EUR / USD

EUR/USD remained elevated despite the ECB acknowledging slower growth expectations for the Eurozone, while the Federal Reserve maintains a hawkish stance focused on inflation concerns.

Technical analysis shows the pair trading between critical levels, with the 50-day moving average at 1.16 serving as solid support and 1.17 providing resistance. Market positioning indicates an 84% probability of a Fed rate cut in September, though this sentiment could shift following Fed Chair Powell's Jackson Hole speech.

A decisive break above 1.173 could target 1.181, while a drop below 1.156 might test the early August low of 1.140, making these levels crucial for determining the pair's medium-term direction.

USD / JPY

USD/JPY remained in a tight balance as the dollar remained stable. Japanese government bond yields have reached 16-year highs, creating a supportive environment for the yen, while technical indicators show the currency pair trading between critical support at 146.73 and resistance at 149.08. The monetary policy divergence between the Fed and BOJ remains a crucial driver, with markets pricing in potential Fed rate cuts while the BOJ maintains its trajectory toward policy normalisation.

Recent price action shows USD/JPY consolidating between the 50-day moving average at 146.73 and the 200-day moving average at 149.15, with significant volume spikes observed during early trading sessions. Technical analysis suggests a continuation of this momentum in the near term.

GBP / USD

GBP/USD weakened yesterday, influenced by the unexpected rise in UK inflation to 3.8%, which has forced market participants to reassess their Bank of England rate cut expectations. The increase was driven by higher airfares (30%!) and food costs, with food and non-alcoholic beverages up 4.9% YoY, the fastest pace since February. The Bank of England expects inflation to peak at 4% in September, double its 2% target, with food prices a key contributor. Services inflation, a measure closely watched by policymakers, climbed to 5% in July from 4.7% the month before, underlining persistent price pressures across the economy.

Markets took the latest CPI figures in stride, having already pared back expectations for further easing after August's cut. Swaps now imply around a 50% probability of another quarter-point reduction before year-end.

Technical analysis reveals a precarious position as the currency pair declined by 0.18%, moving from 1.348 to 1.3454, while maintaining a delicate balance above its 100-day moving average at 1.3410. The pair's immediate technical outlook appears neutral, with the RSI at 49 and price action contained between the 50-day SMA and the 100-day SMA, suggesting a period of consolidation. The Federal Reserve's hawkish stance on inflation risks, combined with the UK's persistent inflation concerns, continues to shape the pair's fundamental outlook.

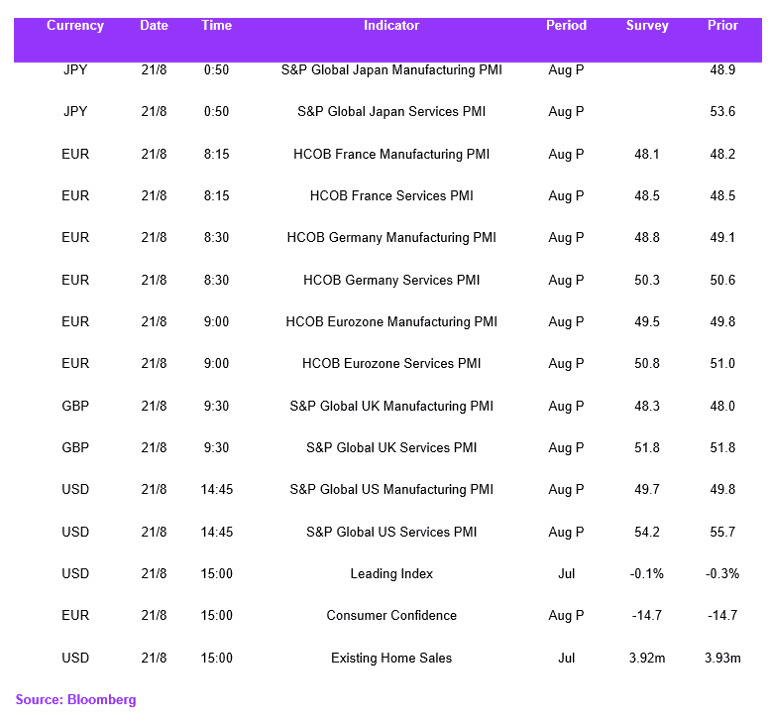

Economic Calendar