EUR / USD

The EUR/USD pair continues to display weakness as mixed economic signals and evolving monetary policy expectations shape market sentiment. Recent Eurozone consumer confidence data holding steady at -14.2 in November provides some stability, yet is overshadowed by robust US employment figures showing 119,000 new jobs in September.

The divergence between ECB and Federal Reserve policy stances remains a key driver, with markets pricing in fewer rate hikes from the ECB while the Fed maintains a relatively hawkish position. Technical analysis reveals the pair trading above the critical 200-day moving average at 1.15, with immediate resistance formed by the 50-day and 20-day moving averages at 1.16.

The dollar's strength is further bolstered by its safe-haven status amid broader market risk aversion, while the euro faces continued pressure from subdued demand for euro-denominated assets. A decisive break below the 200-day moving average could trigger a decline toward November lows, while upside potential appears limited unless the pair can overcome resistance at 1.17.

USD / JPY

he USD/JPY pair has demonstrated remarkable strength, maintaining levels above 157 and reaching 10-month highs amid significant pressure on the Japanese yen. This upward momentum has been primarily driven by the stark policy divergence between the Federal Reserve and Bank of Japan, with the latter maintaining ultra-loose monetary policy while the Fed remains hawkish.

The recent approval of a massive 21.3 trillion yen stimulus package by Prime Minister Takaichi's administration has further weakened the yen by raising concerns about Japan's fiscal health and debt sustainability. Technical indicators reveal significantly overbought conditions with an RSI reading of 77.52, suggesting a potential correction might be on the horizon. Despite Finance Minister Katayama's escalating intervention warnings, markets appear to be targeting the 160 level before any intervention becomes likely.

The moderation in Japanese export growth to 3.6% year-over-year in October, combined with persistent core inflation at 3%, presents additional challenges for the BOJ's policy normalization timeline and could maintain pressure on the yen in the near term.

GBP / USD

The GBP/USD pair faces mounting pressure as October's UK inflation decline to 3.6% has significantly increased expectations for a Bank of England rate cut, with markets now pricing in an 80% probability for December easing. The upcoming UK budget announcement on November 26 represents a critical juncture for sterling, as it must balance substantial funding needs with fiscal responsibility amid growing economic concerns.

Technical analysis reveals the pair trading below all major moving averages, with the 200-day SMA at 1.34 serving as substantial resistance, while immediate support rests at 1.30. The combination of a cooling labor market, reaching a four-year high in unemployment, and deteriorating consumer confidence suggests continued weakness in the British economy.

The US dollar's sustained strength, coupled with reduced Federal Reserve rate cut expectations, creates additional headwinds for the pair, while the RSI at 35 indicates oversold conditions without showing reversal signals. A break below the crucial 1.30 support level could trigger further sterling weakness, potentially pushing the pair toward 1.29, particularly if the upcoming budget announcement disappoints market expectations.

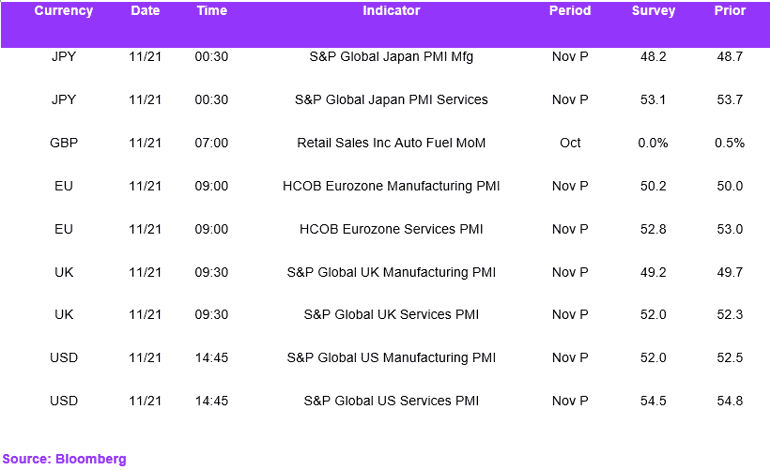

Economic Calendar