Electric Vehicle Trends

With the end of 2023 approaching, we look back at how the electric vehicle (EV) has performed amidst growing fears of the global economic recession. While downbeat economic forecasts have been postponed further to next year, investor sentiment dampened in 2023. Industrial production across the world declined, with manufacturing performance falling into contractionary territory for the first time since the beginning of the pandemic. However, the green energy sector remains the silver lining of the industrial performance. Despite internal combustion engine (ICE) vehicles dominating sales in major producing nations, electric vehicle sales continued to beat new highs. Automakers are betting on the longer-term trend, where combustion vehicles are completely phased out in the coming decades.

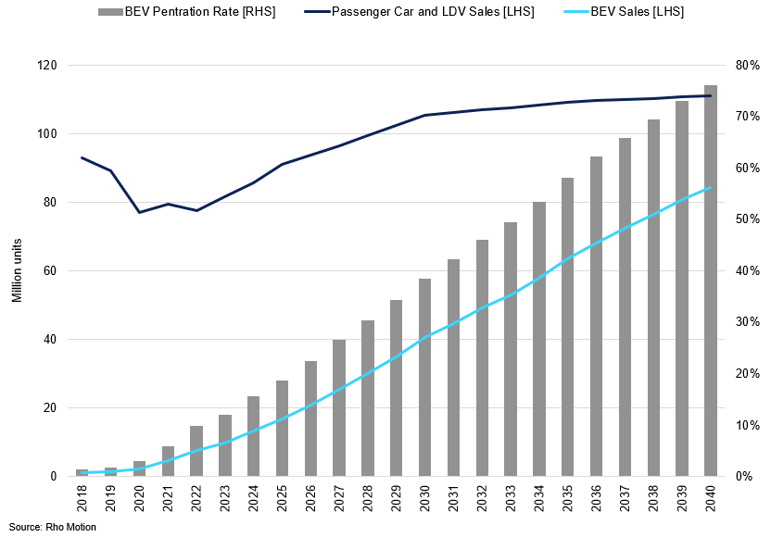

Global BEV Trends

The passenger and light-duty vehicle (LDV) sector is expected to grow marginally, with the peak seen around 2030.

Against this backdrop, EVs are on track to achieve over 13.8m sales worldwide this year, marking a notable 23% y/y increase. The industry also achieved a penetration rate of 12% – another record. China is driving this growth, with 55% of vehicles sold so far this year. The nation is firmly in the mass-market phase of adoption, with battery-powered vehicles making up more than 30% of passenger car sales in September. Europe has been surprisingly resilient, with sales in the region expected to increase by 20% this year to around 3.3m units, though subsidy cuts could still impact the final figure. While US sales are further behind, they have crossed the 1-million mark for the first time this year and are expected to grow by more than 40% from 2022 levels (Rho Motion). Despite the continued phase-out of subsidies in the US, the solid performance indicates that the nation is approaching a pivotal momentum in terms of EV sales. The global trend is set to continue in 2024, albeit at a slower pace, as continued price wars are diminishing profit margins, which is weighing heavily on original equipment manufacturers (OEMs) from EV segments. For example, Ford has further increased their expected profit loss in 2023 to $4.5bn, up from $3.0bn forecasted earlier this year. Looking ahead to the 2030s, we expect battery electric vehicles (BEVs) to constitute more than 50% of total cars sold. The outlook for EVs remains bright, and macroeconomic factors are unlikely to derail the longer-term trend.

Despite the continued phase-out of subsidies in the US, the solid performance indicates that the nation is approaching a pivotal momentum in terms of EV sales.

On the battery front, accompanied by a continued price decline across key minerals, real progress has been made in commercialising new chemistries, especially in solid-state and sodium-ion batteries. Lithium iron phosphate (LFP) batteries continue to gain market share, surpassing 40% globally for the first time. The biggest driver behind the uptake of LFPs has been China, constituting 60% of the total chemistry share, 15% in the US, and 5% in the EU. This trend is set to continue into next year. While nickel-manganese-cobalt (NMCs) are set to represent the majority of global sales into the end of this decade, continued research & development (R&D) into new battery chemistries is reshaping the landscape at an unprecedented pace.

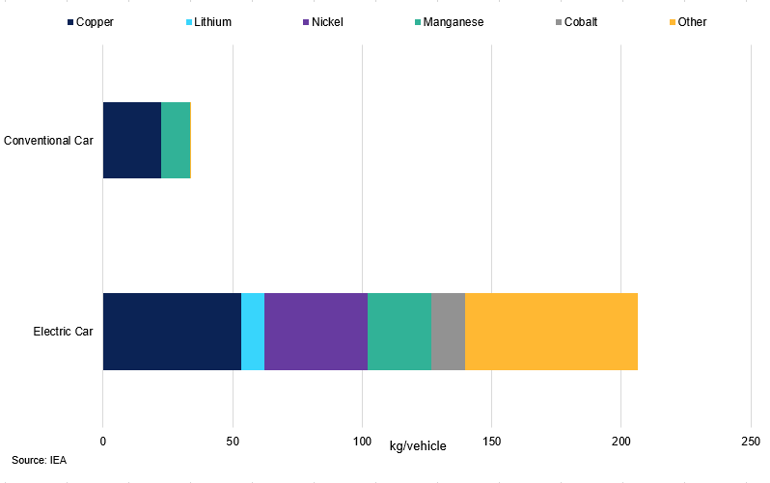

Metals Used in ICE vs EV (kg/vehicle)

Metal content is higher in EV models given the necessity of battery materials.

Given the rapid expansion of electric car sales, accessibility and sustainability issues surrounding mineral supply chains brought into question the ease of battery manufacturing. Electric cars are considered more environmentally friendly than traditional cars. However, the production of a 55kWh battery and its associated systems for a small EV requires over 200kg of metals, which is significantly higher than the 35kg required for a comparable ICE (IEA). This, coupled with the continued need to grow the battery pack sizes, creates a heavier environmental burden on mining and refining processes of the well-to-wheel (WTW) calculation of the greenhouse gas (GHG) impact of driving an EV. With the number of electric cars growing, the quantity of critical materials needed for EVs will also expand. Going into the latter half of this decade, deficits for a number of metals are growing, as the supply side is not enough to keep up with demand. Although new mines are coming online, both the timing and investment into new projects are extensive. For the mining of lithium, nickel and cobalt, which contribute around 60% of the overall battery, an investment of around $130bn per year over 2023-2025 is required, which would be directed to any mining project already in the permitting pipeline. As a result, new chemistries have emerged to substitute the need for “traditional” critical materials in hopes of phasing out metals such as cobalt and nickel in favour of more accessible materials. However, the energy density assumption of these chemistries is still being questioned. Accelerating innovation through advanced battery technology requiring smaller quantities of material could also take some of the load off the sourcing, which has been the case for cobalt. The interplay between technological advancements, material demand/supply, and environmental considerations continues to shape the landscape of EVs.

Regulations

In a world increasingly focused on mitigating climate change, the transition to green energy and electric vehicles (EVs) stands as a key strategy. This transition, however, unfolds against a backdrop of complex challenges, including fierce international competition for technology dominance, the quest for investment, and the pivotal role of critical mineral mining. The race to pioneer and excel in green technology has become an increasingly notable feature of global climate efforts. Nations and corporations vie for leadership in renewable energy, advanced battery systems, and EV production. In recent years, the global EV market has witnessed significant growth, with an anticipated sales figure in 2023 reaching nearly 14 million units. China has long held a dominant position in the green energy and EV sectors due to substantial investments that have enabled it to cultivate a world-leading industry. Western nations are intensifying their efforts to challenge this dominance, seeking to bolster their own industries. This competitive landscape extends beyond economic interests, encompassing strategic positioning in a carbon-constrained world. The transition to green energy and EVs relies heavily on the availability of critical minerals that are fundamental for battery manufacturing. The extraction and responsible sourcing of these minerals pose environmental and ethical dilemmas compounded by geopolitical complexities. Within this context, nations are taking strategic actions to strengthen their own EV industries, including the implementation of emission standards and industrial policies aimed at promoting the widespread adoption of cleaner transportation alternatives. International trade agreements play a pivotal role by facilitating access to critical minerals and fostering reliable supply chains for the essential components of green technology.

China has long held a dominant position in the green energy and EV sectors due to substantial investments that have enabled it to cultivate a world-leading industry.

