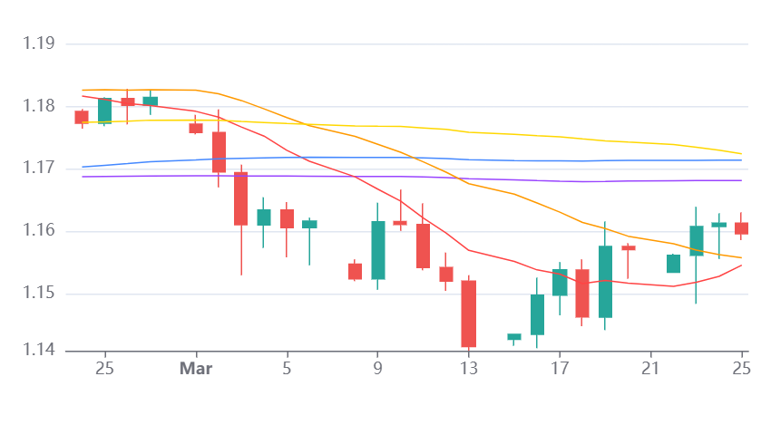

EUR / USD

Source: Massive (polygon.io)

EUR/USD is trading near 1.1597, and we see the pair firmly caught in a tug-of-war between competing macro forces, with geopolitical developments remaining the dominant driver. Fluctuating expectations around the U.S.–Iran conflict continue to drive volatility in energy markets and risk sentiment, and we expect this to maintain asymmetric pressure on the eurozone relative to the United States. Europe’s reliance on imported energy leaves it significantly more exposed, and we see this increasingly reflected in softer activity data, with the composite PMI slipping to 50.5 alongside elevated input cost pressures.

By contrast, we see the US economy showing greater resilience, with PMI data holding in expansionary territory at 51.4. This divergence reinforces the underlying imbalance, even as weakening US data and a softer dollar index below 100 provide some offset.

On monetary policy, we see growing complexity. Markets are increasingly pricing ECB tightening risk, with around a 65% probability of a hike at the April meeting, driven by energy-led inflation, while the Fed remains broadly on hold despite a gradual repricing of upside rate risks. We expect this evolving dynamic to limit directional conviction in the near term.

Technically, EUR/USD remains capped below the key 1.17 resistance cluster, with RSI recovering to a neutral 49 after prior oversold conditions. We expect a break above 1.1630 to open the path towards 1.1680, though failure at resistance would likely see a move back towards 1.1420. Overall, we see continued range-bound trading with a modest downside bias, as eurozone vulnerabilities and safe-haven dollar demand continue to cap rallies.

USD / JPY

Source: Massive (polygon.io)

USD/JPY remains in a complex and highly reactive environment, and we see the pair driven by the interaction between central bank divergence and geopolitical risk. The Bank of Japan is gradually strengthening its case for further tightening, supported by sustained wage growth and firm underlying inflation, with markets pricing around a 60% probability of a rate hike in April.

However, we see this yen-supportive narrative being offset by developments in the United States. The Federal Reserve remains on hold, but rising inflation expectations , amplified by elevated oil prices, have led to a sharp repricing of rate expectations, with markets increasingly assigning probability to further tightening later in the year. This has helped sustain the dollar and preserve the rate differential.

From a technical perspective, the pair remains well supported above the 158–159 zone, where the 20-day SMA and 30-day VWAP converge. The RSI near 56 suggests momentum has moderated but remains constructive. We expect that holding above this support area would allow a retest of the 160 level and potentially a move towards 162. Conversely, a break below 158.40 would expose the 50-day SMA near 156.

Looking ahead, we expect geopolitical developments to remain the dominant driver. A de-escalation in the Middle East would likely weaken the dollar and support yen appreciation, particularly if it accelerates BOJ tightening expectations. However, if tensions persist and energy prices remain elevated, we expect USD/JPY to stay biased higher, with intervention risk increasing materially as the pair approaches 160.

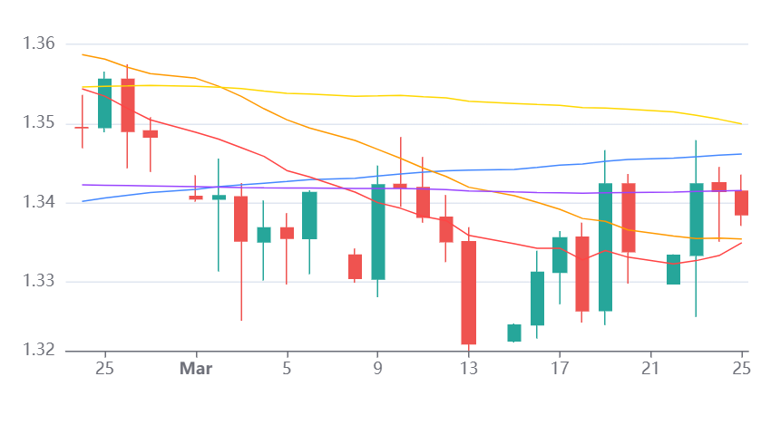

GBP / USD

Source: Massive (polygon.io)

GBP/USD is trading in a narrow and technically indecisive range around 1.338–1.341, and we see the pair at a key inflection point. The convergence of the 200-day SMA, 20-day SMA and 30-day VWAP near 1.340 is acting as a pivot, while resistance at the 50-day SMA near 1.350 continues to cap upside. The RSI near 49 reflects a lack of clear directional momentum following the pullback from the 1.370 area.

From a macro perspective, we see sterling facing a particularly challenging environment. The UK’s exposure to higher energy prices, driven by the ongoing Middle East conflict, is amplifying stagflationary risks, with activity indicators weakening and input costs rising sharply. This places the Bank of England in a difficult position, with markets now pricing multiple rate hikes despite deteriorating growth, a dynamic that we see as increasingly negative for the currency.

At the same time, we see gilt yields rising sharply, with 10-year yields at levels not seen since 2008. However, rather than supporting sterling, we expect this to reflect growing concerns around fiscal sustainability and risk premium, limiting any positive impact from higher yields.

On the US side, we see the dollar continuing to benefit from safe-haven demand and relatively stronger economic conditions, while the near-zero rate differential between the BoE and Fed leaves GBP/USD highly sensitive to shifts in expectations.