EUR / USD

Source: Massive (polygon.io)

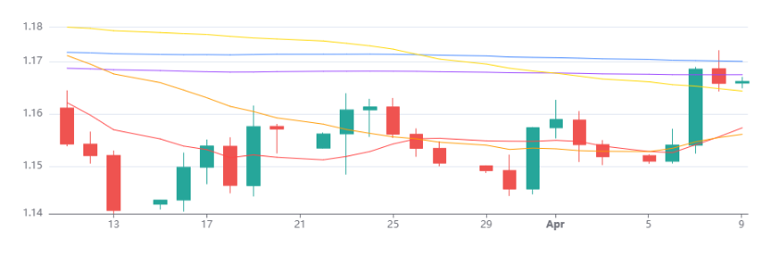

The EUR/USD pair is navigating a highly complex macro environment defined by geopolitical fragility and divergent central bank expectations. The initial unwinding of safe-haven dollar positioning following the US-Iran ceasefire announcement propelled the euro to multi-week highs, but emerging cracks in the truce - particularly the continued closure of the Strait of Hormuz and rebounding oil prices - have introduced significant caution, as reflected in the pair's retreat from its session high near 1.1721 to around 1.1662.

The widening policy divergence between the Federal Reserve and the European Central Bank remains a fundamental headwind for sustained euro strength. With Fed officials signalling a higher-for-longer rate stance and even discussing potential hikes, while ECB expectations have moderated to at most one rate increase this year, the 150-to-175 basis point rate differential continues to favour the dollar. The eurozone's acute vulnerability to energy shocks compounds this challenge, as elevated oil and natural gas prices feed stagflationary pressures, evidenced by inflation accelerating to 2.5% alongside a composite PMI slipping to a nine-month low of 50.7.

From a technical perspective, the pair settled around 1.1662, holding just above the 20-day near 1.1550 but failing to sustain a break above the 200-day SMA at approximately 1.1680, which served as clear overhead resistance. The path forward hinges on whether upcoming US core inflation data and the April 10 US-Iran talks reinforce dollar strength or allow bulls to reclaim the 1.17 level and target the 1.1880 resistance area. In the meantime, technical resistance levels in the form of moving averages are likely to keep the pair’s upside capped.

USD / JPY

Source: Massive (polygon.io)

USD/JPY is navigating a complex macro environment defined by monetary policy divergence, geopolitical uncertainty, and technically neutral-to-bearish short-term positioning. The Federal Reserve's hawkish "higher-for-longer" stance, reinforced by recent FOMC minutes citing sticky services inflation and resilient wage growth, continues to support a substantial interest rate differential in favour of the dollar. However, this is being structurally challenged by mounting evidence of Bank of Japan policy normalisation, with strong Japanese wage data, and public signals from former BOJ officials suggesting a rate hike could come as soon as this month.

The geopolitical backdrop adds a further layer of complexity, as the fragile US-Iran ceasefire and renewed disruptions near the Strait of Hormuz directly threaten Japan's energy-dependent economy, pressuring its trade balance and complicating the yen's safe-haven appeal. The interplay between declining US Treasury yields following the initial ceasefire announcement and the Fed's insistence on maintaining restrictive policy creates contradictory signals for the pair.

From a technical standpoint, USD/JPY currently trades around 158.77, sitting below the 20-day SMA at 159.24, suggesting short-term bearish positioning, while the daily RSI is near 50, reflecting decidedly neutral momentum. Over the medium term, the divergence in expected policy paths — with the Fed anticipated to cut rates while the BOJ continues to normalise — represents a meaningful structural headwind for USD/JPY, even as near-term geopolitical volatility and the pair's intact broader uptrend above the 50-day and 200-day SMAs prevent a more decisive directional move. We expect the pair to remain historically elevated in the meantime, with neutral technical pressures preventing it from accelerating higher in the medium term.

GBP / USD

Source: Massive (polygon.io)

GBP/USD is trading in a volatile environment, shaped by fragile Middle East geopolitics and divergent central bank policy signals, with the pair recently surging to a two-week high near 1.3445 on the back of the US-Iran ceasefire, only to retreat sharply as cracks in the truce emerged. The rapid deterioration of the ceasefire, highlighted by Iran's closure of the Strait of Hormuz, has reignited safe-haven dollar demand and pushed the dollar index back toward 99.10, capping sterling's upside. Elevated oil prices, still 30–40% above pre-conflict levels, continue to feed inflationary pressures on both sides of the Atlantic, complicating the policy outlook for both the Federal Reserve and the Bank of England.

From a fundamental standpoint, the Fed's hawkish, higher-for-longer stance is providing a structural floor for the dollar, while the Bank of England faces its own dilemma: stronger UK retail sales and services PMI data clash with alarming inflation signals that may force prolonged restrictive policy at the cost of growth. The flattening of the GBP 2s5s curve suggests markets are increasingly pricing in a medium-term growth headwind for the UK, even as near-term data remains resilient.

Technically, the pair is struggling beneath the 200-day and 50-day simple moving averages clustered near 1.34, which acted as clear resistance during the recent selloff from the 1.3484 high, while finding tentative support around the 1.3380–1.3390 zone tested multiple times overnight. The near-term trajectory hinges on whether buyers can defend 1.3380, opening a path toward 1.3496 resistance, or whether a breakdown triggers a deeper retracement toward the 1.3172 swing low, with the durability of the Middle East ceasefire and upcoming US inflation data serving as the key catalysts.

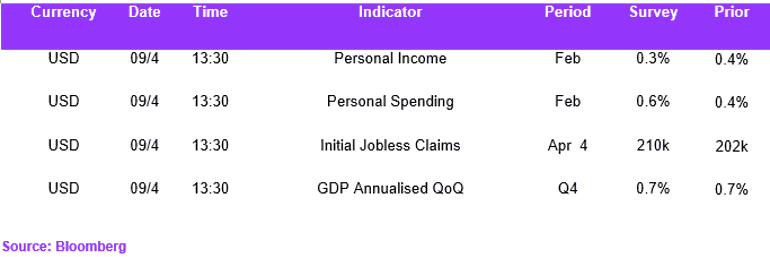

Economic Calendar