EUR / USD

EUR/USD was under significant pressure, declining approximately 0.56% to 1.1786 as divergent economic fundamentals and monetary policy expectations between the U.S. and the eurozone continue to widen. The Federal Reserve's hawkish pause, with markets pricing only 59-62 basis points of easing spread across 2026, sustains elevated real yield differentials that favour dollar assets and drive capital away from euro-denominated equivalents. Meanwhile, the eurozone struggles with weak growth momentum reflected in declining ZEW sentiment indices, leaving European policymakers trapped between sluggish activity and restrictive real rates that constrain the ECB's flexibility.

From a technical perspective, bearish momentum has firmly taken hold as the pair now trades below the 20-day SMA at 1.1860, with the next support of the 50-day SMA at 1.1688 not far from yesterday’s lows. The daily RSI, which has been dropping to approximately 45.5, is well below its prior-month average of 58. Institutional selling was evident during the European/U.S. session overlap, with volume surging around the 1.1815 breakdown level, reinforcing the move lower. Structural dollar inflows, including approximately $36 billion in Japanese capital commitments to U.S. energy and infrastructure projects, provide baseline support for dollar strength that extends beyond speculative positioning.

Looking ahead, the 50-day SMA represents a critical inflection point; a defence of this level could trigger a mean-reversion bounce toward the 1.18 area, particularly if U.S. monetary policy expectations shift. However, a decisive break below this level would expose the longer-term moving averages as support and confirm a broader trend reversal from the January highs. With the fundamental backdrop of persistent yield differentials and eurozone growth deficiencies, we favour further downside.

USD / JPY

USD/JPY rallied from 153.2 to nearly 154.8, shaped by diverging monetary policy trajectories and a recent sharp technical recovery. The narrowing interest rate differential between the Fed, holding rates at 3.50%–3.75%, and a Bank of Japan moving toward normalization with a neutral band of 1.5%–2.5% represents a secular headwind for the pair, while cooling U.S. inflation at 2.4% and market pricing of 50–59 basis points of Fed cuts through 2026 reinforce downward pressure on the dollar. However, structural support persists through Japanese commitments of up to $550 billion in direct U.S. infrastructure investment, generating long-duration capital flows that partially offset the deteriorating rate differential.

From a technical perspective, the pair's decisive 1% rally has shifted short-term momentum back toward neutral, with the daily RSI recovering to approximately 49, though price remains capped below the 100-day and 20-day SMA at 154.75. Historically elevated short positioning in the U.S. dollar, at 14-year highs, creates the potential for a tactical short-covering rally, even as longer-term fundamentals favour gradual yen appreciation. The key near-term battleground lies at the 155.0; a sustained break above would open a path toward the 156 zone.

Ultimately, Japan's strengthening export performance, up 16.8% year-over-year, driven by AI semiconductor demand, supports the case for continued BOJ tightening, yet modest GDP growth of just 0.2% annualised constrains the pace of normalisation, leaving USD/JPY in a fundamentally balanced but fragile equilibrium through the current quarter.

GBP / USD

GBP/USD weakened sharply, declining roughly 0.5% over the past 24 hours to trade near 1.3498, driven by a potent combination of sterling-negative domestic fundamentals and persistent dollar strength. The deteriorating UK labour market, with unemployment reaching a five-year high of 5.2% and wage growth decelerating to 4.2%, alongside cooling inflation at 3.0% has dramatically shifted market expectations toward Bank of England easing, with swap markets now pricing an approximately 80% probability of a rate cut as early as March. This dovish repricing stands in stark contrast to a divided Federal Reserve maintaining a cautious approach, which has kept Treasury yields elevated around 4.06-4.08% and widened the interest rate differential in the dollar's favour.

From a technical perspective, the pair now trades below both its 20-day moving average at 1.3650 and its 50-day SMA at 1.3527, with the daily RSI near 41, while near-term support rests at the 200-day moving average around 1.344. Institutional positioning reinforces the bearish outlook, as non-commercial traders have reduced long sterling exposure while increasing shorts, a behavioural shift near cyclical highs that frequently precedes broader price rotations. A decisive break beneath the 1.3494 level could expose the pair to a deeper slide toward 1.3352, particularly if incoming data, most notably US initial jobless claims and further UK employment readings, continues to reinforce the policy divergence narrative.

The structural backdrop remains firmly tilted toward further GBP/USD weakness, as the Bank of England's likely accommodation contrasts sharply with the Federal Reserve's reluctance to ease aggressively, making near-term rallies more likely to be viewed as selling opportunities rather than signals of trend reversal.

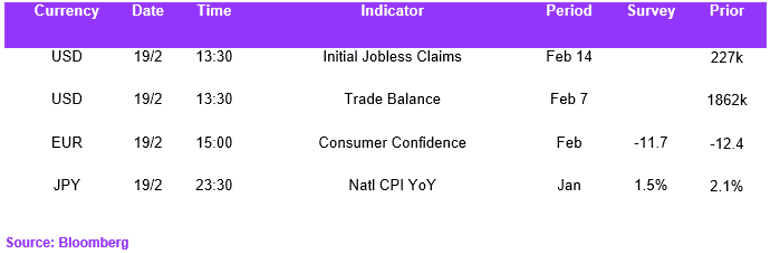

Economic Calendar