EUR / USD

EUR/USD is navigating a complex macro backdrop where the February nonfarm payroll report, showing a contraction of 92,000 jobs against expectations for a gain of around 55,000 and unemployment rising to 4.4%, would ordinarily weaken the dollar and support the euro. However, we see surging energy prices linked to escalating Middle East tensions fundamentally altering this transmission mechanism. The spike in crude above $100 per barrel has reinforced a stagflation narrative, which we expect to disproportionately weigh on the eurozone given its reliance on imported energy, thereby sustaining dollar strength despite labour market deterioration in the United States.

Technically, EUR/USD is trading near 1.1633 after staging an intraday rebound from the 1.1548 low, though the pair remains below key trend indicators, including the 200-day and 20-day SMAs around 1.17. We see this as confirming a broadly bearish technical structure. At the same time, widening policy divergence has re-emerged, with markets increasingly pricing the possibility of multiple ECB rate increases by year-end to address energy-driven inflation pressures.

Looking ahead, we expect the pair’s direction to depend heavily on incoming US CPI data. If inflation readings reinforce stagflation concerns, the dollar’s safe-haven premium may remain intact. Conversely, if labour market weakness becomes the dominant narrative, we could see renewed downside pressure on the dollar. Any meaningful de-escalation in Middle Eastern tensions could also ease energy market stress and allow EUR/USD to recover towards the 1.17 resistance area. However, absent such developments, we see the euro’s energy vulnerability and bearish technical posture likely to keep the pair under pressure.

USD / JPY

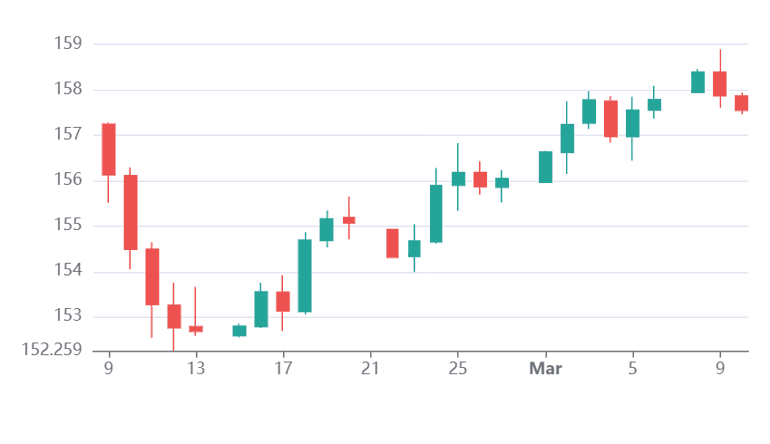

Source: Massive (polygon.io)

USD/JPY has remained elevated despite the sharp deterioration in US labour data, as geopolitical tensions and the surge in crude prices have redirected flows towards the dollar. The February nonfarm payroll report revealed a contraction of 92,000 jobs versus expectations for growth, with unemployment rising to 4.4%. Ordinarily, we would expect such weakness to accelerate expectations of Federal Reserve rate cuts. Instead, we see markets focusing on the inflationary implications of higher energy prices, which has delayed anticipated Fed easing and supported the dollar.

Japan’s exposure to rising oil costs further complicates the picture. With roughly 95% of its crude imports sourced from the Middle East, higher energy prices significantly increase import costs and inflation pressures. We see this dynamic making it more difficult for the Bank of Japan to normalise policy aggressively despite solid domestic growth and improving wage dynamics.

Technically, USD/JPY is trading around 157.6, comfortably above the 200-day moving average near 153. The 156 area forms a key support cluster where the 20-day SMA, 50-day SMA and 30-day VWAP converge. We expect this zone to remain an important pivot for near-term direction. The late-session sell-off and close below the session average suggest some downside pressure emerging, though the broader trajectory will likely depend on whether stagflation fears continue to dominate market pricing or whether recession concerns eventually trigger a faster Federal Reserve easing cycle. In the latter case, we would expect the yen to appreciate more meaningfully.

GBP / USD

Source: Massive (polygon.io)

GBP/USD has been influenced by the same competing macro forces shaping the broader FX complex. February’s nonfarm payroll report revealed a sharp contraction of 92,000 jobs against expectations for a 55,000 increase, with unemployment rising to 4.4%. Under normal conditions, we would expect such labour market weakness to undermine the dollar and support sterling. However, we see the surge in oil prices above $100 per barrel, driven by geopolitical tensions in the Middle East, generating a powerful safe-haven bid for the dollar and offsetting the labour-driven downside pressure.

At the same time, we see the UK policy outlook evolving rapidly. Swap markets have shifted from expecting multiple Bank of England rate cuts to assigning roughly a 70% probability of a rate increase by year-end. This hawkish repricing has provided structural support to sterling. However, the UK’s status as a net energy importer means persistently high oil prices could quickly undermine domestic demand and limit sterling’s upside.

Technically, GBP/USD is trading near 1.3448 after rebounding from the 200-day SMA around 1.34. Resistance remains clustered near 1.35, where the 20-day and 50-day SMAs and the 30-day VWAP converge. We expect near-term direction to depend less on the payroll report alone and more on whether upcoming US CPI and UK GDP releases reinforce inflation persistence or signal emerging demand destruction. This distinction will likely determine whether GBP/USD can move beyond its current 1.32–1.34 consolidation range or remain constrained by the competing forces shaping the macro outlook.