EUR / USD

EUR/USD remained elevated, holding above 1.16 but struggling to supersede yesterday's highs of 1.1641. Euro strength is primarily driven by a broader weakening of the US dollar and shifting Federal Reserve policy expectations. Recent US economic data disappointments, including weak consumer confidence and housing market indicators, have reinforced market expectations for Fed rate cuts as early as July, creating a supportive environment for the euro.

The technical picture remains decidedly bullish, with the pair trading well above all major moving averages and maintaining significant distance from the 200-day SMA at 1.08, while the RSI at 65.66 suggests strong upward momentum without reaching overbought conditions. The recent Middle East ceasefire agreement has reduced safe-haven demand for the dollar, while capital flows increasingly favour the euro as US yields become less attractive.

Despite mixed eurozone economic fundamentals, including contracting business activity, the divergence between Fed and ECB policy paths continues to support the euro's ascent, with the potential for testing the 1.17 psychological level if upcoming US economic data remains soft. However, the sustainability of the rally may depend on whether the Middle East ceasefire holds and if profit-taking accelerates, with the 50-day SMA at 1.137 serving as a potential pullback target.

USD / JPY

USD/JPY held within yesterday's range, as moving averages create a tight trading range. The Bank of Japan signalled a potential shift from its historically accommodative monetary stance, with BOJ board member Tamura suggesting decisive rate hikes may be necessary if inflation risks escalate. Recent Japanese economic data, particularly the stronger-than-expected services PPI at 3.3%, indicates persistent inflationary pressures that could accelerate the BOJ's policy transition.

The technical outlook shows the pair trading above the 50-day MA at 144.25 and the 20-day MA at 144.54, though remaining below the 100-day MA at 146.63. The recent geopolitical de-escalation between Israel and Iran has weakened safe-haven demand for the US dollar, while the Federal Reserve's cautious approach to rate cuts has created uncertainty around the dollar's yield advantage.

The pair's immediate technical levels suggest further sideways movement. Internal disagreements among BOJ policymakers regarding the impact of US tariffs on Japan's economy could create policy uncertainty and weaken the yen's longer-term outlook.

GBP / USD

GBP/USD remained elevated, holding above 1.36, its highest level since January 2022, representing an impressive 8.7% gain against the USD year-to-date. Technical indicators support the bullish outlook, with the currency pair trading comfortably above major moving averages, including the 20-day SMA at 1.352, while the daily RSI at 62 suggests potential for further upside.

The pound's apparent strength, however, appears to be more a reflection of broad dollar weakness rather than inherent sterling strength, as evidenced by its 2.9% decline against the euro this year. Recent developments, including the Iran-Israel ceasefire announcement, have contributed to improved risk sentiment, further pressuring the dollar while supporting risk-sensitive currencies like the pound.

The pair's future trajectory faces potential headwinds from both technical and fundamental perspectives, with immediate resistance at the psychological level of 1.37 and support at 1.35, while Bank of England Governor Andrew Bailey's indication of continued interest rate cuts could limit sterling's upside potential. Market participants are currently pricing in an 80% probability of a BoE rate cut in August, while the softening UK labour market and potential political challenges surrounding welfare system reforms could introduce additional uncertainty to the pound's outlook.

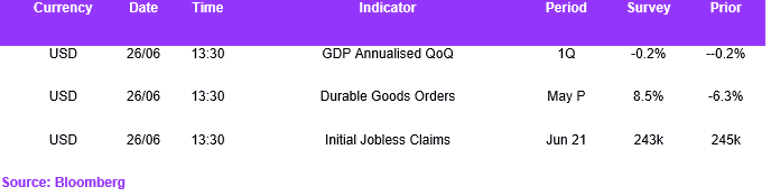

Economic Calendar