EUR / USD

The EUR/USD pair faces headwinds as recent Eurozone economic data disappoints, with economic confidence falling below expectations to 95.2 in August 2025, while French political uncertainty adds to regional concerns. In contrast, the US economy shows resilience with Q2 GDP revised upward to 3.3% QoQ, though political tensions surrounding the Federal Reserve's independence create an element of uncertainty following President Trump's dismissal of Fed Governor Lisa Cook.

The pair's technical structure reveals a cautiously bullish bias, trading above the 200-day moving average at 1.11, though resistance near the 50-day moving average at 1.17 poses a significant hurdle. The diverging monetary policy expectations between the ECB and Fed, with markets pricing in an 88% probability of a Fed rate cut in September while the ECB maintains a more hawkish stance, continues to drive increased volatility in the pair.

The immediate technical outlook suggests potential for further upside if buyers can overcome resistance at 1.174, though failure to maintain support at 1.157 could trigger a reversal toward 1.150.

USD / JPY

The USD/JPY pair faces mounting downward pressure as fundamental factors increasingly favour yen strength, primarily driven by the Federal Reserve's pivot toward monetary easing and the Bank of Japan's more hawkish stance. The threat of Japanese intervention remains on the table, particularly as the pair approaches the psychologically important 150 level that previously triggered action in 2022.

Technical analysis reveals bearish momentum, with USD/JPY trading below key moving averages and showing significant market interest around the 147.00 psychological level. The narrowing interest rate differentials between the US and Japan, coupled with the BOJ's credible hawkish bias supported by above-target Tokyo inflation, suggest continued compression in the monetary policy gap.

Market positioning presents a striking imbalance, with retail traders heavily positioned against the yen while institutional investors take the opposite side, creating potential for sharp moves if retail positions are forced to unwind. The combination of these technical and fundamental factors, along with intervention risk and vulnerable market positioning, points to an improving outlook for the Japanese currency as we approach year-end.

GBP / USD

The GBP/USD pair continues to show strength, primarily driven by shifting monetary policy expectations and the Bank of England's neutral-hawkish stance amid persistent UK inflation pressures. Market expectations for UK rate cuts in 2025 have decreased to 40% probability, down from 100% earlier this month, while the US dollar faces pressure from concerns about Federal Reserve independence.

The technical landscape shows the pair maintaining positions above crucial levels of 1.31 and 1.33, with recent price action indicating a potential consolidation phase as the currency trades near both its 20-day and 50-day moving averages at 1.35. The yield spread dynamics favour sterling, with UK 2-year yields now commanding a 30+ basis point premium over US yields, representing a notable shift from July's positioning.

Despite the positive momentum, both technical and fundamental risks persist, as the pair faces resistance at 1.36 while the British economy grapples with structural challenges, particularly the upcoming autumn budget and a cooling labour market.

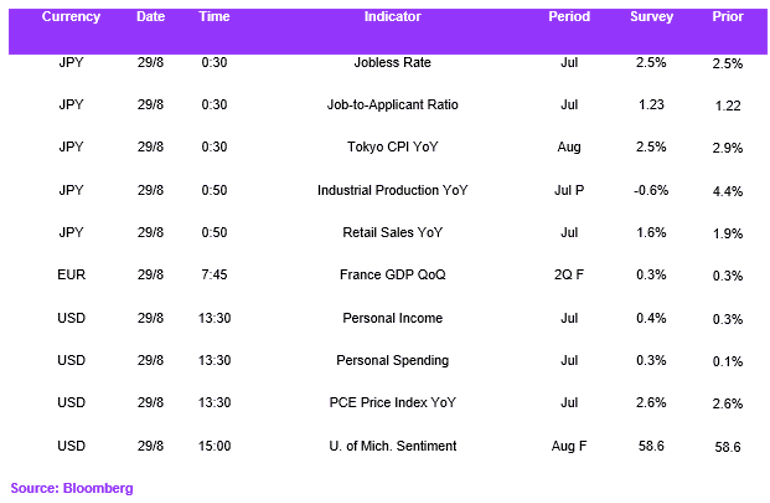

Economic Calendar