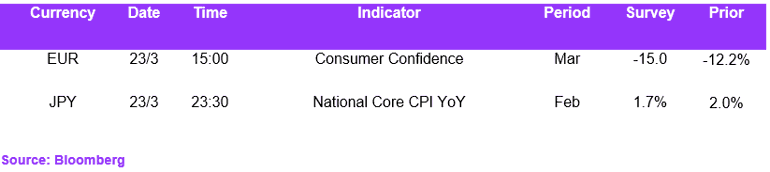

EUR / USD

Source: Massive (polygon.io)

EUR/USD remains under sustained pressure, and we see the dominant driver as the energy shock stemming from the US–Israel–Iran conflict, which disproportionately impacts the eurozone. With Brent crude holding above $100 per barrel, we expect the eurozone to face a worsening stagflationary backdrop, where rising inflation coincides with deteriorating growth. This places the ECB in a difficult position, as it may be forced to consider tightening even as activity weakens. By contrast, the United States continues to benefit from its status as a net energy exporter, with we seeing ongoing support for the dollar through both safe-haven flows and energy-related demand.

Positioning dynamics reinforce this view, with we seeing speculative accounts moving closer to net-short EUR exposure, while asset managers have increased bullish dollar positioning to one-year highs.

Technically, EUR/USD continues to grind lower, trading around 1.1526 and remaining firmly below all key resistance levels, including the 200-day and 50-day SMAs near 1.17 and the 30-day VWAP and 20-day SMA near 1.16. The RSI near 43 reflects persistent bearish momentum. We expect the near-term path to remain biased to the downside, with a move through 1.1520 likely to expose the March low near 1.1415.

Looking ahead, we expect this week’s data to be critical. Flash PMIs on Tuesday and eurozone consumer confidence will provide a timely read on how severely the energy shock is feeding into activity, particularly in manufacturing. We expect these releases to confirm further softness. Unless geopolitical tensions ease materially or energy prices retrace, we see limited scope for a sustained EUR/USD recovery.

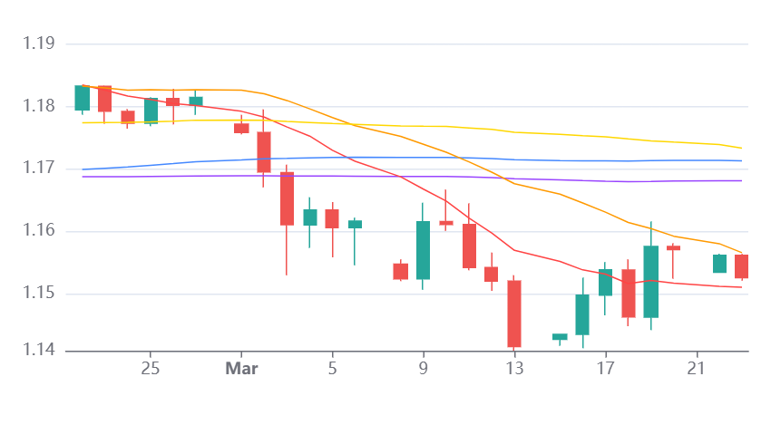

USD / JPY

Source: Massive (polygon.io)

USD/JPY remains under strong upward pressure, with we seeing the pair advancing towards the critical 160 level, currently trading near 159.6. The rally continues to be driven by a clear macro divergence: elevated oil prices and geopolitical tensions are supporting the dollar while weighing heavily on Japan as a major energy importer. At the same time, safe-haven demand continues to favour the dollar.

We expect intervention risk to increase materially at current levels, particularly as Japanese officials have reiterated their readiness to respond to excessive currency volatility. This introduces meaningful two-way risk despite the prevailing uptrend.

From a technical perspective, USD/JPY remains firmly above all key moving averages, including the 200-day SMA near 153, the 50-day SMA at 156 and the 20-day SMA near 158.5, confirming strong bullish momentum. The RSI around 60 suggests there is still room for further upside. We expect a break above 159.60 to open the path towards 160 and potentially a retest of the 162 high, although rejection at these levels could trigger a pullback towards support near 158.5.

