EUR / USD

EUR/USD is opening the week on a volatile note, led mostly by the dollar, as the rapid escalation of geopolitical risk in the Middle East left markets unable to respond to weekend announcements. Escalating Middle Eastern tensions and the threat of energy supply disruptions through the Strait of Hormuz are reinforcing expectations that the Federal Reserve will maintain its 3.5–3.75% rate range longer than anticipated, widening the policy differential against the ECB’s static 2.15% stance in favour of dollar strength. Simultaneously, safe-haven capital flows are actively realigning toward defensive assets such as the Japanese yen, the Swiss franc, and precious metals, creating additional headwinds for the euro.

Falling to 1.1732, the pair now sits virtually between both its 50-day and 100-day simple moving averages, while the daily RSI at approximately 41 reflects thoroughly neutral directional conviction. This technical stasis suggests that the pair is not in any overstretched position and is likely to be strongly dictated by dollar moves rather than by macroeconomic divergence between the two nations.

From a technical perspective, the 1.1850 level represents meaningful overhead resistance, while the 200-day SMA around 1.17 provides a solid structural floor well beneath current price action. The balance of risks appears tilted modestly to the downside in the near term, as the combination of energy-driven inflationary pressures compressing European manufacturing margins, persistent safe-haven demand favouring the dollar, and the absence of a clear catalyst for sustained euro strength suggests limited upside for EUR/USD absent a decisive geopolitical de-escalation or unexpected Fed rate-cut signals.

USD / JPY

The escalating Middle East conflict has fundamentally reshaped safe-haven currency dynamics, with the Japanese yen and the dollar both emerging as the primary beneficiary of heightened risk aversion. The potential blockade of the Strait of Hormuz threatens approximately 70-75% of Japan's oil imports and 60% of its liquefied natural gas supply, yet Japan's strategic reserves provide near-term buffers even as energy-driven inflation expectations, with Brent crude reaching $80 and potentially targeting $100, create a complex policy environment that pressures USD/JPY lower.

While the pair jumped to 156.88, the expectations point toward USD/JPY weakness into the 150.00-152.00 range as safe-haven flows accelerate. The carry trade unwinding mechanism amplifies downside risks for USD/JPY, as short yen positions accumulated during years of ultra-low interest rates face forced liquidation when safe-haven demand surges, overwhelming conventional technical support levels. The Bank of Japan's gradual tightening trajectory, with rates held at 0.75% and real rates remaining significantly negative, structurally incentivises this unwinding amid spiking geopolitical risk premiums.

Prime Minister Takaichi's stable political mandate and policymakers' recognition that sustained breaks below 150.00 would cripple Japan's export-dependent economy, establishing a policy floor that would constrain further downside. Ultimately, the critical variable determining near-term USD/JPY direction remains the duration and severity of Middle East supply disruptions rather than Bank of Japan policy actions, with the yen appreciating within bounds authorities will tolerate but not far enough to structurally impair Japan's manufacturing competitiveness.

GBP / USD

GBP/USD weakened sharply to 1.3380 on Monday open as escalating Middle East tensions have triggered broad risk-off sentiment, driving capital into safe-haven assets such as the US dollar, Japanese yen, and Swiss franc at sterling's expense. Disruption risks to the Strait of Hormuz, through which approximately 20% of global crude transits, have reignited inflation expectations. This energy shock threatens to delay Federal Reserve rate cuts, compressing sterling's yield advantage and supporting the dollar's resilience by widening real yield differentials.

Domestically, the pound is further undermined by deteriorating UK macroeconomic conditions, including rising youth unemployment, structural labour market weakness, and political uncertainty surrounding Prime Minister Starmer's leadership, all of which have eroded confidence in the medium-term growth outlook. The Bank of England's explicit easing bias contrasts with a repricing of Fed rate-cut expectations downward amid sticky US inflation data, reinforcing a monetary policy differential that favours the dollar.

From a technical perspective, GBP/USD is now trading below the 200-day and 100-SMA SMA at 1.3447 and 1.3399, respectively – for the first time since January, creating a stronger overhead resistance for the pair as European and US participants join the market during the day. We see sterling as a near-term short candidate, and with FX market liquidity compressed and downside risks remaining elevated, a decisive break below the 1.3360 support zone potentially opens the door toward deeper support at 1.3330.

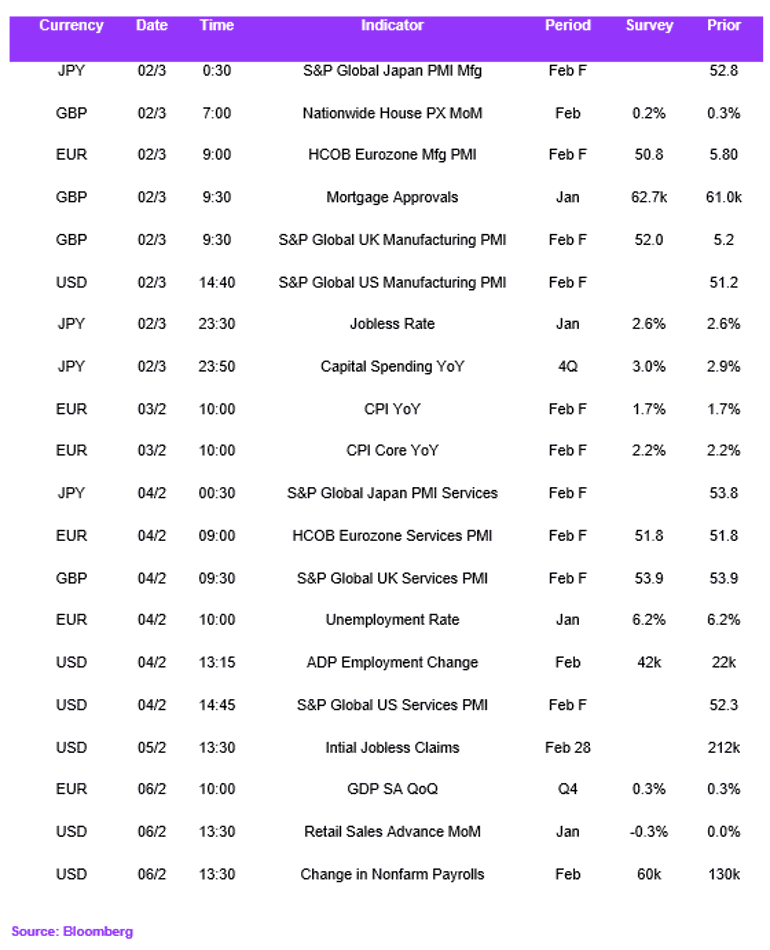

Economic Calendar