EUR / USD

EUR/USD continues to navigate a complex mix of trade frictions, shifting political risk premia and recalibrating rate expectations. The escalation in US–EU tariff rhetoric has altered capital flow dynamics, with repatriation risks rising as European investors reassess US policy stability. Meanwhile, confusion surrounding Fed leadership succession limits scope for aggressive easing, even as the ECB maintains a dovish bias supported by inflation now aligned with its 2% target.

The pair has dipped ~0.3% across three sessions, briefly breaking down from 1.162 to 1.158 before stabilising near 1.163. Daily RSI at ~31 signals oversold conditions, and price remains below the 20-, 50-DMA and 30-day VWAP around 1.17, while still holding above the 200-DMA at 1.16. A recovery above the 1.17 cluster would indicate upside momentum, while a breach of 1.16 risks an extension toward 1.150.

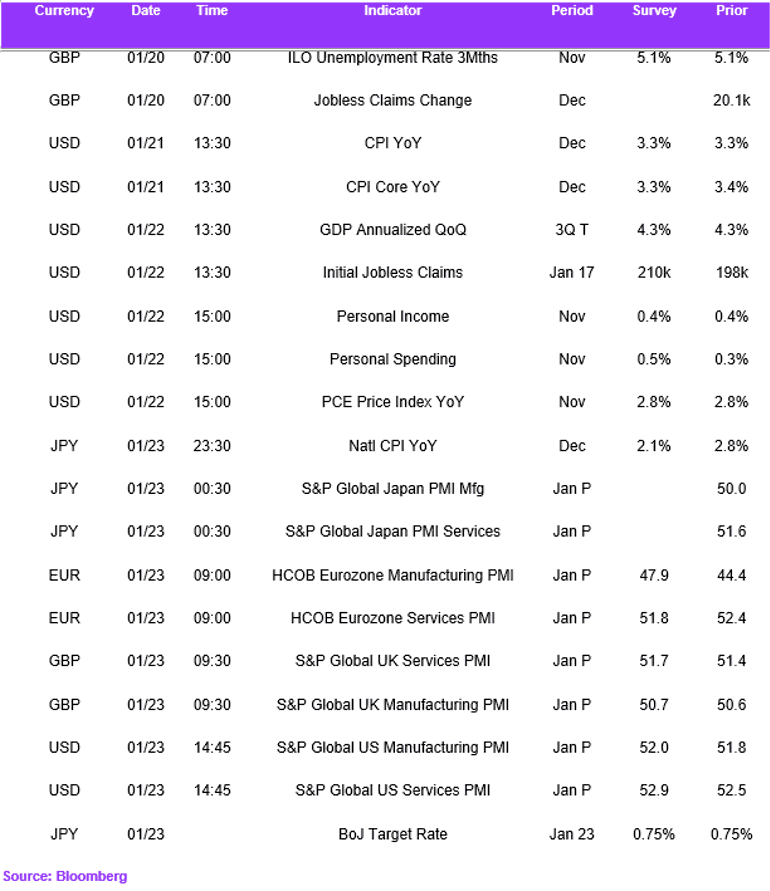

This week, we are focused on Eurozone PMI prints and US PCE. We see the PMIs as key for validating the Eurozone soft-landing narrative, while US inflation data could shape the Fed’s ability to cut later in H1. PMI resilience vs softer US inflation could bias EUR/USD higher, while the inverse pairing could reinforce dollar carry.

USD / JPY

USD/JPY is contending with narrowing policy divergence as the BoJ edges towards rate normalisation while the Federal Reserve maintains restrictive positioning. Rising consumer inflation expectations in Japan, plus tentative timelines for a spring/summer hike, are compressing rate spreads. The tariff dispute has also added safe-haven demand for the yen, while a proposed snap election and fiscal plans inject domestic volatility into the policy outlook.

Price has softened ~0.2%, slipping from ~159 toward 158 in a controlled range. Strong technical support near 157 is reinforced by the 20-DMA, 50-DMA and 30-day VWAP convergence. A break below 157 would shift risk toward 155, while re-establishing upside momentum above 158 would target the recent peaks.

The calendar puts Japan front-and-centre with Natl CPI, Japan PMIs and the BoJ rate decision. We expect markets to look for confirmation of the BoJ’s neutral rate assumptions and wage-price dynamics. We think positive surprises on CPI/PMIs plus constructive BoJ guidance would bias USD/JPY modestly lower, while BoJ ambiguity could favour stability ahead of US inflation data.

GBP / USD

Sterling faces meaningful headwinds as trade uncertainty, political risk and monetary divergence reshape the cross. With the BoE closer to easing than the ECB, and the Fed remaining cautious, the pound continues to behave more like a risk-sensitive asset than a haven. Structural vulnerabilities evident in housing and services reinforce the downside asymmetry.

GBP/USD slipped ~0.4% from 1.3403 to 1.3344 before recovering to ~1.3396. RSI at ~42 reflects softening momentum, while price trades within a heavy confluence zone around 1.34, where the 20-, 50- and 200-DMA align with the 30-day VWAP. A break below 1.3333 exposes downside toward 1.3045; sustained closes above the cluster would target 1.3464 then 1.3558.

We are focused on UK PMIs vs US PCE and US consumption data. UK PMIs will be pivotal for assessing whether softness remains confined to housing or broadens into services. Strong UK PMIs vs soft US inflation could support GBP/USD, but weak PMIs vs firm CPI/PCE risk keeping sterling vulnerable.

Economic Calendar