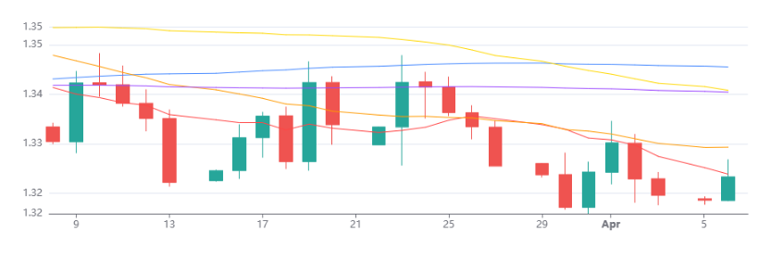

EUR / USD

Source: Massive (polygon.io)

The EUR/USD pair is trading in a precarious position, caught between the dollar's safe-haven strength amid the US-Iran conflict and a narrowing US-German yield differential that has historically supported the euro. The closure of the Strait of Hormuz represents an asymmetric shock to the Eurozone, which, as a major net energy importer, faces accelerating inflation, already at 2.5% in March, and a growing stagflation risk that far exceeds that of the relatively energy-independent US. While the ECB has revised its inflation forecasts higher and markets are beginning to price in potential rate hikes, the Fed's inclination to hold rates elevated for longer continues to provide a fundamental floor for the dollar.

From a technical standpoint, the pair's positioning near 1.1541, well below the cluster of longer-term moving averages around 1.17 and barely clinging to the 20-day SMA at 1.15, confirms the broader bearish structure despite a modestly recovering RSI near 47. The intraday rejection at the 1.157 resistance zone during Monday's session suggests sellers remain firmly in control at higher levels, and a break below the 1.1415 mid-March support could accelerate downside momentum toward the 1.14 handle.

The near-term trajectory hinges on two critical catalysts: the outcome of US-Iran ceasefire negotiations and this week's US CPI release, either of which could trigger sharp moves given the crowded speculative long-euro positioning revealed by CFTC data. On balance, the combination of Europe's disproportionate energy vulnerability, the dollar's geopolitical bid, and the pair's bearish technical posture tilts the risk-reward toward further EUR/USD downside, with any rallies toward the 1.162 zone likely to be met with renewed selling pressure unless a credible ceasefire materialises.

USD / JPY

Source: Massive (polygon.io)

The USD/JPY pair remains elevated near multi-decade highs around 159.7, underpinned by the persistent monetary policy divergence between a restrictive Fed and a still-accommodative Bank of Japan. The upcoming US CPI report is a critical catalyst, as any hotter-than-expected inflation reading could further delay anticipated Fed rate cuts and reinforce the dollar's yield advantage, with the market currently pricing only a 30% probability of a Fed cut this year.

On the Japanese side, the Bank of Japan faces a difficult balancing act; while markets assign roughly a 70% probability to a rate hike at the April 27-28 meeting, Governor Ueda has signalled caution amid heightened geopolitical risks, and surging crude oil prices near $111 per barrel threaten to slow growth in energy-dependent Japan. The escalating US-Iran confrontation is pulling the pair in opposing directions, with the dollar benefiting from safe-haven demand while the yen's own haven status attracts competing repatriation flows.

Technically, the pair is constructively positioned above all major moving averages, with a decisive break above the 160.3 resistance level potentially opening the path toward a retest of the all-time high near 162. However, the psychologically critical 160 level heightens the ever-present risk of Japanese official intervention, as the Ministry of Finance has intensified rhetoric about speculative one-way moves and has historically acted aggressively near these thresholds.

GBP / USD

Source: Massive (polygon.io)

The GBP/USD pair faces significant headwinds amid the ongoing Middle East conflict and the resulting energy shock, which creates a deeply unfavourable macro backdrop for the British pound. The closure of the Strait of Hormuz has driven crude prices above $110 per barrel, disproportionately impacting the energy-import-dependent UK economy, while deteriorating fundamentals reinforce concerns about stagflation. The US dollar, by contrast, continues to benefit from dual tailwinds of safe-haven demand and resilient domestic data, including a stronger-than-expected March payrolls print of 178,000.

Monetary policy divergence adds further complexity, with markets now pricing in two Bank of England rate hikes in 2026 despite Governor Bailey's pushback, while the Federal Reserve faces even more hawkish pressure, with Cleveland Fed President Hammack raising the prospect of rate hikes and inflation projections approaching 3.5%. This environment of restrictive policy on both sides of the Atlantic, combined with persistent geopolitical risk, broadly favours continued dollar strength.

From a technical perspective, GBP/USD remains capped below a formidable cluster of resistance at the 20-day SMA near 1.33, the 50-day SMA at 1.34, and the 200-day SMA at 1.34, with the daily RSI at 44 reflecting subdued momentum within a one-month downtrend of nearly 2%. The 1.3194 support zone, tested twice recently, represents the critical near-term level, and a breach would expose the pair toward the late-March low near 1.3172, which appears the more probable path given the prevailing fundamental and geopolitical headwinds.

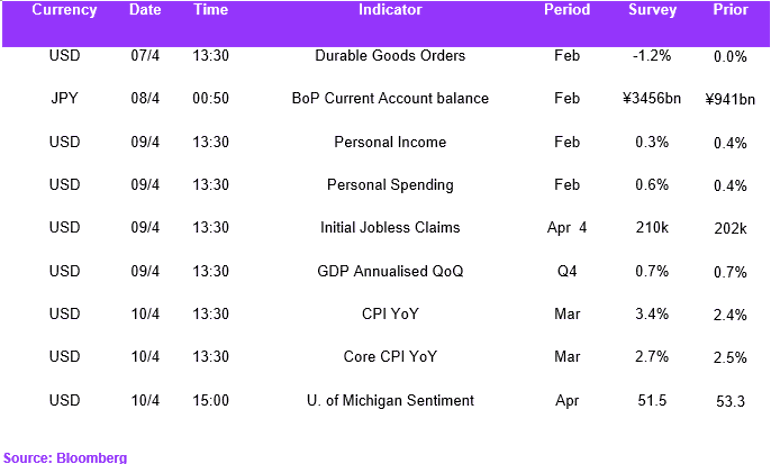

Economic Calendar