contracts on April 21st. We saw more shorts enter the market as we have seen specs sell the market below 100cts/lb, however, a short position now is a long-term trade. We could see the short-covering rally continue with covering orders placed above the market. While it does not seem there will be a significant rally in the immediate term, we believe the probability of a rally in Q3 is increasing, as we see clarity on the situation and move into the off-cycle we expect futures to rally strongly.

Arabica Producer Commitment of Traders

The net-short has decreased in recent months but remains short, we do not envisage producer selling at current prices.

The commercial COT was -22,938contracts as of July 2nd; we have seen a reduction in the net position in recent months. With prices at current levels and the real strengthening, we do not envisage producer selling at this level, especially as they have already sold a lot of coffee forward. The real strength is due to capital flows as well as USD weakness, as mentioned we do not envisage producer selling at current levels and prices would need prices to push back towards 110cts/lb in order to see more producer selling. Diffs have firmed which will reduce the demand for Brazils at current levels, volumes are limited.

For London, the managed money net positions have held constant in recent weeks and stood at -40,805 contracts (shorts) as of July 2nd. The roll yield and wideness of the spread is expected to keep the short intact, but the lower Vietnam crop, as well as a reversion back to traditional coffee blends in consumption, could prompt some tightness in the spread. We continue to look at the strong differentials and potential for a lower crop. However, this is more likely to plan out on the flat prices, as we are seeing strong Conilon shipments will keep the spread wide to help the carry trade. The producer/merchant/ processor COT net position stands at 34,794 as of July 2nd 2020.

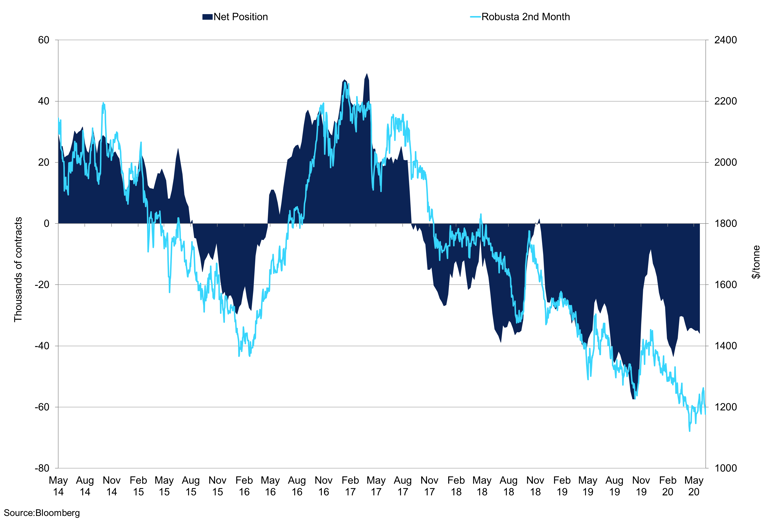

Robusta Managed Money Net Position vs 2nd Month Robusta

The Robusta managed money short position exerts heavy pressure on the market.

Inventories

We continue to see large withdrawals from exchange warehouses, most notably arabica. Since the beginning of March, inventories have fallen 22.6% to 1.6m bags. This suggests that consumption has not been as weak as suggested, and some roasters were caught with low inventory levels. In our opinion, inventories will continue to fall in the near term despite the strong shipments from Brazil. Looking ahead to the off-cycle, and continued troubles in Central America, we still maintain our view that inventories will fall to 900,000 bags this year: giving rise to prices in the long term. Indeed, any stocks held by roasters would have been drawn down in recent months and this may quicken the pace of withdrawals. Contra to ICE stocks, the GCA inventory levels increased to 6.818m, the majority of arabica stocks is in Europe. Robusta certs have also fallen incessantly since February to 11,650 lots as of July 2nd from 15,285 on February 12th, a decline of 23.7%. Conilon shipments have been strong but inventories continue to decline, if the Vietnam crop comes in under expectations we expect the decline to continue.

Trading Strategy

- We prefer using options in the current climate. September KC 130 calls, the premium is 0.88, for those wanting less time decay the Dec 130 calls are $2.85 with the 150 at $1.25

- A Dec call spread of 130 & 150 may be preferential

- If the recent price action has taught us anything, it is to get downside protection

- As we move into Q3, we would start building a futures position

- Despite the large Brazil crop on the horizon, we still anticipate the KC spread to tighten

- Robusta spreads are likely to remain wide as Conilon arrives in Europe. The managed money short is expected to stay elevated due to the roll yield

- On arabica spreads, the March 21-22 spread has started to tighten and we expect this to continue. We favour buying the spread as we envisage further tightness.