United States

The Biden administration has placed significant emphasis on addressing climate change, making the reduction of greenhouse gas emissions (GMG) a central pillar of its environmental agenda. In 2021, the White House set a target for cutting GHG by 50% from 2005 levels by 2030 and committed to net zero emissions by 2050. Given that the transportation sector, primarily light-duty vehicles, accounts for 27% of total GHG emissions in the US, the administration's focus lies on encouraging the production and usage of EVs. The Inflation Reduction Act (IRA) adopted in August 2022 includes a comprehensive set of measures to catalyse the growth of the US EV market by offering incentives for businesses and individuals. In regard to the former, the legislation introduced a new tax credit of up to $40,000 for commercial clean vehicles that meet weight and battery capacity requirements. It also widened the scope of the tax credit for alternative refuelling property, enabling up to a 30% reduction in capital expenditures for charging units. The definition of qualifying property has been broadened to encompass bidirectional charging equipment and the charging infrastructure for 2- and 3-wheeled vehicles, encouraging the widespread deployment of charging stations. Moreover, the IRA extended for 10 years clean electricity production and investment tax credits whose shared goal is to promote the installation and operation of new clean energy sources. The extension also introduced direct pay, enabling tax-exempt entities, which collectively generate 15% of the entire US power supply, to take advantage of clean energy tax credits for the first time.

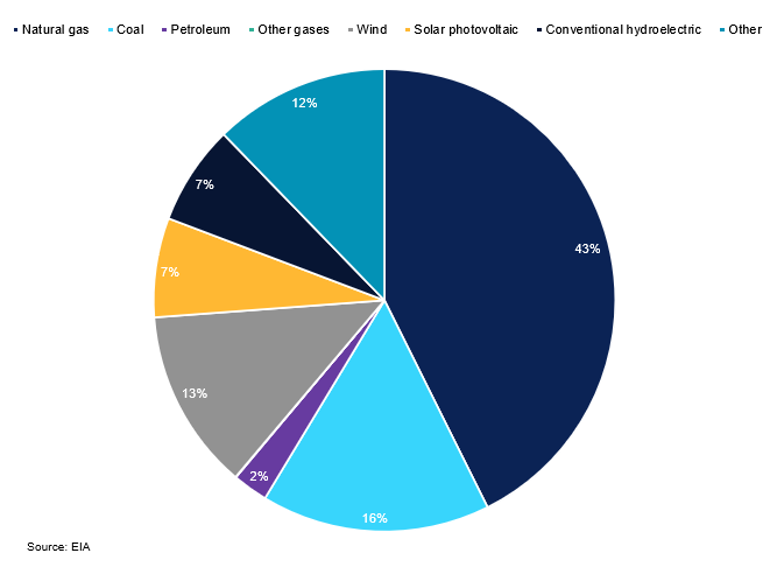

US Generating Capacity by Energy Source

Natural gas, coal, and petroleum remain the biggest source of energy in the US.

Concerning the consumer, the IRA replaced the longstanding EV tax credit with the Clean Vehicle Credit, offering tax credits of up to $7,500 for EV acquisitions. To ensure equitable access, this credit is subject to income limitations, with eligibility capped at a gross income of $300,000 for married taxpayers and $150,000 for single persons. Additionally, price caps were implemented to prevent excessive benefits for high-end vehicles, with a ceiling of $80,000 for Vans, SUVs, and pickups and $55,000 for other vehicle categories. Starting from April 2023, the IRA introduced additional Domestic Content requirements designed to prevent US industry’s dependence on non-allied countries for essential inputs. To qualify for the full $7,500 tax credit, EVs must go through final assembly in North America and meet two conditions related to critical minerals and battery components. Firstly, at least 40% of the critical minerals used in the EV’s battery must originate from the US or from countries that have a free trade agreement (FTA) with the US. The critical mineral quota will rise every year until it reaches 80% by 2027. Secondly, a minimum of 50% of the battery must be manufactured or assembled in the US or in FTA countries, with the content requirement rising to 100% in 2029. If only one criterion is met, the EV is eligible for a $3,500 tax credit. Additionally, any critical minerals or battery components from China, Russia, or other “foreign entities of concern” will disqualify a vehicle from eligibility, starting in 2024 for battery content and in 2025 for critical minerals. The policymakers anticipate that the additional conditions will incentivise automakers to relocate their supply chains toward the US and its allies. However, the EV sector has voiced concerns regarding the limited supply of minerals from countries with FTA with the US. Given that China has over half of the world’s lithium refining capacity, obtaining battery-grade lithium presents a significant challenge for battery producers. At the time of writing, only 11 meet the necessary criteria.

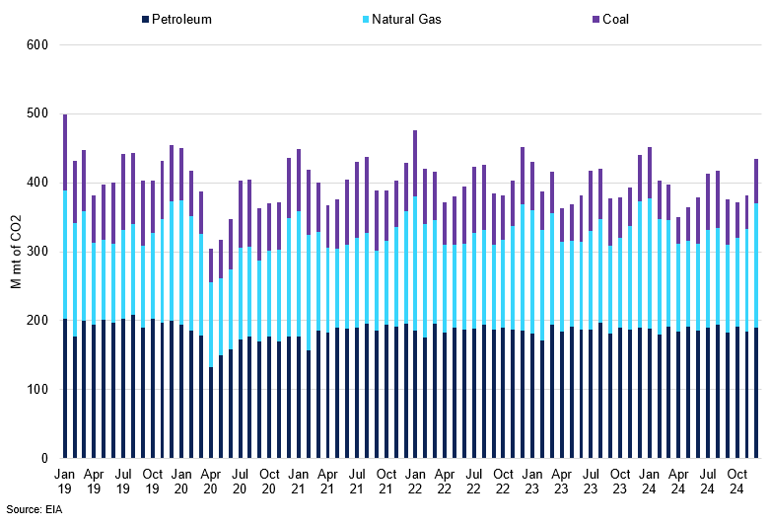

US Emissions per Energy Source

With these energy sources set to dominate energy capacity, emissions from the US should remain broadly unchanged.

Meanwhile, even if the cars do not meet the sourcing and manufacturing requirements, a legal loophole allows companies to claim tax credits by leasing vehicles to customers. Automakers and dealers can then pass on these credits to consumers through reduced monthly lease payments. This leasing option was initially intended to provide subsidies to operators of large fleets but is also applicable to private individuals leasing vehicles. Lessees can choose to use some or all of the tax credit to offset their lease costs or receive it directly. In December 2022, the US Treasury Department confirmed that buyers can effectively bypass the Domestic Content requirements for EVs when leasing. In 2023, EV leasing has lifted off disproportionately as many automakers introduced reduced lease prices, including for imported EVs and luxury models. In 2024, consumers choosing to buy eligible EVs will be able to transfer the credit to the dealer to lower the price of the car by the credit amount.

With more EV models becoming eligible for IRA tax credits, US EV sales are set to surpass 6 million by 2030.

Despite favourable conditions, such as a large automotive industry and a high GDP per capita, the U.S. has so far faced challenges in keeping pace with the electric mobility revolution sweeping across China and Europe. However, policy incentives implemented through IRA are expected to bolster higher adoption rates. According to S&P Global, the impacts of IRA have boosted the outlook for EV sales to more than double the pre-IRA forecast, with short-term sales already increasing. In Q3’23, BEV and PHEV sales increased for the thirteenth consecutive quarter, with the total number of EV sales growing to 313,086 units, making up 7.9% of total industry sales in that quarter. In the first nine months of 2023, EV sales reached 873,000 units, putting the market on track to surpass 1 million for the first time in history by the end of the year. The S&P Global predicts the US EV sales will ’each 1.3 million in 2023, marking a 52% increase YoY. With more EV models becoming eligible for IRA tax credits, US EV sales are set to surpass 6 million by 2030. However, challenges remain, including grid infrastructure upgrades and securing a stable supply of cost-effective lithium for EV batteries. Given the anticipated surge in EV sales, the electricity load is expected to increase, reaching 83 TWh by 2030. Upgrading the power grid will be essential to guarantee that the charging network can effectively support the anticipated sales growth.

