EUR / USD

Source: Massive (polygon.io)

EUR/USD rebounded strongly yesterday on dollar weakness, pushing the pair back to 1.1500. A number of central banks' meetings are taking place this week, and while no rate changes are expected from either the ECB or the Fed, the minutes and post-meeting commentary will be closely watched. Policymakers are likely to take a more cautious approach to oil and inflation narratives, as little time has passed to indicate any conclusive decisions. Still, any divergence in language between central banks may add volatility to the pair’s price discovery as investors reprice in light of new interest rate dynamics.

In particular, the risks for central banks mount in the medium term should the conflict persist. The ECB is caught in a stagflationary bind: energy-driven inflation has pushed rate-hike expectations to 85% by July, yet tightening into slowing growth risks further economic damage, paradoxically weakening rather than supporting the currency. The Federal Reserve's relative insulation from direct energy shock transmission allows it to maintain yield support, attracting safe-haven capital flows into dollar-denominated assets and reinforcing the divergence.

From a technical standpoint, the pair is trading near 1.1480, well below the 200-day SMA at 1.1670, the 50-day SMA at 1.1736, confirming the entrenched bearish trend that has driven a roughly 2.9% decline over the past month. The daily RSI near 37 signals oversold momentum without reaching extreme levels, while primary support sits in the 1.1355–1.1415 zone, aligning with Fibonacci retracement levels and recent price action lows. The support of 1.14 appears well-anchored, given that energy dynamics and terms-of-trade deterioration will likely continue dominating rate differential considerations until Strait of Hormuz supply normalisation occurs - a timeline extending well beyond near-term ECB guidance this Thursday.

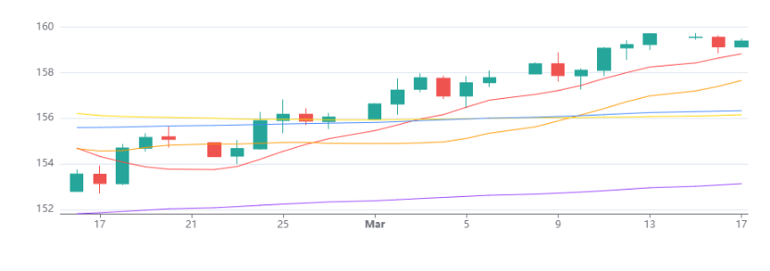

USD / JPY

Source: Massive (polygon.io)

USD/JPY remains firmly entrenched in a bullish posture, trading near 159.40 and well above all key moving averages, underscoring the strength of the prevailing uptrend. Interest rate differentials have reasserted themselves as the dominant driver, with correlations between the pair and US Treasury yields reaching 90% as markets unwind Federal Reserve rate cut expectations, pushing US yields higher and widening the spread favouring the dollar. Japan's acute dependence on imported energy - approximately 95% of its crude supplies - has compounded yen weakness as surging oil prices deteriorate the current account and amplify structural headwinds.

The Bank of Japan faces a difficult policy dilemma, with Governor Ueda noting gradual progress toward the 2% inflation target but market pricing suggesting only a 60% probability of an April rate hike, limiting any hawkish catalyst for yen recovery. Meanwhile, Japanese authorities have escalated verbal intervention signals, though analysts view the intervention bar as elevated, given the fundamental legitimacy of the dollar's strength driven by energy supply concerns and rate differentials.

From a technical perspective, the daily RSI at approximately 65 indicates positive momentum approaching overbought territory, with a break above 159.70 opening the path toward the psychologically significant 160 level. The duration of elevated energy prices will prove critical to the pair's trajectory, as sustained import cost pressures would reinforce yen weakness. Markets are likely to cautiously approach the 160 level in the meantime, as fears of intervention are likely to keep a psychological lid on prices.

GBP / USD

Source: Massive (polygon.io)

GBP/USD is trading near 1.3288, remaining firmly below all key moving averages and reflecting a persistent longer-term bearish structure that has defined the broader downtrend from the late-January high near 1.3848. The daily RSI, hovering around 37, indicates subdued but not yet oversold momentum, suggesting the recent decline may be entering a stabilisation phase rather than accelerating further.

The pound faces persistent headwinds, with elevated oil prices creating inflationary pressures that complicate the Bank of England's policy path, as energy-driven inflation threatens to derail disinflationary progress. Defensive dollar positioning remains a dominant driver, with the greenback strengthening as a safe-haven asset amid Middle Eastern geopolitical turbulence, while market repricing has shifted rate-cut expectations materially, with participants now pricing a minimal probability of the Federal Reserve easing through the first half of 2026.

On the technical front, a bullish scenario requires the price to reclaim the 100-day SMA around 1.34 and push toward the 1.35 cluster on improving sentiment, whereas a bearish breakdown below support at 1.3279 could accelerate selling toward the mid-March low near 1.3222. The pound's structural position within global capital flows has deteriorated as risk sentiment remains fragile, with downside pressure likely to persist absent meaningful geopolitical de-escalation or clear evidence that energy-driven inflation proves temporary.