EUR / USD

Source: Massive (polygon.io)

EUR/USD is facing a complex macro environment as deteriorating US labour data collides with powerful countervailing forces that have nevertheless supported the dollar. February’s nonfarm payrolls report showed a contraction of 92,000 jobs, well below expectations for a gain of roughly 59,000 and marking a sixth consecutive monthly decline. Ordinarily, we would expect such labour market weakness to strengthen the case for Federal Reserve easing and support the euro. However, the sharp surge in crude oil prices above $115 per barrel has altered this transmission mechanism by raising inflation expectations and delaying anticipated rate cuts.

We see the energy shock posing a particularly acute challenge for the eurozone, given its heavy reliance on imported energy. This creates a stagflationary scenario that complicates the ECB’s policy outlook, forcing a balance between persistent inflation and weakening growth. Market pricing has shifted accordingly, with we seeing a rising probability of ECB rate increases as early as June, while the Federal Reserve faces its own dilemma as weakening employment data conflicts with inflation pressures stemming from higher energy costs.

From a technical standpoint, EUR/USD has broken decisively below the 200-day, 50-day and 20-day moving averages. The daily RSI near 28 signals deeply oversold conditions, and we expect this could generate a short-term corrective rebound. However, failure to hold the psychological 1.1500 level would risk accelerating losses towards the six-month low near 1.1401. We see the market prioritising inflation risks and safe-haven dollar flows over labour market weakness for now, which is likely to constrain near-term EUR/USD upside despite historically supportive fundamentals for the euro.

USD / JPY

Source: Massive (polygon.io)

USD/JPY has rallied steadily from roughly 157.50 to around 158.90, supported by a combination of geopolitical risk aversion, elevated crude prices above $100 per barrel and a broader stagflationary backdrop complicating the outlook for both the Federal Reserve and the Bank of Japan. The latest US labour data highlighted a sharp deterioration, with employment contracting by 92,000 and the unemployment rate rising to 4.4%, reinforcing evidence of growing economic headwinds.

Under normal circumstances, we would expect weaker labour data to encourage expectations of Federal Reserve easing and weigh on the dollar. However, we see the persistence of elevated energy prices altering this dynamic, as markets reassess the inflation-growth trade-off. As a result, expectations for a June rate cut have actually declined as policymakers appear more cautious about easing into a supply-driven inflation shock.

On the Japanese side, stronger wage growth of 3.0% year-on-year and improving real wages continue to support expectations of eventual Bank of Japan normalisation. Nevertheless, policymakers have signalled reluctance to tighten aggressively against supply-driven inflation pressures, leaving the yen vulnerable despite improving domestic fundamentals.

Technically, USD/JPY is approaching resistance near 159, the yearly high reached in mid-January. The daily RSI around 66 indicates firm momentum without yet entering overbought territory. We expect the support cluster formed by the 20-day and 50-day moving averages and the VWAP near 156 to provide a clear downside reference point. Looking ahead, we see the pair’s trajectory remaining highly sensitive to further labour data, Federal Reserve communication regarding policy in a stagflationary environment and any shifts in Middle Eastern geopolitical risk that could either sustain or reverse the current dollar strength.

GBP / USD

Source: Massive (polygon.io)

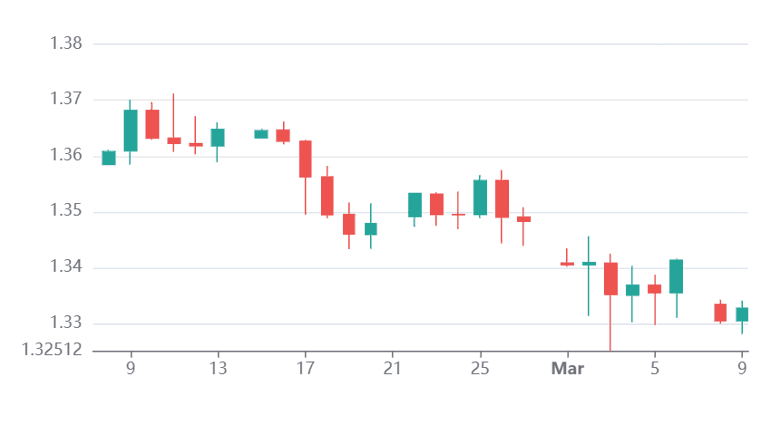

GBP/USD has weakened following the latest US labour market data, with the February nonfarm payrolls report revealing a contraction of 92,000 jobs against expectations of a 59,000 increase and unemployment rising to 4.4%. Normally, we would expect such labour weakness to weigh on the dollar by reinforcing expectations of Federal Reserve easing. However, the simultaneous surge in oil prices above $100 per barrel has instead reinforced dollar strength by creating a stagflationary policy dilemma and pushing June hold probabilities above 51%.

The pair has fallen roughly 0.7% and has now broken below key technical levels, including the 200-day moving average near 1.34 and the cluster of the 50-day and 20-day moving averages around 1.35, as well as the 30-day VWAP. The daily RSI near 35 signals pronounced bearish momentum. We see immediate support around the 1.3280 region, with continued dollar strength potentially exposing the 1.3250 area. Any meaningful recovery would first require a move back above 1.34 and ultimately the 1.35 resistance cluster.

Sterling also faces additional structural challenges. As a net energy importer, the UK is particularly exposed to oil-driven stagflationary pressures, while the Bank of England faces its own policy dilemma as expectations for further rate cuts have declined to around a 40% probability. We expect the combination of persistent geopolitical risk, elevated energy prices and safe-haven dollar demand to keep GBP/USD under pressure in the near to medium term, with the outlook heavily dependent on whether oil prices remain above the $100 threshold and how the Federal Reserve responds to weakening labour conditions amid rising inflation risks.

Economic Calendar