Europe

Since the introduction of the European Green Deal (EGD) in 2019 – the world’s first public commitment to climate neutrality – the EU has stood as one of the global leaders of the green transformation. EGD set a plan covering all sectors of the economy to reduce EU net domestic production of greenhouse gas emissions by at least 55% by 2030 compared to 1990 levels and attain climate neutrality by 2050. To facilitate the transition to carbon neutrality, the EU proposed a “Fit for 55” package in 2021, containing a strategy to meet the 2030 interim target. With transportation contributing to around 25% of the EU’s GHG emissions, an important aspect of the strategy lies in the development of a more sustainable mobility system, including acceleration of the auto industry’s transition to EVs. The focus is placed on mandating manufacturers to progressively lower their average fleet emissions and ensuring that the necessary infrastructure is established to encourage the widespread adoption of EVs. In February 2023, the EU Parliament voted in favour of incorporating into European law the Fit for 55 goal of completely eliminating tailpipe CO2 emissions from new passenger cars and vans by 2035. In July, the Council of the EU adopted the Alternative Fuels Infrastructure Regulation (AFIR) to add more fast-charging stations and alternative fuel stations throughout the EU. According to the IEA, the total number of fast chargers in Europe increased by 55% YoY in 2022, exceeding 70,000. Still, the deployment of charging infrastructure remains uneven, with Germany, France, and the Netherlands together accounting for 69% of all charging points. Starting in 2025, the new regulation requires the installation of fast charging stations, each delivering a minimum of 150kW of power, at intervals of every 60 kilometres along the European Union's Trans-European Transport Network (TEN-T) system of highways, which serves as the primary transportation corridor for the bloc. In line with the law, charging stations should cover the complete TEN-T network by 2030, making EV travel through the EU more feasible.

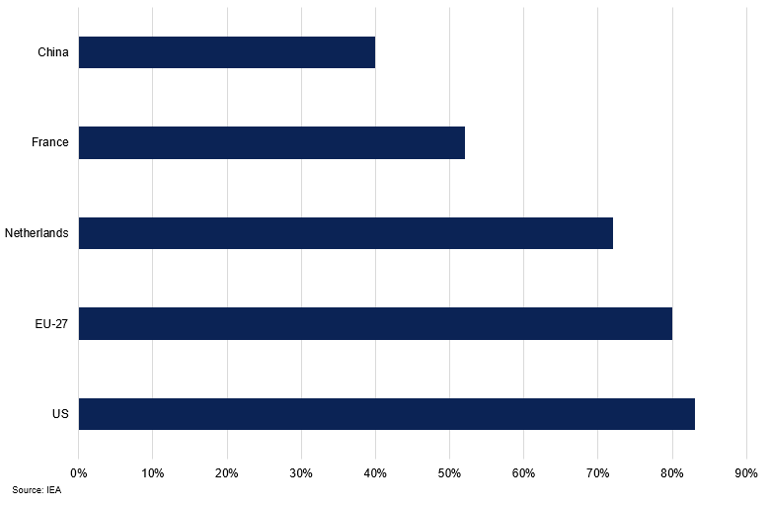

Share of Home Charging Points per Country

US and EU have the highest share of home charging points, easing off the peak-time energy load.

The EGD encompasses both environmental and economic dimensions, with a key focus on enhancing Europe’s competitive position in the net-zero industry. The adoption of IRA in the US has heightened concerns within the EU that manufacturers and adopters of clean technology may relocate their production to the US. While in the US, federal government subsidies are applied uniformly to domestic producers, regardless of their location, the subsidy landscape in the EU is characterised by variations among member states, relying on their fiscal capacities. Still, almost every EU country subsidises the purchase of electric vehicles. These incentives vary significantly in their nature and monetary value but collectively amounted to nearly €6 billion in 2022, with an average of approximately €6,000 per vehicle (Bruegel, 2023). Unlike the tax credits under the IRA, these subsidies do not discriminate between different producers. Despite the US being the EU’s largest trade and investment partner, there is no dedicated free trade agreement between the two. Since April, the EVs produced in Europe are no longer eligible for the US $7,500 Clean Vehicle Credit. Given that the credit lowers the cost of an average-priced eligible vehicle by around 20%, EU automotive manufacturers could face challenges in maintaining their previous market shares in the US. In response, the EU has introduced the Green Deal Industrial Plan, featuring the proposed Net-Zero Industry Act and Critical Raw Materials Act. These initiatives aim to bolster Europe’s net-zero technology manufacturing capacity, secure a sustainable supply of critical raw materials, and streamline permitting procedures for critical raw material projects. In March 2023, the EU and the US launched negotiations on a Critical Mineral Agreement to enable critical minerals extracted or processed in the EU to count toward certain EV tax credit requirements of the IRA, but at the time of writing, there is still no consensus or deal in place.

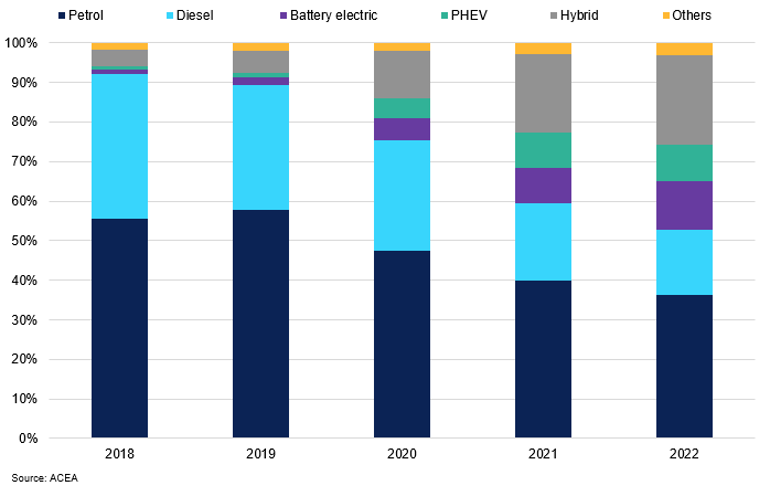

New EU Car Sales by Power Source

Petrol and diesel cars are being phased out in favour of electric cars.

Following a lacklustre 2022, the EU automotive sector experienced significant growth in 2023, driven primarily by increased EV sales. Over the first ten months of the year, new car registrations in the EU increased by 16.7%, reaching almost nine million units. During that period, EVs saw a 53,1% YoY increase, resulting in 1.2 million units sold and a 14% market share. At the same time, hybrid electric vehicles accounted for nearly 30% of all vehicles sold, as concerns regarding the availability of charging infrastructure continue to discourage consumers from going fully electric. Overall, electrified vehicles, including fully electric, plug-in hybrid, and full hybrid models, represented over 47% of new passenger car registrations in the EU from January to October 2023, up from 42% in the same period the previous year, according to the European Automobile Manufacturers Association (ACEA).

China

China's automotive industry has witnessed substantial growth in the last decade. In October 2021, the country became a net auto exporter for the first time, and since mid-2022, exports have continuously outperformed imports. By the first half of 2023, China surpassed Japan, emerging as the world's leading car exporter. Still, China's main focus lies on new energy vehicles (NEVs), a category encompassing fully electric cars, plug-in hybrids, and hydrogen fuel-cell vehicles. According to IEA, the country accounted for 35% of global EV exports in 2022, shipping mostly to Europe due to the region's high demand and substantial government subsidies for EVs regardless of origin. Internally, the annual sales of NEVs in 2022 surged from 1.3 million to 6.8 million, solidifying China's position as the world's largest EV market for the eighth consecutive year. The leader's position has been attained with comprehensive support from the government on both national and local levels. In 2014, the government implemented a 10% purchase tax exemption for both domestically manufactured NEVs and imported models. Initially set to expire in 2020, the purchase tax exemption has been extended a few times to bolster the market affected by the COVID-19 pandemic. In June 2023, the purchase tax reduction policy for NEVs was extended again for another 4 years, starting from January 2024. During this period, NEV buyers will be able to benefit from exemptions of up to 30,000 yuan ($4,170) per vehicle in 2024 and 2025, subsequently halved to 15,000 yuan for purchases in 2026 and 2027. On the local level, more than 50 cities and regions in 2022 implemented a range of incentives designed to stimulate the demand for EVs, including cash subsidies, free parking spaces and consumer vouchers. Local authorities also play an important role in encouraging R&D. In January 2023, Hunan province announced its plan to offer a subsidy of 5 million yuan for the development of a new passenger vehicle model and promised to provide a maximum of 50 million yuan to automakers, establishing an R&D centre within the province.

