EUR / USD

EUR/USD weakened, shedding approximately 4.1% from its February highs to current levels near 1.1415, driven by persistent safe-haven dollar demand amid Strait of Hormuz disruptions and broader risk-off capital flows. The pair now trades decisively below all key moving averages—including the 200-day SMA at 1.1677, the 50-day SMA at 1.1739—while the daily RSI has plunged to approximately 27, signalling deeply oversold conditions that suggest the selloff may be approaching exhaustion.

Fundamentally, Eurozone structural deterioration, driven by weakening current account dynamics, presents a persistent headwind for the euro, even as purchasing power parity models indicate valuation support at current levels. Back-to-back Federal Reserve and European Central Bank policy meetings this week represent the primary catalyst for diversion, with both central banks confronting a dual mandate conflict between elevated energy-driven inflation pressures and weakening growth—a policy paralysis that historically precedes significant currency repricing. Forward guidance on inflation persistence and rate-cut timing will prove as consequential as the decisions themselves, with hawkish ECB tones or dovish Fed surprises capable of triggering 150–200 basis-point moves within 10 days.

From a technical perspective, a bullish mean-reversion scenario could see a bounce toward the 1.1480–1.1500 zone. Resolution of the current consolidation range appears imminent, given the dual central bank meeting, though institutional EUR long positioning in the 65–70th percentile creates additional technical fragility if disappointing policy messaging triggers unwinding flows.

USD / JPY

Source: Massive (polygon.io)

USD/JPY continues to grind higher within a persistent uptrend, climbing to 159.71 and trading well above all key moving averages, reflecting the fundamental backdrop of monetary policy divergence between the Federal Reserve and the Bank of Japan. The pair's advance is underpinned by diminished expectations for Fed rate cuts, with money markets pricing only a 90% probability of a single 25bps reduction by year-end, while elevated oil prices further weigh on Japan's energy-import-dependent economy and bolster the dollar's relative appeal.

This week's back-to-back central bank decisions represent a critical inflection point: the Fed's March 18 meeting is expected to hold rates steady, but Jerome Powell's commentary on inflation amid commodity price shocks will shape yield expectations, while the BOJ's March 19 announcement must balance growth support against imported inflation pressures, with markets pricing a 90% probability of two BOJ rate increases by December. Should the Fed signal extended rate maintenance while the BOJ emphasises only gradual normalisation, the widening policy trajectory gap would reinforce the bullish case for USD/JPY toward the psychologically significant 160 handle and potentially the all-time high near 162.

However, caution is warranted, as the daily RSI has pushed above 71, firmly into overbought territory, raising the risk of a mean-reversion pullback toward initial support at the 20-day SMA near 157. Geopolitical uncertainty stemming from Middle East tensions continues to drive safe-haven flows and amplify currency volatility, with foreign institutional investors persistently selling risk assets. While stretched technical conditions coincide with the critical 160 level intervention threshold, market attention will be on divergent central bank signals, and geopolitical risk will ultimately determine whether USD/JPY sustains its uptrend or enters a corrective phase in the sessions ahead.

GBP / USD

Source: Massive (polygon.io)

GBP/USD has come under significant pressure, dropping roughly 0.9% over the past week to close near 1.3222, driven by a confluence of macroeconomic headwinds and safe-haven dollar demand stemming from the escalating Iran conflict and its disruption to global energy supplies. The pair now trades decisively below all key moving averages, confirming a bearish technical posture that aligns with the deteriorating fundamental backdrop for sterling.

The Bank of England faces a particularly difficult policy dilemma: surging crude prices threaten to push UK inflation to more than double the 2% target, yet the economy has already shown signs of softness, with an unexpected contraction in January output. This stagflationary environment is mirrored by constrained Fed policy, with markets pricing in substantially fewer rate cuts in 2026, limiting any relative yield advantage for the pound and reinforcing broad dollar strength. The transatlantic divergence in monetary expectations, with both central banks reluctant to ease, ultimately favours the dollar given its safe-haven status during geopolitical uncertainty.

From a technical perspective, the daily RSI has fallen to approximately 33, indicating deeply oversold conditions that could trigger a mean-reversion bounce toward the 200-day SMA near 1.34 if buyers defend the 1.3220 support area. However, the decisive break beneath all major moving averages raises the risk of a broader downtrend continuation toward 1.3150 and potentially the November lows near 1.3015 should bearish momentum accelerate. This week's Bank of England and Federal Reserve policy decisions will be pivotal in determining whether sterling can stabilise or whether the fundamental and technical alignment continues to pressure the pair lower.

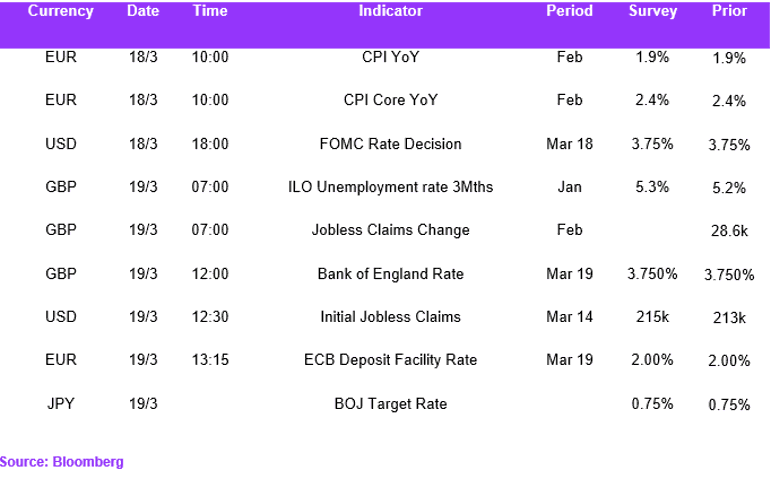

Economic Calendar