EUR / USD

Source: Massive (polygon.io)

EUR/USD remained under pressure on the back of a stronger dollar, driven by the continued influence of geopolitical risk and deteriorating eurozone fundamentals, as the Middle East conflict drives energy prices sharply higher and exposes Europe's acute import dependency. Sustained elevated crude prices above $84/bbl threaten to push eurozone inflation above 3% while simultaneously reducing growth, creating a stagflationary environment that severely constrains the ECB's ability to cut rates despite mounting economic weakness. Meanwhile, widening yield spreads, with 10-year Treasury yields at 4.1% against constrained German Bund yields, and robust safe-haven demand for the dollar, bolstered by US energy independence, have established a firmly bearish macro backdrop for the pair.

The technical picture corroborates this fundamental weakness, with EUR/USD declining to a low near 1.1559 before partially recovering to approximately 1.1606, trading well below its clustered 100-day and 200-day moving averages of 1.1680. While the daily RSI at approximately 31 signals deeply oversold conditions that could catalyse a short-term relief rally back toward the 200-day moving average, the widening gap between spot and overhead resistance at 1.17–1.18 reflects a deteriorating trend likely to attract further selling.

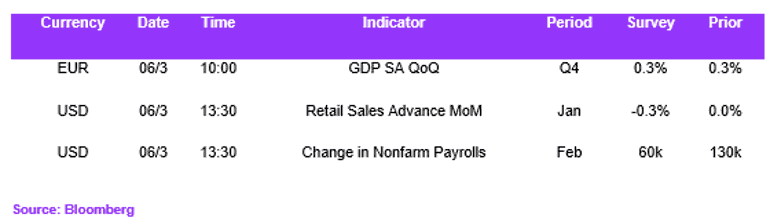

The upcoming February nonfarm payrolls report represents a critical near-term catalyst, with consensus estimates pointing to meaningful deceleration from January's 130,000 gain as temporary weather disruptions and a significant healthcare strike weigh on the headline figure. For EUR/USD specifically, a weaker print would likely support the euro by introducing recession concerns and reinforcing expectations for eventual Fed easing, while a stronger reading would maintain upward pressure on the dollar amid persistent inflation concerns from energy price spikes.

USD / JPY

Source: Massive (polygon.io)

The USD/JPY pair remains firmly supported by a widening macroeconomic divergence between the US and Japanese economies, driven primarily by escalating geopolitical tensions in the Middle East. Higher energy prices disproportionately burden Japan, a major energy importer, worsening its current account position and weakening the yen, while simultaneously benefiting the US, an energy exporter. This fundamental asymmetry is compounded by a hawkish Fed pushing back rate cut expectations and a politically constrained Bank of Japan unlikely to tighten meaningfully, further widening interest rate differentials in the dollar's favour.

From a technical perspective, USD/JPY is trading at approximately 157.52, well above key support levels including the 50-day SMA at 156.11, and the 100-day SMA near 155.54, confirming the prevailing bullish structure. The RSI at 62 reflects meaningful upside momentum, though late-session rejection from the 157.84 high signals indecision near the critical 158 resistance zone.

An upcoming US payrolls print below 130,000 would materially shift the calculus by introducing genuine growth concerns capable of triggering a retracement toward the 155–155.50 support confluence, while a reading above 170,000 would cement the Fed's hold bias and likely propel USD/JPY toward a retest of the 159 resistance zone. Ultimately, the pair's medium-term trajectory hinges on whether the employment report confirms sufficient labour market resilience to justify sustained rate elevation amid rising energy costs, or deteriorates enough to pivot Fed policy toward accommodation and relieve upward pressure on USD/JPY.

GBP / USD

Source: Massive (polygon.io)

GBP/USD remained suppressed from both macroeconomic and technical perspectives, with escalating Middle East tensions and energy supply disruptions creating pronounced headwinds for sterling against the safe-haven dollar. The Bank of England faces a complex policy dilemma as supply-chain disruptions and energy-driven inflation risks complicate the anticipated timeline for rate cuts. The divergence in monetary policy expectations between the Fed and BoE, compounded by significant net short sterling positioning among asset managers, suggests further downside risks remain embedded in the market.

The upcoming February nonfarm payrolls report represents a decisive catalyst for the pair, with consensus expectations ranging from 55,000 to 60,000 jobs - a sharp decline from January's 130,000 - driven by the healthcare strike and weather-related disruptions. A weaker-than-expected print would likely weaken the dollar and offer the pound a reprieve, potentially allowing GBP/USD to reclaim the 200-day SMA and trigger a mean-reversion squeeze.

From a technical standpoint, the pair is trading well below all major moving averages, while the RSI at approximately 33 reflects deeply oversold conditions following the sustained decline from the late-January high near 1.385. The critical level to watch is support around 1.332, where a hold could trigger a mean-reversion rally toward 1.34, though the fundamental backdrop of dollar strength and geopolitical risk premiums argues against a strong recovery in the face of a weaker US labour print.

Economic Calendar