Despite a less-than-stellar economic performance this year, the government incentives at both the national and local levels continue to effectively encourage the adoption of EVs.

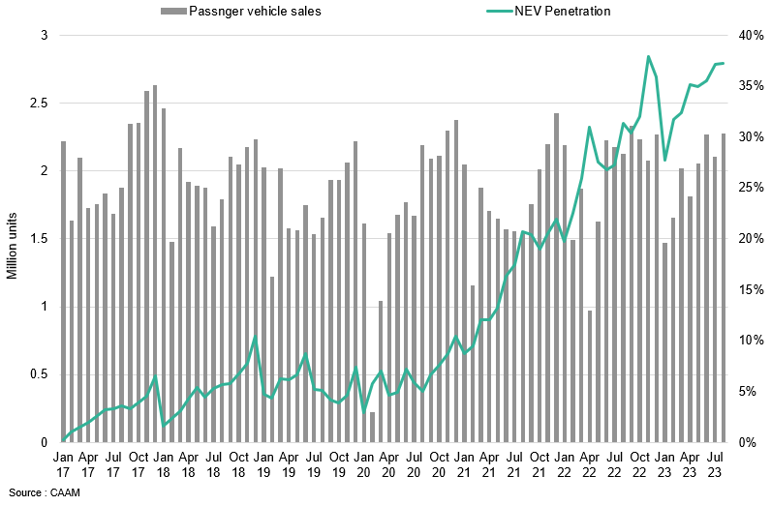

China Passenger Vehicle Sales vs EV penetration

EV penetration continues to grow rapidly in China, thank to stellar production and sale figures from the electric segment.

According to the China Association of Automobile Manufacturers (CAAM), China’s NEV sales reached a new record in September, amounting to 904,000 units, making up 31.6% of total sales. From January to September, China’s NEV sales surged by 37.5% YoY, totalling 6,278,000 units. The global EV leader is expected to surpass 8 million units in 2023 with the largest producer – BYD – planning to hit the target of 3 million NEV sales. Despite a less-than-stellar economic performance this year, the government incentives at both the national and local levels continue to effectively encourage the adoption of EVs.

Nickel

From 2017 to 2022, demand from the energy sector was the main factor behind a 40% rise in demand for nickel, with its share jumping from 6% to 16% in 2022. This trend is expected to continue, leading to a significant increase in exploration spending for nickel, which rose by 45% in 2021. Canada is leading the way in this regard, where high-grade sulphide resources, proximity to existing infrastructure and access to low-emission electricity create attractive investment opportunities. Despite the introduction of LFP battery chemistries into the global mix, NMCs remain the dominant chemistry at 55% until the end of the decade, and nickel is an integral part of lithium-ion batteries to improve energy density (IEA). Moreover, with the majority of global LFP production concentrated in China, economies such as Europe and the US should continue to rely on nickel and cobalt for most of the battery manufacturing. With stellar growth of EVs across the world, we expect global nickel demand to almost double from 2021 to 2030, requiring more than 2.0Mt of additional material. While 50% of demand still comes from stainless steel, 27% will come from EVs, and this percentage is expected growing at a rapid pace, while demand from stainless steel is diminishing.

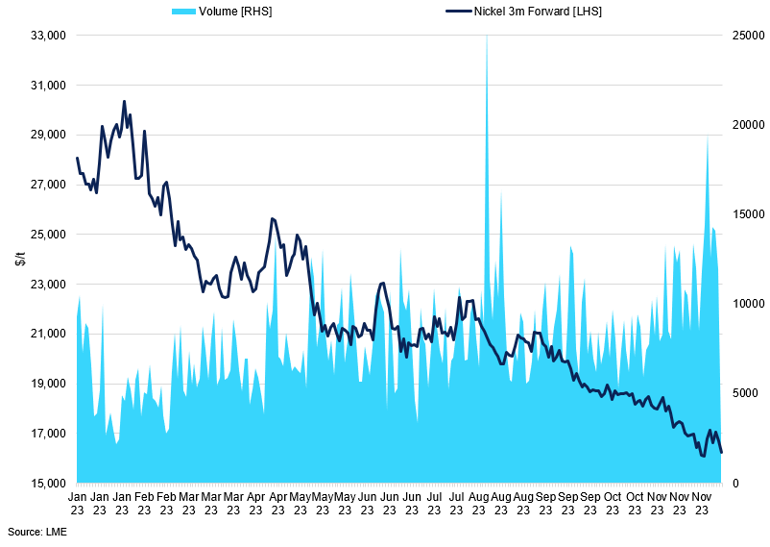

Nickel Prices vs Volumes

Volumes for nickel forwards have picked up in recent months, as prices continued to decline.

Going into the latter half of this decade, the demand for Class 1 nickel is expected to exceed the supply, leading to a deficit. This will result in a further depletion of inventories. On the other hand, Class 2 nickel is expected to be oversupplied marginally in 2030. Indonesia is expected to contribute around 500kt of nickel by 2025, which accounts for 40% of the total production. However, this is still not enough to offset near-1Mt of global Class 1 nickel shortages that is anticipated by 2030. While Indonesia is set to increase reserves, other regions lack sufficient reserves to ensure a stable supply stream. A search for new nickel sulphide deposits has been in progress for years now, particularly in Australia and Canada. Laterite focus has been mostly in Southeast Asia. However, projects in these regions are less feasible over the long term, and the share of Indonesian production is set to grow further.

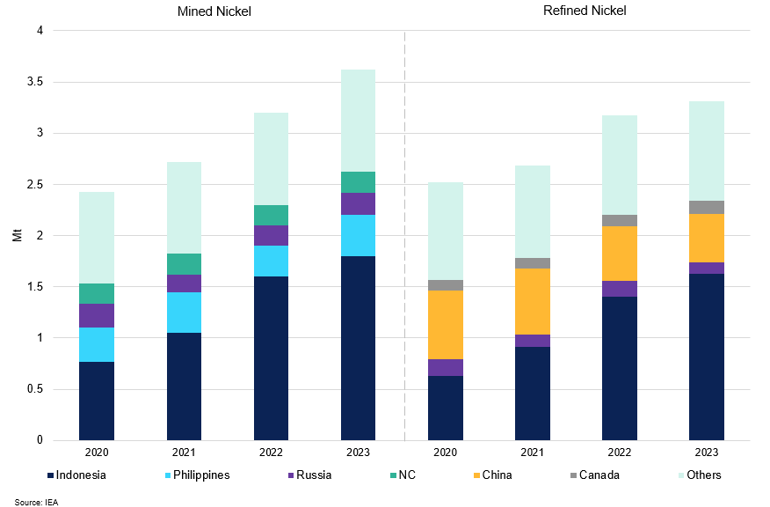

Mined and Refined Nickel Geographical Concentration

Indonesia is leading the way with both mined and refined sources of nickel.

Increased geopolitical concentration is driven by the growing risk of underinvestment in clean energy and supply bottlenecks in emerging economies. One hurdle to investment in those countries is their higher cost of capital, which has a significant impact on the financial viability of clean energy projects. As described in our previous report, the higher the risk is with the associated project, the higher the discount rate will be, reducing the future value of cash flows for the project. Financing costs for material production projects can be twice as high in emerging economies due to a greater perception of risk. Therefore, the discount rate will be even higher, making foreign investment less attractive and therefore, distribution is likely to remain concentrated.

...the higher the risk is with the associated project, the higher the discount rate will be, reducing the future value of cash flows for the project.

Therefore, maintaining adequate stockpiles of vital materials and components is essential for companies to handle any temporary disruptions or dislocations in supply. For example, nickel consumption fluctuates largely year-on-year, and maintaining a healthy stockpile level is essential in establishing a smooth supply chain. As of November 2023, LME stockpile levels are at 46,338mt, and while improving month-on-month, it remains near the 2007 low, suggesting that any massive disruption to demand could cause a sharp increase in prices. Despite stellar EV growth this year, overall demand for nickel, in particular, in construction, has been lacklustre, exemplified by the cash to 3-month spread at -$223.50/t – a multi-year low. The nickel market is currently oversupplied with ferronickel and nickel-pig-iron (NPI), most of which are coming from China. Further imports from Indonesia will add to the 400kt surplus in 2023. This, coupled with weak stainless steel demand in the region, should weigh on nickel prices in 2024. We believe that the current EV trend is more likely to solidify support levels than push prices higher over the short term.

