EUR / USD

EUR/USD remains resilient, supported by a weaker dollar, which is driven by signals of potentially two more cuts from the Fed this year, creating a favourable environment for euro strength. The divergence in monetary policy stances between the Fed and ECB has become more pronounced, with markets viewing the ECB as largely finished with its rate-cut cycle while expecting additional Fed easing.

Technical indicators reinforce this positive outlook, with EUR/USD maintaining positions above crucial moving averages, including the 20-day and 50-day moving averages at 1.1740 and 1.1678, respectively, while the RSI reading of 58.50 and flat suggests a moderating bullish momentum without entering overbought territory. Recent eurozone economic data has shown resilience, with the composite PMI strengthening modestly in September, rising to 51.2, extending the current run of growth to nine months. The headline masked diverging trends, with Germany showing renewed momentum while political uncertainty continued to weigh on France. The services sector drove the expansion, with its PMI improving to 51.4 from 50.5 in August.

The combination of Fed Governor Bowman's dovish comments about labour market weakness and the high probability (91%) of another Fed rate cut in October suggests continued pressure on the dollar, with potential for EUR/USD to test the resistance level of 1.187 and possibly extend toward 1.19 if this level is breached.

USD / JPY

USD/JPY faces moderate pressure as support and resistance levels in the form of moving averages keep the pair in range. Technical analysis shows the currency pair trading between 147.45 and 147.91, with critical moving averages clustered around 147.60 serving as immediate support levels.

Fed Governor Bowman's dovish stance regarding labour market conditions, coupled with political uncertainties surrounding Fed independence, has created notable headwinds for the dollar against the yen. Meanwhile, the Bank of Japan's commitment to ultra-loose monetary policy, despite some scaling back of asset support, continues to be a fundamental driver for the pair's movement.

Growing concerns about US government shutdown risks and funding negotiations are introducing additional uncertainty into the market, while technical indicators suggest potential for upward movement if the pair breaks above the resistance cluster near 148.35, with 149.00 serving as the next psychological target.

GBP / USD

GBP/USD edged cautiously higher to 1.3520 as the UK grapples with persistent inflation challenges, with OECD projections indicating the highest inflation rate among G7 nations at 3.5% in 2025. Technical analysis shows the pair maintaining position above the cluster of short-term moving averages at 1.35, with the next support at 1.33 and resistance at 1.36, while trading activity remains concentrated around the 1.352 level.

The pair's near-term outlook appears constrained by multiple factors, including the UK's slowing GDP growth forecast of just 1% for 2026 and the recent decline in business activity as reflected in September's PMI data. In particular, the composite PMI slowed to 51.0 from 53.5, reflecting a weaker performance in both services and manufacturing. Firms reported pressure from higher costs linked to recent tax increases, adding to speculation that further fiscal tightening could emerge in the November budget. The Bank of England's slightly more optimistic stance on inflation, as indicated by chief economist Huw Pill, provides some support for sterling, though this is tempered by ongoing concerns about sticky price pressures in services and wage inflation.

The currency pair's future trajectory will likely be determined by both technical factors, with a potential upside target of 1.38 if resistance at 1.36 is breached, and fundamental developments, including upcoming PCE inflation data, Federal Reserve commentary, and the UK's autumn budget announcements.

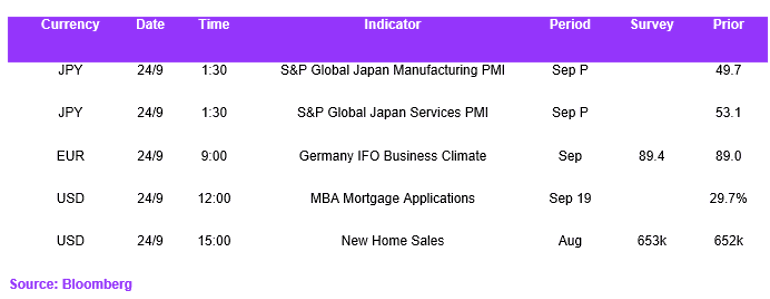

Economic Calendar