EUR / USD

The EUR/USD outlook appears mixed but tilted slightly bearish in the near-term due to several key macro factors. The European Central Bank is expected to cut rates by 25 basis points this week to 2.00%, while the Federal Reserve maintains a cautious stance amid trade policy uncertainty. Recent US economic data shows cooling but resilient conditions, with core PCE inflation moderating to 2.5% and consumer spending remaining positive.

The trade policy environment has become increasingly complex, with Trump's tariff agenda facing legal challenges but receiving temporary court relief. European economic data has been relatively stable, with inflation trending toward the ECB's 2% target, though manufacturing remains soft. The diverging monetary policy paths between the ECB and Fed, combined with heightened trade tensions and fiscal uncertainty in the US, suggest continued volatility ahead.

While Europe has shown economic resilience and attracted significant investment flows in 2025, the impact of potential auto and industrial tariffs poses risks to the region's export-oriented economy.

USD / JPY

The Bank of Japan's recent decision to set aside maximum provisions for bond transaction losses signals a strategic preparation for rising interest rates, marking a significant shift in Japan's monetary landscape. The BOJ's unprecedented move to raise provisions to 100% for fiscal 2024, increasing them by 472.7 billion yen, demonstrates the central bank's growing concern about potential losses as interest rates normalize.

Japanese economic indicators, particularly the services sector performance and wage growth data, will be crucial in determining the BOJ's timeline for potential policy normalization. The combination of persistent inflation concerns and the BOJ's preparatory measures suggests the increasing probability of monetary policy adjustment in the medium term. Market participants are closely monitoring Japan's wage growth data, as sustained increases could provide the BOJ with the confidence needed to begin normalizing its ultra-loose monetary policy.

The interplay between US labour market data and Japanese economic indicators will be crucial in determining the currency pair's direction, as diverging monetary policies between the Fed and BOJ continue to be a primary driver of exchange rate movements.

GBP / USD

The British pound faces growing headwinds amid a complex macroeconomic environment shaped by trade uncertainties and diverging monetary policies. Rising gilt yields pose a key financial stability risk, according to BoE officials, while Trump's evolving tariff policies inject additional volatility into currency markets. The UK's sticky inflation at 3.5% versus US levels around 2.6-3.0% complicates the interest rate differential picture.

Market sentiment remains particularly sensitive to US employment data due this week, with expectations of 130,000 new jobs potentially influencing Fed policy timing. Global liquidity conditions and trade negotiations between major economies continue to drive broader currency movements.

The upcoming ECB meeting and its likely 25bp rate cut could also impact relative currency valuations. Sterling's near-term direction will largely depend on how these competing factors resolve, particularly the cut by major central banks, which could put additional pressure on the BOE to cut rates, weighing on the overall sterling outlook in the medium term.

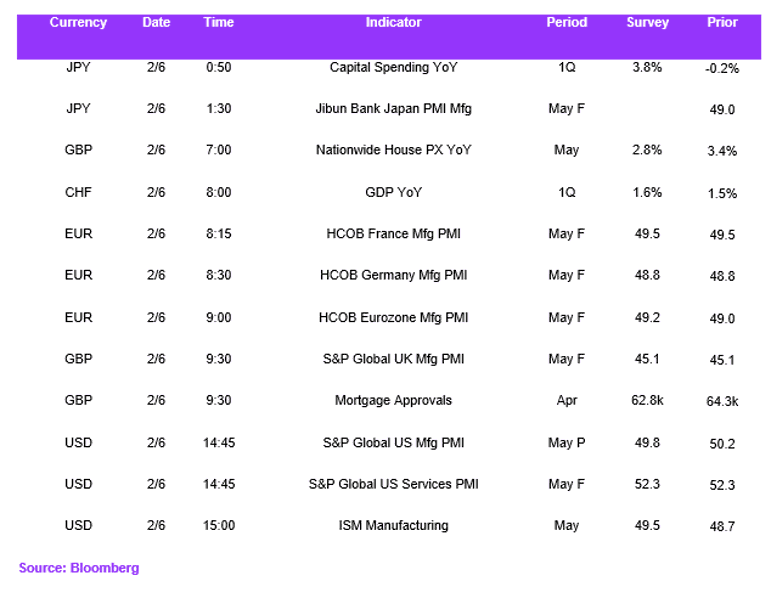

Economic Calendar