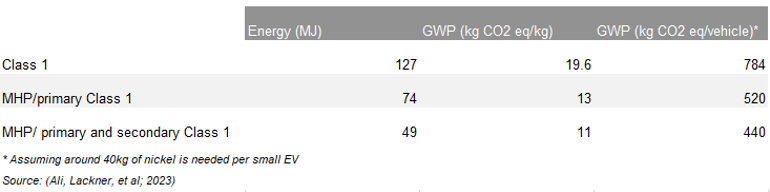

Nickel Sulphate Production from Different Materials and Their Respective Energy Consumption and CO2 Emissions

There have been efforts to address the shortage of Class 1 nickel supply by using technologies like the high-pressure acid leach (HPAL) method, which convert Class 2 into Class 1. However, this process has a higher carbon footprint than traditional Class 1 sources. Western automakers, who are subject to more stringent regulations, are unlikely to prefer this method. Nickel sulphate, which is an important feedstock in the production of lithium-ion cathodes, can be manufactured from Class 1 and other intermediates like nickel matte, mixed hydroxide products (MHP), mixed-sulphide-precipitate, crude nickel sulphate and the rest is from secondary nickel sources such as from recycling of nickel. This should help reduce the environmental burden on battery-grade nickel production, especially as nickel sulphate demand is expected to increase to more than 1000kt in 2030, up from 200kt in 2022. Different studies show that nickel energy usage during the production stages varies, but the majority agree that electricity usage accounts for 52%, followed by natural gas at 40%. Taking this into consideration, the table below shows that the least energy-intensive and carbon-emitting option is seen in the combination of MHP and primary/secondary use of Class 1, at 440kg of CO2 eq./kg of nickel sulphate (Ali, Lackner, et al. 2023). The biggest tailwind to a more balanced market is seen through the continued growth of LFPs, which are expected to lift some of the pressures of the nickel market over the longer term.

Cobalt

Despite efforts to reduce the use of cobalt in battery chemistry, demand for this mineral remains one of the highest among critical minerals, witnessing a 70% jump from 2017 to 2022; the share of clean energy applications reached 40%. This trend is set to continue, with overall demand for the mineral set to grow 3-fold, and demand from the EV battery sector is set to expand 5-fold, making up 52% of overall global growth by 2030, according to the IEA. That is faster than copper and nickel, only behind lithium in comparison. Other industries such as aerospace and defence, catalysts, magnets, electronics, etc, also contribute to cobalt demand, adding stronger upside to our demand forecasts. Although cobalt is much more energy- and carbon-intensive than other materials, much smaller amounts are usually needed to make specific products. For example, an average EV typically requires around 7kg of cobalt compared with 920kg of steel and 220kg of aluminium. Still, according to research by Qing Shi, cobalt demand in China, which represents 70% of total refined demand, is set to peak around the late-2020s at 30-65k mt across the baseline scenario as high-cobalt chemistries are phased out. A decline in market share of lithium-ion batteries by 10% should result in a 14.3% decline in cobalt demand, suggesting a near-proportional impact from EVs on cobalt. While cobalt substitution can reduce the demand substantially, it cannot completely phase-out demand driven by the increasing EV sales and battery capacity.

Cobalt Demand from EVs vs Total Supply

Given the EV segment, cobalt market should remain balanced. However, given the prevalence of other demand sectors, cobalt could be in a sharp deficit by the end of the decade.

Most of the cobalt produced worldwide is a by-product of either nickel or copper mining. Cobalt production is thus incentivised by firmer nickel or copper prices rather than on its own price cycle. In recent years, cobalt prices on the LME have closely followed nickel, falling by 35% in 2023 vs 47% for nickel. The Democratic Republic of the Congo (DRC) produces 71% of cobalt today. However, Indonesia made significant progress, becoming the second-largest supplier of mined cobalt, tripling its cobalt production to 187kt in 2022, with the commencement of new HPAL projects, according to the Cobalt Institute. The US has also begun its first cobalt production since 1994, with the start of production at the Idaho Cobalt Operations in October 2022. However, due to a lack of domestic processing capabilities, these ores are to be exported. With a strong pipeline of projects in the DRC and Indonesia, and with restrained price conditions, the dominance of these two countries in global cobalt supplies is expected to continue, while China maintains its stronghold in refined product supplies.

With a strong pipeline of projects in the DRC and Indonesia, and with restrained price conditions, the dominance of these two countries in global cobalt supplies is expected to continue.

Despite high geographic concentration, we do not expect to anticipate a significant shortage of supply until the end of this decade. Indeed, cobalt has one of the lowest supply gaps among critical minerals, at only 10%, thanks to innovations in battery chemistry that have reduced its content. This illustrates of how innovation can help reduce mineral demand in the face of rising costs and concerns about environmental, social and governance (ESG) considerations. Additionally, we do not see any concerns regarding longer-term output prospects, as lithium and copper require 70 and 80 mines, respectively, to meet the needs of demand in a given year, while only 30 mines are needed for cobalt, most of which are incorporated into the nickel/copper supply stream. Therefore, while the share of cobalt in battery chemistries may decrease, given its high-density properties, the phase-out is not expected in the near future. As a result, supply is likely to closely follow demand, and we anticipate marginal deficits until 2030. For 2023 and 2024, oversupply is more likely, and we expect to see further softness in cobalt prices. Alongside the DRC, Indonesia is set to add more volumes as the country produces cobalt as a by-product of its growing nickel industry.

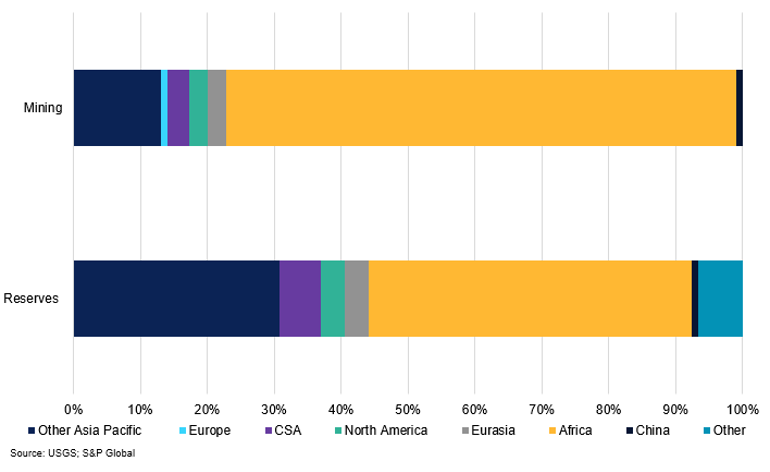

Global Reserves and Mining of Cobalt

The DRC continues to dominate the cobalt market, although the rising share of reserves in Other Asia pacific could help diversify the sources of the metal.

As investment in the battery metals sector continues to grow, trading liquidity has notably improved since 2022. Unlike base metals, cobalt has traditionally been traded based on bilateral multiyear contracts, with limited activity on major exchanges. This highlights the growing importance of spot pricing and the potential emergence of financial instruments to hedge price risks. However, the trading liquidity of battery metals still lags significantly behind that of other bulk materials despite recent improvements. Currently, daily traded volume as a percentage of annual production represents less than 1% for cobalt, compared with 10-30% for major materials such as nickel, zinc, and copper. This underscores the significant potential to increase market liquidity as well as the need to enhance market transparency as the sector continues to grow.

Lithium

In just a decade, the lithium industry has undergone a drastic transformation, with batteries now being the dominant use of the material. Historically, the majority of lithium mining capacity has been concentrated in Chile's salt flats and Australia's hard rock spodumene ore mines, both accounting for 30% and 46% of global mine production, respectively. China dominates the downstream refining process, contributing more than half to a 33% y/y growth in chemical supply in 2023. However, lithium has one of the highest geographical concentrations globally, creating further hurdles for the ease of supply chain diversification. As we have seen so far this year, prices weakened substantially, falling by 75% YTD, due to destocking across the battery supply chain in Chinese markets, which lowered apparent demand for lithium. With just three countries responsible for 90% of global lithium production, supply shocks and uncertainty surrounding mining project additions will continue to add severe volatility to lithium prices.

