EUR / USD

Source: Massive (polygon.io)

EUR/USD has staged a notable rebound, with we seeing a sharp rally on 19 March of around 1.3%, lifting the pair from 1.1471 to a peak near 1.1616. This move has been driven primarily by a repricing of interest rate differentials, as markets respond to the European Central Bank’s increasingly hawkish stance in the face of crude oil prices rising above $119 per barrel. We see markets now pricing potential ECB rate hikes as early as April or June 2026, while the Federal Reserve maintains a “higher-for-longer” approach with no easing expected until 2027. The rise in German two-year yields — up 56 basis points in March — reflects this shift and has supported euro demand.

However, from a technical perspective, we expect significant resistance overhead. The 200-day and 50-day moving averages, along with the 30-day VWAP, converge near 1.1700, while the 20-day SMA around 1.1600 has already begun to cap gains. The subsequent pullback towards 1.1560 suggests fading momentum following the initial rally. We expect a sustained break above 1.1600 to be required to open the path towards the 1.1700 resistance cluster.

Looking ahead, we see oil price dynamics as the key transmission channel for EUR/USD. Continued disruption around the Strait of Hormuz would maintain upward pressure on inflation in the eurozone, reinforcing the ECB’s hawkish bias. At the same time, geopolitical risk continues to support safe-haven demand for the dollar. We expect this tension between narrowing rate differentials and risk-driven dollar demand to keep EUR/USD volatile, with the 1.1440–1.1700 range defining the near-term battleground.

USD / JPY

Source: Massive (polygon.io)

USD/JPY is approaching a critical inflection point, with we seeing a recent sharp pullback from near 160 to around 157.5 as markets reassess the near-term outlook. The Bank of Japan’s increasingly hawkish tone — with Governor Ueda signalling the possibility of rate hikes as early as April — contrasts with the Federal Reserve’s more cautious stance, contributing to a gradual narrowing of interest rate differentials that would typically support yen strength.

However, we see the broader macro backdrop complicating this dynamic. Elevated oil prices and ongoing Middle East tensions pose a particular challenge for Japan, given its heavy reliance on imported energy. This introduces cost-push inflation that limits the effectiveness of monetary tightening, as rate hikes would do little to address supply-driven pressures while potentially weighing on growth.

Technically, the pair is trading near 158.4, just above the 20-day SMA around 158, with RSI moderating to approximately 52 following earlier elevated readings. Support is layered at the 30-day VWAP near 157 and the 50-day SMA around 156, while resistance at 159 remains a key level where selling pressure previously emerged. We expect the 157–159 range to act as a near-term pivot, with direction dependent on incoming policy signals and geopolitical developments.

We also expect intervention risk to remain elevated as the pair approaches the 160 level, with Japanese authorities likely to increase verbal or direct action to stabilise the currency. The balance between narrowing rate differentials and energy-driven inflation risks will be key in shaping USD/JPY’s next move.

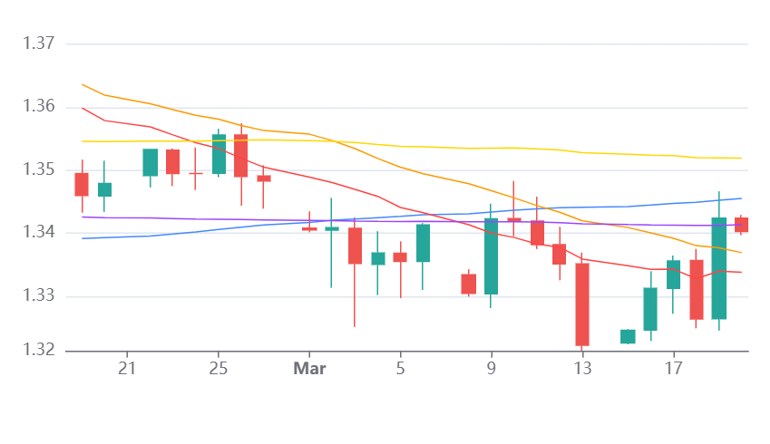

GBP / USD

Source: Massive (polygon.io)

GBP/USD is trading at a critical juncture, shaped by diverging central bank expectations and key technical levels converging around current prices. We see the Bank of England’s unanimous decision to hold rates at 3.75%, accompanied by a more hawkish tone, as a significant shift in market expectations. Markets are now pricing close to three rate hikes by year-end, compared with only a single Federal Reserve cut expected in 2026. This widening policy gap, reflected in a sharp 88 basis point rise in two-year gilt yields month-to-date, has provided fundamental support for sterling.

Technically, the pair is holding near the 1.3400 level, which represents a key confluence of the 200-day moving average, the 30-day VWAP and the 20-day SMA. The RSI has recovered to around 51 from previously weaker levels, suggesting stabilising momentum. We expect that a sustained hold above 1.3400 could allow a move towards the 50-day SMA near 1.3500 and the 1.3550 resistance zone. Conversely, failure to maintain this support would likely expose the mid-March low near 1.3220.

However, we see the broader macro environment continuing to cap sterling upside. Elevated energy prices and persistent geopolitical uncertainty are reinforcing risk-off sentiment, driving flows into the dollar as the preferred safe-haven asset. We expect the key tension for GBP/USD to remain between supportive rate differentials favouring sterling and the overriding influence of global risk dynamics, which continue to limit upside potential in the near term.