EUR / USD

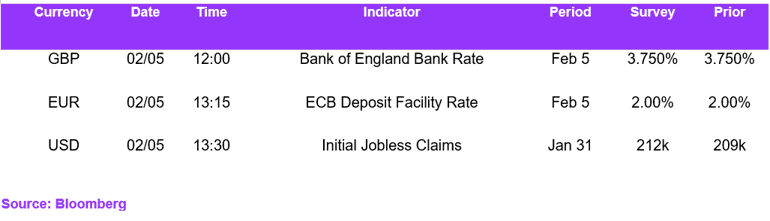

EUR/USD is trading within a narrow range as markets look through today’s European Central Bank decision, which we expect to leave rates unchanged and, crucially, to reinforce the message that the easing cycle is complete. With eurozone inflation now below target but stabilising, we see the ECB shifting firmly into a wait-and-see stance rather than signalling further accommodation. As a result, euro dynamics are increasingly driven by relative US developments rather than expectations of additional ECB easing.

The US dollar has regained some traction on resilient US activity data and a reassessment of the Federal Reserve’s willingness to cut rates aggressively. We expect the Fed to remain cautious, keeping rate differentials supportive of the dollar at the margin, even as peak policy rates are firmly behind us.

From a technical perspective, EUR/USD is consolidating just above the key 1.17 support zone, where the 200-day and 50-day moving averages converge, while trading marginally below the 20-day SMA near 1.18. The RSI at 52 signals neutral momentum. We expect the pair to remain range-bound in the near term, with a sustained hold above 1.17 allowing scope for a move towards 1.1858, while a break lower would expose downside towards 1.1683 as dollar support reasserts itself.

USD / JPY

USD/JPY continues to trade with an underlying bid, supported by relative policy divergence and domestic Japanese fiscal dynamics. The pair remains above all key moving averages, with the 200-day SMA near 151 and the 20- and 50-day SMAs clustered around 156 providing a firm technical base beneath spot levels near 156.9. Momentum remains neutral-to-constructive, with the RSI around 55 consistent with consolidation rather than trend exhaustion.

Fundamentally, we see persistent headwinds for the yen stemming from Japan’s fiscal outlook and political developments. Prime Minister Sanae Takaichi’s expected electoral victory this weekend is likely to embolden expansionary fiscal and defence spending plans, while confidence in near-term Bank of Japan intervention capacity remains limited. At the same time, the dollar retains support from the Fed’s relatively restrictive stance.

We expect upcoming US payrolls data to be the key near-term catalyst. Evidence of labour market softening would cap USD/JPY upside by accelerating Fed cut pricing, but absent a clear downside surprise, we see risks skewed towards continued yen underperformance over the intermediate term.

GBP / USD

GBP/USD remains under pressure as markets look ahead to today’s Bank of England decision, which we expect to leave rates unchanged while maintaining a cautious, data-dependent tone. Unlike the ECB, the BoE still faces a more ambiguous inflation outlook, keeping expectations for eventual easing alive and reinforcing sterling’s sensitivity to relative rate dynamics versus the US.

Technically, GBP/USD has fallen around 0.6% over the past 24 hours to trade near 1.3612, slipping below the 20-day SMA and the 30-day VWAP at 1.36. Medium-term support remains intact above the 50-day SMA at 1.35 and the 200-day SMA at 1.34. We see global risk aversion, amplified by aggressive AI-related capital expenditure announcements and subsequent equity rotation, providing cyclical support to the dollar.

Looking ahead, we expect sterling to remain vulnerable unless UK data meaningfully outperforms. A sustained break below 1.35 would open downside towards 1.33, particularly if US employment data reinforces the view that rate differentials will continue to favour the dollar.

Economic Calendar