Many resource-holding nations are seeking to move further up the value chain, while consuming countries want to diversify their source of refined metal supplies. As a result, lithium is attracting substantial attention from mining investors. The capital sector for critical minerals startups improved, reaching $1.6bn in 2022. Lithium also emerged as the clear leader in the growth of exploration activities, with spending increasing by 90% in 2022, following a 25% increase in 2021. Canada and Australia led the way with over 40% growth, notably in hard-rock lithium plays. Tianqi and Albemarle, two major lithium ore miners in Australia, have both invested in refining plants. In 2022, Tianqi launched Australia's first battery-grade lithium hydroxide plant at Kwinana, with capacity expected to grow from 24kt to 100kt per year. Albemarle is commissioning a similar-size plant at Kamerton at 50kt per year.

Many resource-holding nations are seeking to move further up the value chain, while consuming countries want to diversify their source of refined metal supplies. As a result, lithium is attracting substantial attention from mining investors.

There has also been progress in China in extracting ore domestically through lepidolite mining. Yichun has been at the centre of the nation's lithium mining boom, aiming to bring about 350k mt of LCE by 2025. However, significant hurdles remain to support the meaningful growth of this process. These include a higher cost profile compared with other lithium sources and the substantial amount of waste associated with their development. Indeed, black mass refining undercapacity in China is set to expand further into 2030 at 5Mt, further burdening potential smelting projects. The projects are also vulnerable to the recent fall in lithium prices. While new lithium mines and mining exploration projects are coming online, we anticipate these projects to be minor to fill the supply gap by 2030. From exploration to construction alone, a mining project requires, on average, 3-5 years. This highlights that while new projects are likely to extend the timeline, they are not going to avert the widening deficit by the end of the decade.

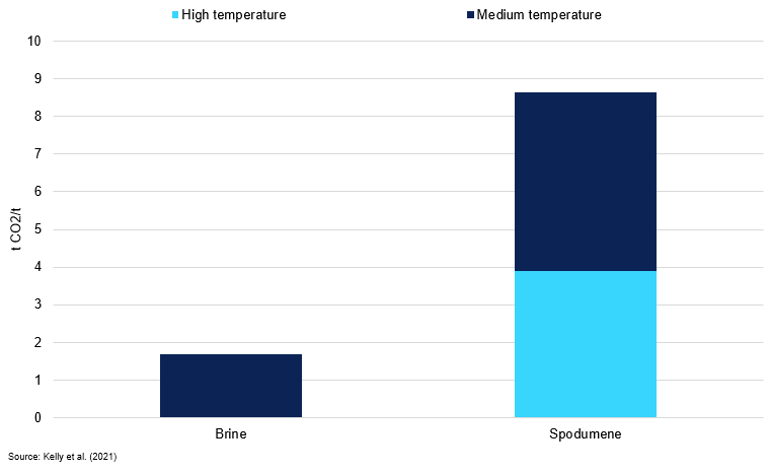

As the world shifts towards green energy with the use of EVs, the extraction of lithium has to improve as well to ensure that well-to-life (WTL) emissions remain in line with global environmental standards. Extraction via spodumene is far more energy- and carbon-intensive, given the heating steps that use coal to power the high-temperature kilns and steam production. While the brine method uses a lot of chemicals with their own indirect emissions, the whole process is five times less carbon-intensive than extraction from spodumene. There are ongoing efforts to develop cost-effective technologies to decarbonize these production routes. It may be possible to replace fossil fuels with renewable electricity or low-emission hydrogen or use carbon capture in this process, but little research exists so far. For example, electrodialysis enables the extraction of high-purity lithium hydroxide directly from brine, requiring only electricity. However, this technology is still at the laboratory scale (Grageda et al., 2020; Zavahir et al., 2021). One of the most ambitious projects is being led by Vulcan Energy in Germany. Their geothermal plant will produce electricity for sale to the grid and use the heat derived from extracting lithium from the geothermal brine (Vulcan, 2022).

Lithium Hydroxide Emission Intensity per Production Route Using Heat

Refining through brine is five times less carbon-intensive than production from spodumene.

Another complicating factor in assessing future lithium supply and demand is that the market comprises two different key products: lithium carbonate and lithium hydroxide. The former is mainly used in LFPs, which have been widely used in batteries in the Chinese market and are now making inroads in other regions. On the other hand, lithium hydroxide is driven by high nickel cathode chemistries, which are increasingly favoured by the premium EV market due to their higher energy density. This has important implications for the pricing of the two different compounds. The discount rate for lithium could, therefore, be higher in the near term to favour material extraction in the short term to maximise profit, but there is a greater risk due to the new entrants into the market; this increases the risk to the project. We expect prices for battery-grade materials to remain elevated due to robust expectations for demand growth, the challenges associated with producing and qualifying as a battery-grade product, and the higher cost profile of non-brine plays.

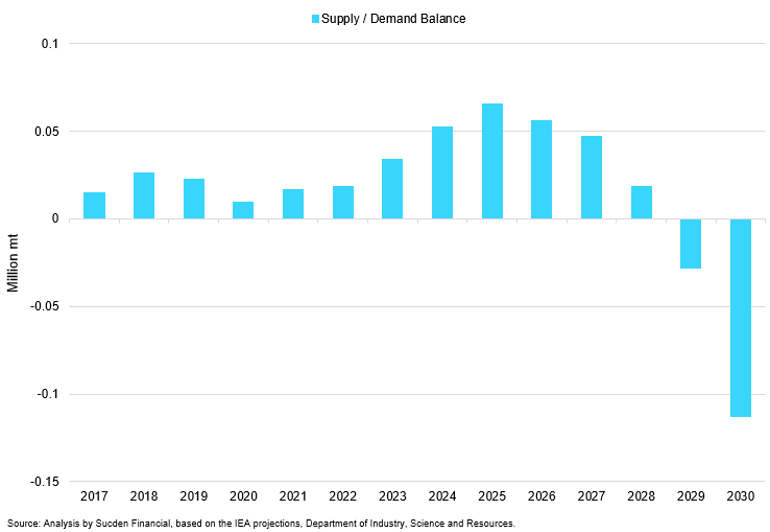

Lithium Supply & Demand Balance

The case for a lithium deficit is expected to expand by the end of this decade, as EV demand expands rapidly.

Still, the lithium market is currently experiencing a period of rapid expansion, with demand set to grow 3.5-fold from 41,300mt in 2017 to 144,700mt in 2022. Production levels are also increasing at a significant pace, with 2023 set to post 30% y/y growth to above 178,500mt. As a result, we expect another year of surplus, exceeding 33,000mt in 2023. Supply growth for 2024 is set to expand rapidly once again, growing by 26% y/y. This should expand the surplus further to 52,600mt, weighing on lithium prices next year. Severe lithium price corrections this year have removed sizeable downside risk, but the upside remains limited over the medium term. In our high-case scenario, we see further upside to the demand outlook, given a more rapid acceleration of EV adoption globally. Should this view materialise, the market would remain pretty balanced until 2025, with a marginal surplus still present. Still, the gap between supply and demand is set to expand in the latter half of the 2020s, reaching 35% by 2030, led in large by rapidly expanding Chinese demand. By 2030, lithium demand is set to grow 7-fold to 415kt, and more than 80% of that growth is due to electric vehicle demand, which is set to expand consistently over the coming decades. That is in comparison to a 1.6x increase for copper, 2.0x for nickel, and 2.8x for cobalt. This implies that unless new expansion projects in processing as well as mining are launched soon, the required expansion of EV fleets worldwide to remain on track for net zero by 2050 will be severely hindered.

Critical Mineral Demand Outlook

NMCs have been the preferred choice for automakers, representing 50% of total battery sales, due to their high-density properties that allow for longer driving ranges. However, a sharp price increase across lithium, nickel, and cobalt in 2021-2022 led to the first-ever increase in battery pack prices. In 2017, battery packs accounted for only 5% of the total vehicle cost, but this has now risen to 20%. As a result, automakers have started to move away from materials such as nickel and cobalt in hopes of reducing costs but also ensuring supply chain accessibility over the longer term. At the same time, the affordable and safe but less energy-dense lithium-iron-phosphate (LFP) chemistry has been making a comeback and steadily increasing its market share. This is due to strong support from local and global automakers in China, leading to renewed interest in the chemistry from automakers in the West as well.

