EUR / USD

EUR/USD faces significant downward pressure as recent US economic data continues to showcase resilience, with Q2 GDP revised upward to 3.8% and jobless claims dropping to 218,000. The stark contrast between US economic strength and European challenges is evident, as German consumer confidence remains in negative territory despite a slight improvement to -22.3.

Market sentiment has shifted notably, with the probability of a Fed rate cut in October declining to 84%, while Fed officials maintain a cautious stance on potential rate adjustments. The technical outlook appears bearish, with the pair breaking below key support at 1.1700 and the RSI dropping to 43, suggesting momentum remains with sellers.

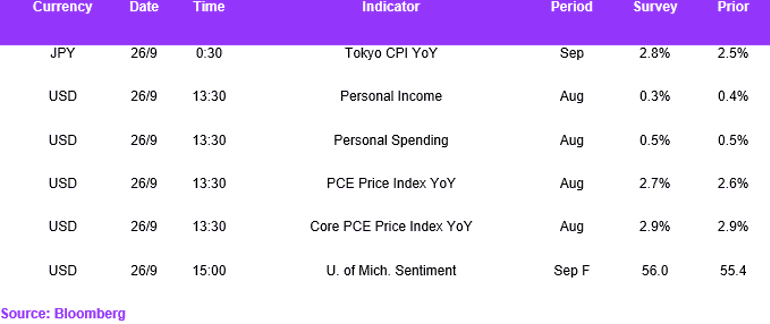

Today's US PCE headline inflation is expected to rise to 2.7% in August, up from 2.6% in July, while the core inflation rate is anticipated to remain unchanged at 2.9%. Both figures are significantly above the 2.0% target, which may lead to a reduction in expectations for a 50 basis point increase for the remainder of the year, potentially benefiting the dollar. In July, while goods inflation may have increased slightly, the main contributor to inflation was an uptick in services. This suggests that bringing inflation down could be challenging enough that the Federal Reserve may be reluctant to implement two rate cuts.

The currency pair's immediate trajectory appears weighted to the downside, with critical support at 1.1589 at the 100 SMA serving as a pivotal level that, if breached, could accelerate the decline toward 1.140.

USD / JPY

USD/JPY continues to demonstrate significant upward momentum, driven primarily by the stark policy divergence between the Fed and Bank of Japan, with recent price action pushing the pair from 148.80 to 149.80. Strong US economic fundamentals, including Q2 GDP growth of 3.8% and declining jobless claims, provide substantial support for the dollar against the yen.

The technical outlook seems to be stagnating on the upside, with the pair trading above its 200-day moving average at 148.48, though the psychological 150 level looms as significant resistance. Japanese inflation pressures continue to be a concern. The services PPI increased by 2.7% YoY in August, and expectations suggest that the Tokyo CPI may rise to 2.8% in September, up from a downwardly revised 2.5%. This increase could help reinforce the likelihood of a 25bps interest rate hike by the end of the year and may strengthen expectations for a rising yen.

Recent BOJ meeting minutes reveal growing hawkish sentiment among some policymakers, indicating that the current policy divergence between the US and Japan might begin to narrow. The immediate trajectory for USD/JPY appears tilted to the marginal upside, with potential targets at 151.50 if US yields continue their ascent, though any sudden shift in BOJ policy or deterioration in risk sentiment could trigger a retreat toward the 148.7 support level. Today's data will be crucial in guiding the pair's narrative.

GBP / USD

GBP/USD faces significant downward pressure as recent price action shows a decisive break below key moving averages, with the pair finding temporary support at 1.3300. The Bank of England's hawkish stance on rates, while traditionally supportive of sterling, is being overshadowed by growing dollar and mounting concerns over the UK's deteriorating economic and fiscal conditions.

Strong US economic data, including GDP growth of 3.8% and improving labour market conditions, has reinforced dollar strength against the pound, creating additional headwinds for the currency pair. The divergence between the BoE's restrictive policy and the Fed's potential rate cut trajectory is creating a complex trading environment, particularly as UK economic indicators suggest a faster-than-anticipated deceleration.

Technical analysis indicates that the breach of 1.3300 accompanied by high trading volume signals strong bearish conviction, with the next significant support level at 1.3142 should current levels fail to hold.

Economic Calendar