On the policy side, we see the Bank of Japan’s hawkish rhetoric, including calls for further tightening, as insufficient to offset the widening US–Japan rate differential, particularly as markets have repriced away from Fed cuts and are increasingly considering the risk of further tightening.

Looking ahead, we expect today’s US CPI release to be a key catalyst, particularly in shaping Fed expectations in a stagflationary environment. In addition, flash PMIs, Japanese inflation data and wage negotiations will be closely watched. We expect these data points to determine whether the BoJ can credibly advance its tightening path or whether USD/JPY continues to be driven higher by rate differentials and energy dynamics.

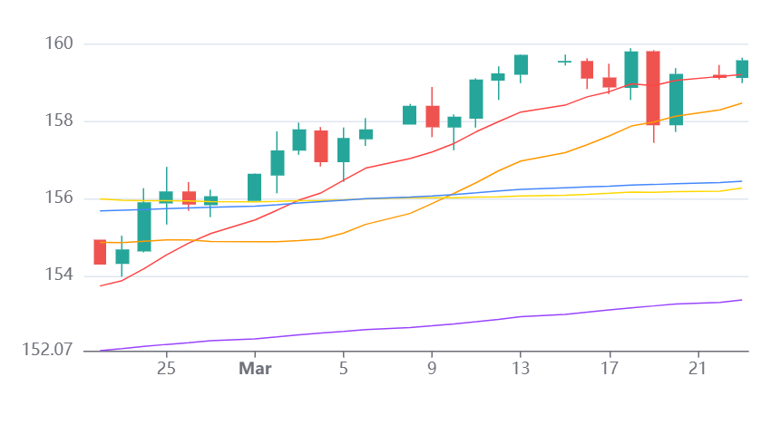

GBP / USD

Source: Massive (polygon.io)

GBP/USD continues to face a challenging outlook, with we seeing a combination of structural and cyclical headwinds weighing on sterling. The energy shock linked to Middle East tensions is particularly negative for the UK as a net energy importer, while the United States benefits from energy independence and safe-haven demand for the dollar.

We expect UK inflation, currently around 3%, to rise further towards 3.5% as higher energy prices feed through into the broader economy. This creates a stagflationary backdrop that limits the Bank of England’s policy flexibility and undermines sterling’s relative attractiveness.

Technically, the pair remains under pressure, trading below all key moving averages, including the 20-day SMA near 1.33, the 200-day SMA near 1.34 and the 50-day SMA near 1.35. The RSI around 43 suggests ongoing bearish momentum with scope for further downside. We expect the 1.3220 level to act as a key near-term support, with a break likely to open the path towards the low 1.31s.

Positioning data confirm the bearish bias, with we seeing increased speculative short positioning in GBP/USD alongside stronger dollar demand.

Looking ahead, we expect this week’s data to play a decisive role. Flash PMIs on Tuesday and UK CPI on Wednesday will provide critical insight into the balance between inflation persistence and demand weakness. We see risks skewed towards further downside in GBP/USD, particularly if inflation surprises to the upside or activity indicators deteriorate further.

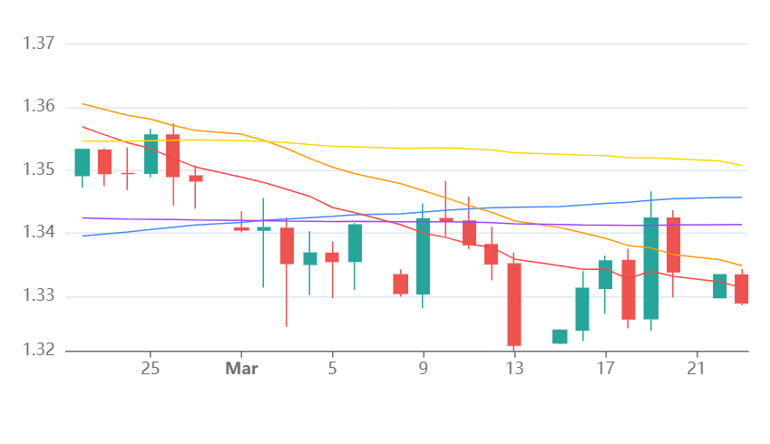

Economic Calendar