Both the NMC and LFP developments are closely linked to the critical minerals that are needed for battery production. While reducing cobalt content has been prevalent over the recent years for companies aiming to reduce costs and mitigate social risks for battery manufacturing, the rise of LFP is triggered by the fact that this variant uses just one key critical battery mineral, namely lithium, reducing concerns around critical mineral supplies.

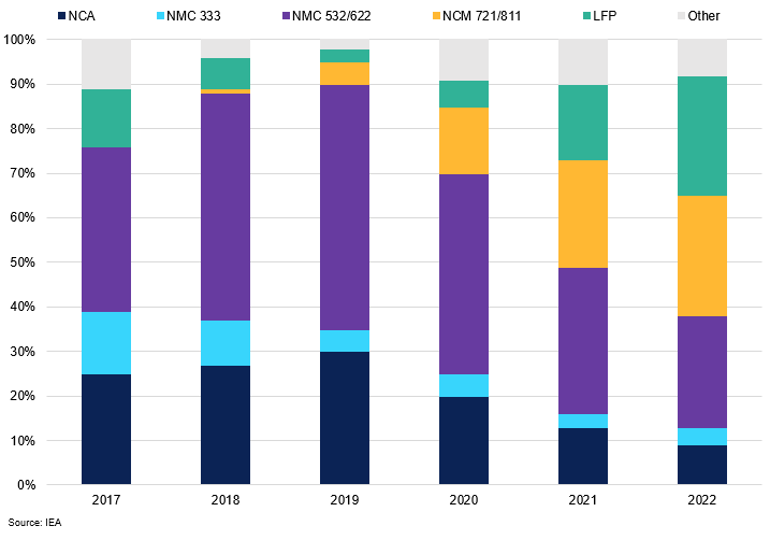

Evolution of Sale Shares by Cathode Chemistry

High nickel and cobalt chemistries are phased out in favour of LFPs.

While NMCs should continue to dominate the market in the coming years, holding a steady 50% share until 2040, the growth of LFPs is exceptional, with its share peaking at 43.7% in 2024. Still, in absolute numbers, the production of both chemistries is set to grow rapidly, given the continued expansion of EV sales, putting additional pressure on critical minerals. According to our calculations, nickel demand in passenger BEVs globally will remain the largest among the materials needed for cathode production. From NMC811 demand alone, nickel demand is set to expand to 1.76M mt by 2030. This demand is greater for NCAs; however, with diminishing demand for this chemistry, we expect its impact on nickel demand to fade. While 50% of demand is still seen in stainless steel, 27% will come from EVs, and this percentage is seen growing at a rapid pace, while demand for nickel from stainless steel is seen diminishing. Moreover, EV demand is set to be the key driver behind nickel consumption growth this decade.

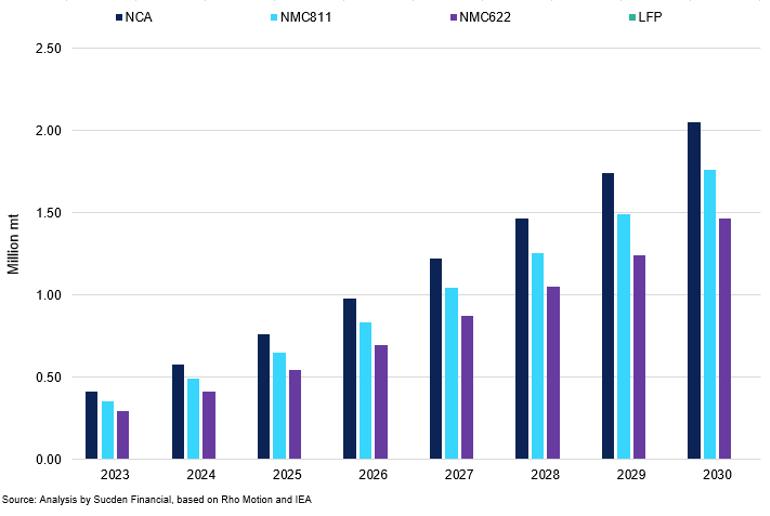

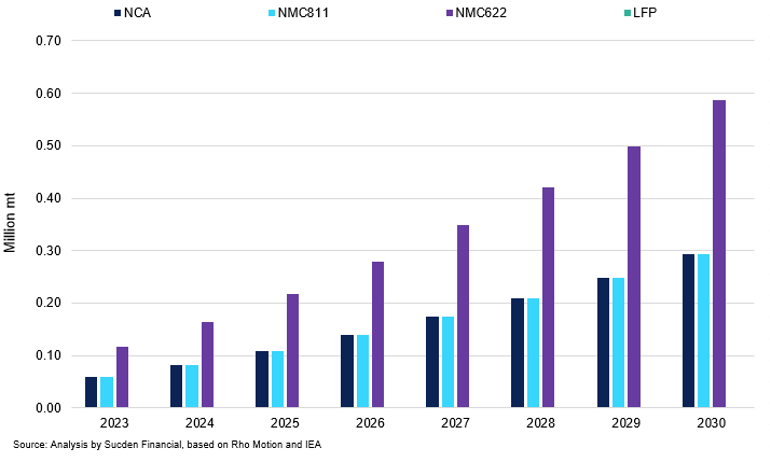

Nickel Demand Outlook by Battery Chemistry Segment

With NCA battery chemistries being phased out rapidly, nickel demand is expected to reach around 1.5M mt by 2030.

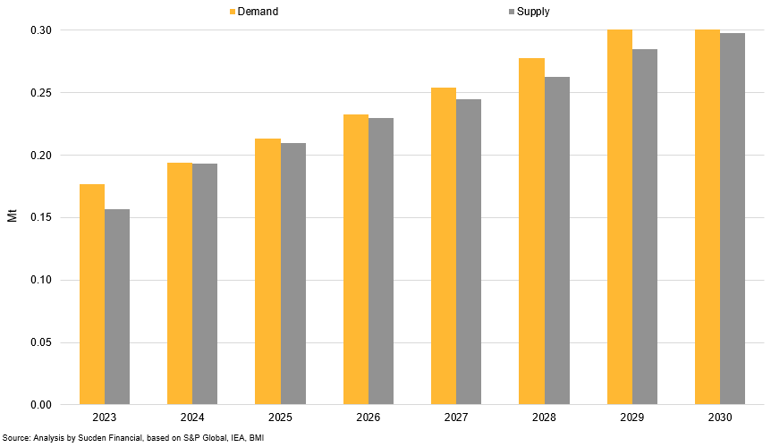

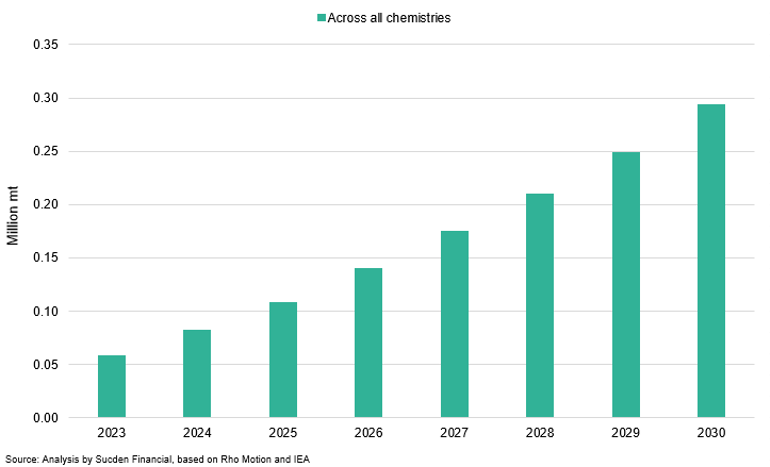

Cobalt’s share is expected to fade away with a growing share of low-cobalt chemistries such as NMC721 and NMC811, as well as LFPs that do not use any cobalt in its composition, resulting in just under 0.6M mt in cobalt demand by 2030. With the diminishing share of NMC622 in global chemistry use, our nickel demand forecast is leaning towards 0.3 Mt for 2030. Supply is anticipated to be slightly above this level at 0.31M, creating a balanced market for EVs. As a result, the supply gap is one of the lowest of all critical minerals at 10%, thanks to innovations in battery chemistry over the last five years that have reduced the cobalt content of batteries. This is a good example of how innovation can help reduce mineral demand in the face of rising costs and concerns about ESG considerations.

