EUR / USD

EUR/USD strengthened, mainly due to weaker-than-expected US core CPI data, which came in at 0.1% MoM, compared to the anticipated 0.3%. This bolsters the case for the Federal Reserve to consider a rate cut later in the year. Additionally, even the announcement of a trade truce between

China and the US, with tariff postponements scheduled until August 10th, did not ease the short-term pressure on the dollar.

Technical analysis reveals strong buying pressure with the pair trading comfortably above major moving averages, including the 20-day SMA at 1.1350, 50-day at 1.13, and 200-day at 1.08, while the RSI reading of 62 confirms the bullish momentum.

Market sentiment has shifted notably bearish for the US dollar, with traders now pricing in a 60% probability of a Fed rate cut by September, while the pair's immediate technical outlook suggests potential for further gains beyond the 1.149 resistance level, targeting the April high of 1.156.

USD / JPY

USD/JPY held its nerve, held back by short-term moving averages on the downside, while the resistance level at 145 has capped the upside potential. The price movement has been moderate, even as there has been a decline in PPI pressures, which indicates a possibility of moderating prices in Japan. Notably, the PPI slowed from 4.1% to 3.2%. This indicates that technical levels, particularly the resistance at 145.00, are a crucial threshold for the pair in the near term.

As a result, market expectations for BOJ policy tightening have been significantly delayed, with traders now anticipating rate hikes no earlier than late 2025 or early 2026, as the central bank confronts possible deflationary pressures.

The pair's technical analysis shows moderate volatility, with prices currently trading above short-term major moving averages, finding immediate support at the 50-day SMA of 144.25. In the meantime, we expect technical indicators, alongside moving averages, to guide the pair's momentum in the near term.

GBP / USD

GBP/USD held its nerve as the dollar remained subdued amid a softer-than-expected US CPI data at 2.4%. The Bank of England's cautious monetary stance, coupled with market pricing in potential rate cuts starting August 2025, suggests a challenging environment for sterling in the medium term. Moreover, the recently announced UK spending review, indicating a modest 2.3% annual real-term growth in departmental budgets, highlights fiscal constraints that could further impact the sterling's performance.

Despite these headwinds, the pound has demonstrated short-term resilience above key technical levels, maintaining positions above the 20-day moving average at 1.34 and the 50-day moving average at 1.33.

The pair's immediate technical outlook suggests potential for upward movement if buyers can breach resistance at 1.36, though this optimism is tempered by the combination of deteriorating UK labour market conditions and fiscal tightness that may weigh on sterling's prospects.

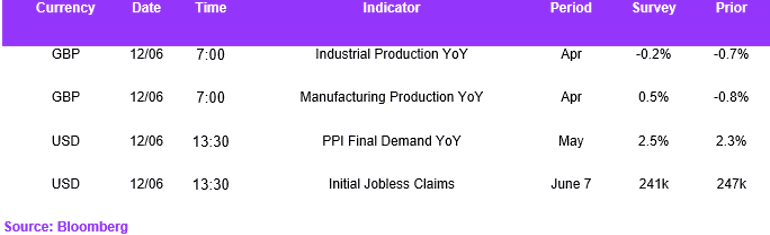

Economic Calendar