EUR / USD

EUR/USD retreated approximately 0.3% over the recent 24-hour period, settling around 1.1687 after reversing sharply from an intraday high near 1.1741, with the pair now trading just above the 200-day moving average at 1.1590.

Geopolitical tensions surrounding President Trump's tariff threats against European allies and discussions of military options regarding Iran have injected major uncertainty into the dollar trade, weakening dollar demand relative to the euro in recent days. Today’s moves indicate stabilisation of this selling momentum, after President Trump eased off the pressures on Greenland, citing a “framework” deal in the works.

Meanwhile, the European Central Bank maintains measured conviction toward current policy settings, with inflation anchored near target at 1.9% and regional sentiment surveys showing improvement despite trade tensions, providing underlying support for euro valuations.

The near-term trajectory will depend fundamentally on whether geopolitical tensions resolve through negotiated frameworks or escalate into broader trade disputes, with a sustained bounce from the 1.1680 support zone potentially targeting the recent swing high near 1.1740. The euro looks fundamentally supported at current levels, with short-term moving averages at 1.6650 acting as a pivotal point for continued resilience.

USD / JPY

USD/JPY currently sits at 158.30, above key technical support levels, including the 50-day moving average at 156.50, while the 100-day moving average at 153.60 serves as a distant floor. The pair traded within a contained 0.45% range over the past 24 hours, with volume spiking during the New York session recovery, which lifted prices from session lows near 158 to 159.

From a macroeconomic perspective, the pair faces conflicting forces creating substantial near-term volatility. Japanese fiscal policy concerns have intensified following Prime Minister Takaichi's tax-cutting announcement, triggering a bond market selloff with ten-year and forty-year JGB yields reaching multi-decade highs, reflecting deep structural concerns about Japan's debt-to-GDP ratio exceeding 240%. Simultaneously, the Bank of Japan's December rate hike to 0.75% signals monetary policy normalisation, with expectations for additional hikes potentially as soon as April.

The medium-term outlook remains decidedly bearish for USD/JPY as expectations solidify for multiple Bank of Japan rate hikes in the second half of 2026, potentially narrowing rate differentials with a Federal Reserve likely to cut rates—a dynamic that historically triggers unwinding of the yen carry trade and currency appreciation. Moreover, Japanese authorities have indicated that foreign exchange intervention remains an option if the yen weakens beyond psychologically significant levels near 160.

GBP / USD

GBP/USD is currently consolidating around a technically significant confluence zone near 1.34, where the 200-day, 50-day, and 20-day moving averages cluster, creating a critical support and resistance area. UK inflation data showed headline CPI accelerating to 3.4% in December, exceeding expectations. However, given that this increase is driven by rises in tobacco duty and air fares, the expectation is that it is a temporary effect, keeping BOE’s cut expectations in place, with growing expectations for an April 2026 cut.

The macroeconomic backdrop reveals diverging forces, with the BoE's more cautious monetary policy stance providing sterling support, while the US dollar faces headwinds from geopolitical tensions surrounding trade disputes and eroding investor confidence in US leadership.

From a technical perspective, the pair traded with neutral momentum, as evidenced by the RSI reading of 51.4. This suggests that markets are likely to remain within a narrow range in the coming days, with support at 1.34 likely to be strong and potential resistance at 1.35.

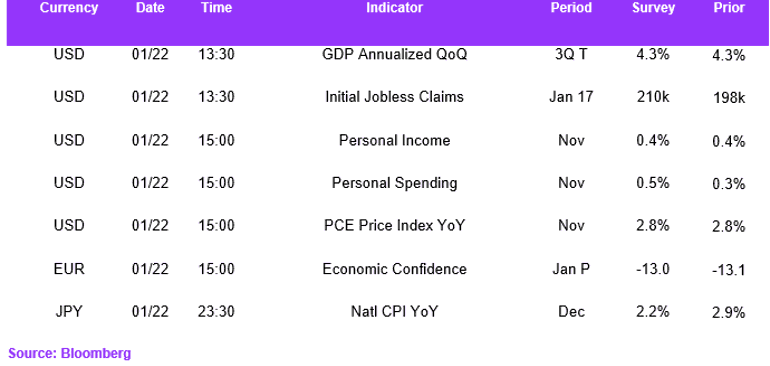

Economic Calendar