EUR / USD

EUR/USD faces renewed structural headwinds as monetary policy expectations diverge further between the Federal Reserve and the European Central Bank. We see the latest US employment data — with 130,000 jobs added in January and unemployment easing to 4.3% — reinforcing the narrative of relative US resilience. This has shifted market pricing towards a longer period of restrictive Federal Reserve policy, underpinning the dollar through supportive rate differentials. By contrast, the ECB remains broadly neutral with a modestly dovish bias, leaving the euro without a strong policy tailwind.

From a technical standpoint, the pair endured a volatile session, falling sharply to around 1.184 before recovering to trade near 1.187, consolidating around the 1.18 area where several short-term moving averages converge. We note that EUR/USD remains above the 200-day SMA at 1.17, which continues to provide near-term structural support. However, we expect that a sustained break below 1.184 could accelerate downside momentum towards the 1.171 support zone. Geopolitical tensions, including renewed US–Iran frictions and broader trade uncertainty, have reinforced risk-off sentiment, and we see this as supportive of safe-haven dollar demand in the near term.

USD / JPY

USD/JPY dynamics have shifted following Japan’s political turn towards fiscal easing under Prime Minister Sanae Takaichi. We see the government’s policy direction as alleviating immediate debt sustainability fears, contributing to a compression in the 2s30s yield curve spread and encouraging selective carry trade unwinding. This has supported the yen, even against a backdrop of firmer US Treasury yields and solid US labour data.

Technically, the pair is trading in oversold territory, with the RSI at 36 and price well below resistance defined by the 50-day SMA at 156 and the 20-day SMA near 155.50. The 200-day moving average around 152 represents a critical inflection point. We expect this level to determine short-term direction: a decisive break lower could see the pair retest the late-January low near 152.20, while successful defence may trigger a relief rally towards the 155.50 resistance area as oversold conditions attract tactical buying.

Looking ahead, we see the trajectory hinging on whether fiscal concerns remain contained and whether the Bank of Japan signals confidence in its tightening path. Any indication of sustained normalisation would reinforce yen strength, whereas renewed fiscal anxiety could stabilise USD/JPY.

GBP / USD

GBP/USD continues to contend with structural headwinds stemming from widening monetary policy divergence. We see the Bank of England’s cautious tone — with a split vote and downgraded growth projections — as contrasting with stronger-than-expected US labour data, which has reinforced expectations that the Federal Reserve will maintain elevated rates for longer. Higher US Treasury yields continue to support the dollar relative to sterling.

Technically, the pair has traded within a contained range, settling near 1.362 after retreating from intraday highs around 1.371. We note that GBP/USD is hovering just above the 1.36 confluence formed by the 20-day SMA and 30-day VWAP. A sustained break below this zone could open downside towards the 1.35 area at the 50-day SMA. While upcoming UK GDP data could provide temporary relief, we expect political uncertainty and relative rate dynamics to remain dominant drivers. Unless the pair can reclaim momentum above 1.371, risks appear skewed towards further consolidation or modest downside.

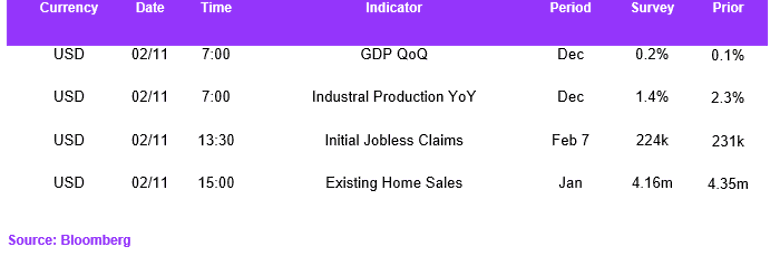

Economic Calendar