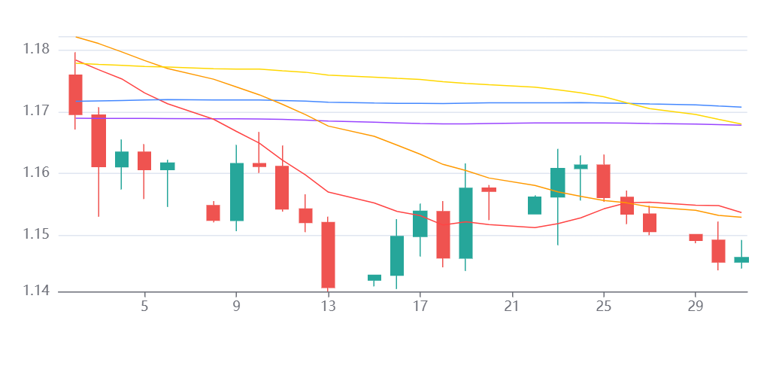

EUR / USD

Source: Massive (polygon.io)

EUR/USD is closing March 2026 with a near three percent monthly decline, and we see the move driven primarily by the geopolitical fallout from the US Israel conflict with Iran and the effective closure of the Strait of Hormuz. The resulting surge in Brent crude above 113 dollars per barrel has created a stagflationary shock that disproportionately impacts the eurozone, where we expect growth to weaken further even as inflation accelerates. This leaves the ECB in a difficult position, as rising prices limit policy flexibility while economic activity continues to deteriorate.

At the same time, we see the Federal Reserve maintaining a relatively firm stance, holding rates in the 3.50 to 3.75 percent range, while markets have repriced away from rate cuts this year. This has widened the policy divergence and reinforced dollar strength through both safe haven demand and positioning flows.

From a technical perspective, the pair is trading near 1.1464 and remains firmly below all key moving averages clustered around 1.16 to 1.17. The RSI near 38 confirms sustained bearish momentum. We expect that failure to reclaim the 1.15 area would leave the pair vulnerable to further downside towards 1.1421, while any recovery would likely struggle against strong resistance above.

Looking ahead, we see EUR/USD direction as highly dependent on geopolitical developments. A credible ceasefire and reopening of energy routes could trigger a sharp reversal higher, particularly if inflation data confirms peak pressures. However, in the absence of de escalation, we expect the broader bearish trend to remain intact.

USD/JPY

Source: Massive (polygon.io)

USD/JPY is consolidating at elevated levels near 159.60, and we see the pair caught between strong structural support and rising intervention risk. The dominant driver remains policy divergence, with the Federal Reserve maintaining a restrictive stance while the Bank of Japan continues to move only gradually towards normalisation.

We see this divergence reinforced by energy dynamics. Elevated oil prices continue to weigh on Japan as a major importer, weakening the yen and supporting the dollar. At the same time, we expect carry trade demand to remain a key factor, given the still wide yield differential between US Treasuries and Japanese government bonds.

From a technical perspective, the pair remains above all key moving averages, with support near 159.20 and 158.35, while resistance is building just below 160 and towards 162. The RSI near 57 suggests momentum is moderating, indicating a potential consolidation phase.

However, we also see growing risks of a sharp reversal. Intervention rhetoric has intensified, and we expect authorities to act more decisively if the pair moves sustainably above 160. Looking ahead, we expect USD/JPY to remain highly sensitive to developments in energy markets, the Bank of Japan policy outlook, and any signs of official intervention.

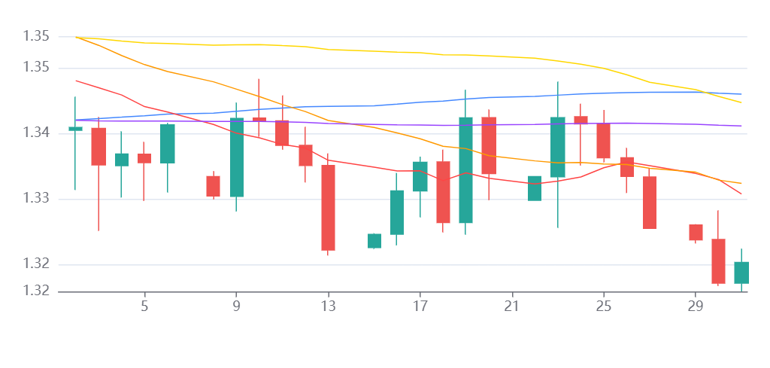

GBP / USD

Source: Massive (polygon.io)

GBP/USD is ending March under sustained pressure, with we seeing a decline of over two percent for the month as sterling underperforms against a broadly stronger dollar. The pair is trading near 1.3201 and remains below all major moving averages around 1.34, with the RSI near 39 indicating persistent bearish momentum.

We see the macro backdrop as particularly challenging for the UK. The sharp rise in energy prices is feeding directly into inflation while weighing on growth, creating a stagflationary environment that constrains the Bank of England. Markets have shifted from expecting rate cuts to pricing multiple hikes, but we see this as a negative signal, reflecting economic stress rather than strength.

At the same time, we see the dollar continuing to benefit from safe haven demand and a more stable macro outlook. This combination is likely to keep pressure on sterling in the near term.

Technically, we expect the 1.3160 level to act as key support, with a break below opening the path towards 1.3015. While a geopolitical de escalation could support a recovery, we expect any upside to be limited unless energy prices fall meaningfully and policy uncertainty eases.