LFP batteries contrast with other chemistries in their use of iron and phosphorus instead of the more critical nickel, manganese and cobalt found in NCA and NMC variants of lithium-ion batteries. The downside of LFP is that their energy density tends to be significantly lower than that of NMC and NCA chemistries, although the gap has narrowed noticeably with the cell-to-pack design. In general, an increase in the market share of LFP batteries, as we are witnessing today, implies lower levels of mineral security concerns due to the absence of cobalt and nickel, whose supply chains are more geographically concentrated and prone to disruptions. Furthermore, the advent of a lithium manganese iron phosphate variant of the LFP battery could provide even higher density than conventional LFP, with mass production expected to start in 2024.

Cobalt Demand Outlook by Battery Chemistry Segment

In line with nickel, cobalt demand is likely to reach the bottom-end of our forecast, at 0.3M mt.

While the requirement for lithium content seems to be smallest among the needed materials, lithium is present across all chemistries. That is why we see little chance of substitution for lithium for EV use over the longer term. With 80% of lithium demand coming from EV use, metals prices are set to grow consistently over the coming decades, and widening deficit in 2030s would further propel the price momentum. The near-term outlook, as we have discussed in the lithium section, remains challenging given the uncertainty surrounding the Chinese demand the medium-term mine projects feasibility.

Lithium Demand Outlook by Battery Chemistry Segment

Despite lithium contributing only 4% to the battery composition, its use across all chemistries point to a continued demand growth until the end of the decade.

Researchers are exploring ways to improve battery technology, either through modifications to existing batteries or the introduction of new chemistries that rely less on hard-to-source materials. Factors such as speedy charging time, material efficiency, safety, and cost are all considered when improving battery density. One promising alternative to lithium-ion batteries is sodium-ion batteries, which use sodium as the main conducting element instead of lithium. While they may not improve energy density, they could significantly reduce costs as they rely on cheaper, less-critical materials. The HiNa brand has already introduced the first sodium-ion battery-equipped electric car, with two other Chinese cars, CATL and the Seagull by BYD, set to follow suit in 2023. However, it remains to be seen if sodium-ion batteries can meet the needs for EV range and charging time, which is why several companies are targeting less-demanding applications to start, such as stationary storage or micro-mobility.

Secondary Market

Another way to ensure a stable, secure, and sustainable supply chain is through an enhanced use of recycling technology. Even though clean energy technologies have significantly lower CO2 intensities throughout their lifespan compared to fossil fuels, their supply chains still contribute significantly to CO2 emissions and other pollutants. The production of materials and manufacturing of technology are responsible for more than 90% of emissions in the clean energy technology supply chains. Through recycling, the need for mineral extraction is reduced, along with the environmental damage it involves. Recycled production is generally less energy- and emission-intensive than primary production, reducing production-related emissions. For instance, recycled nickel requires only about 25% of the energy requirements of primary Class 1 nickel, while secondary aluminium production emits 96% less CO2 than primary. Recycling is crucial for growing EV sales, where the rate of deployment continues to grow even after 2030. Sales of passenger electric cars are expected to be nearly 70% higher in 2050 than in 2030.

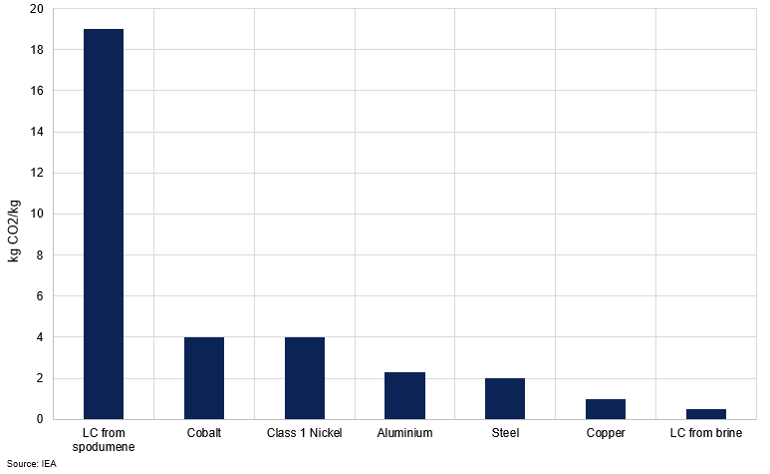

Mining and Processing CO2 Emission Intensity of Selected Materials (kg CO2/kg)

Most of the emission come from the energy during the processing stage. Among critical materials, spodumene (lithium) and cobalt have the highest CO2-emission potential, making the need for recycled material more crucial. However, the process behind it also must improve to ensure feasibility of recycled content being used in new vehicles. Optimal recycling methods depend heavily on the battery type: NCM batteries are better suited to hydrometallurgical methods because of the need to separate multiple metals, while pyrometallurgical methods are simpler for recycling LMO and LFP batteries. The recycling rates for materials are high, at 60%, 46%, and 32% for nickel, copper, and cobalt, primarily driven by content from EV battery packs. This level is, however, much lower for lithium, at 1.0%. The potential for recycled LIB may be as high as 50% as more EVs reach the end of life and more batteries find their way to secondary facilities, further highlighting the importance of recycling process. This should ease the burden on materials that are expected to fall into deficit by the end of the decade. For example, increasing recycling rates of lithium enables mining capacity to be expanded eightfold from 2021 to 2050, rather than 13-fold were recycling rates to remain constant.

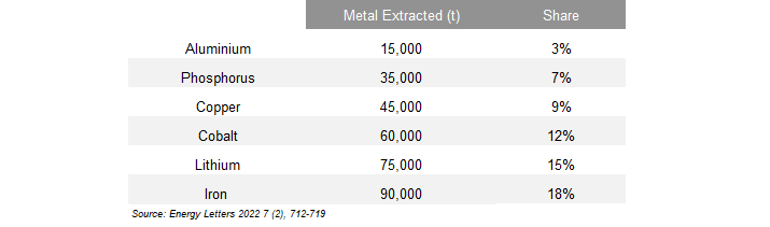

Potential for Battery Recycling from 500,000t of Batteries

The economic viability of lithium-ion battery recycling is only marginally profitable, as indicated by plans for recycling facility expansion and recycling cost estimates. While recycling is not currently mandatory in the US, it is being pursued due to economic incentives or funded research and development. Therefore, with mineral prices at multi-year lows and a continued shift away from nickel- and cobalt-rich chemistries, the battery’s worth to recyclers is further reduced. While we still expect to see continued improvement in recycling facilities, the profitability with current technologies is not enough to bring a strong expansion into the recycling market in the US. This is particularly significant for the American market, where the absence of federal battery recycling laws means that the process relies heavily on economies of scale and public funding. However, estimates suggest that a substantial portion of future EV material demand in the country can be met with recycled content. By 2050, recovered material could supply approximately 45-52% of cobalt, 40-46% of nickel, and 22-27% of lithium.

While we still expect to see continued improvement in recycling facilities, the profitability with current technologies is not enough to bring a strong expansion into the recycling market in the US.

The majority of recycling capacity for batteries is located in China, with 230kt per year. China's black mass is expected to make up 55% of the global total by the end of this year, and this figure is set to grow year-on-year in double digits until the end of the decade. In Europe, regulations are now the biggest driver behind battery recycling. Policy support and incentives help to standardize battery design and classification of materials to ensure efficient scrap collection and recycling. As a result, Europe's share of the global scrap pool is expected to grow to 15% by 2030 (BMI). The European Commission has issued a legislative proposal within the framework of the European Green Deal and Circular Economy Action Plan. This proposal would set minimum recycled content requirements for cobalt (16%), lead (85%), lithium (6%), and nickel (6%). It would also set collection rate targets for EV batteries and eliminate collection charges for end-users. By 2031, 61% of batteries will have to be collected for recycling. Economic operators selling batteries, including automotive OEMs, would be required to establish supply chain due diligence obligations for responsible raw material sourcing. Companies are increasingly being held accountable for their environmental and social impact, and investors are demanding greater transparency and action on ESG issues. However, tougher government scrutiny of ESG and net-zero performance is also seen as the biggest hurdle to operations in the next 5 years, according to the survey from McKinsey. As recycling landscape continues to evolve, adherence to the proposed regulations will be key in the growing influence of ESG considerations in shaping industrial practices.