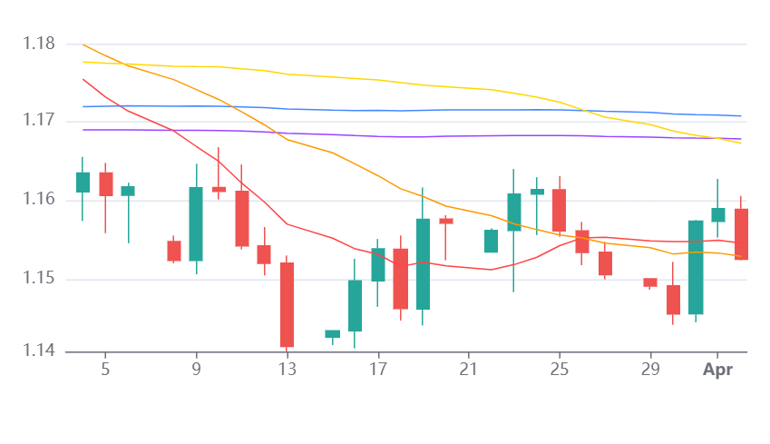

EUR / USD

Source: Massive (polygon.io)

EUR/USD remains under significant bearish pressure in early April 2026, and we see the macro backdrop continuing to favour the dollar as the US Iran conflict amplifies structural divergence between the two economies. Europe’s heavy reliance on imported energy leaves it acutely exposed to supply disruptions, while we see the United States benefiting from relative energy independence, reinforcing a widening growth and inflation gap.

We expect the European Central Bank to remain constrained by a stagflationary mix of weak growth and rising inflation, limiting its ability to respond decisively, while the Federal Reserve’s steady policy stance continues to underpin the dollar through a persistent yield advantage. This divergence, alongside ongoing capital outflows from European assets, suggests the broader trend remains tilted to the downside.

From a technical perspective, we see clear confirmation of bearish momentum, with the pair trading below all key moving averages clustered near 1.17. The move lower toward 1.1526 on strong volume reinforces conviction in the trend. We expect that a break below the 1.15 level would accelerate losses toward 1.1415, while any recovery toward the 1.158 to 1.160 zone is likely to be corrective unless the geopolitical backdrop shifts materially.

USD / JPY

Source: Massive (polygon.io)

USD/JPY remains elevated near 159.44, and we see the pair continuing to be driven primarily by yield differentials and energy driven macro dynamics. The dollar retains strong support from higher US yields and resilient inflation, while the yen remains structurally pressured by Japan’s energy import exposure.

We expect intervention risk to increase as the pair approaches the 160 level, which remains both a psychological and policy sensitive threshold. At the same time, we see growing expectations for Bank of Japan tightening, supported by firm wage growth and improving domestic data, though this has yet to materially narrow the yield gap.

Technically, we see the pair holding above the 20 day moving average near 159, maintaining a constructive bias. However, with momentum moderating, we expect a more volatile range to develop. A break above 160 could open the path toward the cycle highs, while a move below 159 would likely expose support near 157. Looking ahead, we expect US labour market data to be the key catalyst in determining whether yield support for the dollar remains intact.

GBP / USD

Source: Massive (polygon.io)

GBP/USD remains under sustained bearish pressure, and we see the pound continuing to struggle against a combination of geopolitical risk, domestic weakness, and widening policy divergence. The UK economy appears particularly vulnerable to the energy shock, and we expect stagflationary pressures to intensify as higher oil prices feed through to inflation and growth.

We see the Bank of England facing a difficult policy trade off, with limited room to tighten despite elevated inflation, while the Federal Reserve’s firmer stance continues to support the dollar. This divergence, alongside fragile UK growth dynamics, reinforces a negative outlook for sterling.

From a technical perspective, we see the pair firmly below key resistance around 1.34, with momentum remaining weak. The break toward 1.3215 highlights the underlying bearish trend, and we expect that a move below 1.3205 would open the path toward 1.3015. While short term rebounds are possible, we expect these to remain limited unless there is a clear de escalation in geopolitical tensions and a stabilisation in the UK macro outlook.