EUR / USD

Source: Massive (polygon.io)

EUR/USD’s steady climb toward 1.1723 on strong volume during the 13:00–15:00 UTC window reflects genuine buying conviction, as the US-Iran ceasefire announcement has eroded the dollar's geopolitical risk premium, providing a fundamental tailwind for the euro, though the fragile and temporary nature of the agreement means any breakdown could swiftly reverse recent gains. More structurally significant is the divergence in central bank policy expectations: markets are still pricing in potential ECB rate hikes driven by persistent services inflation and elevated wage growth, while the Federal Reserve faces mounting pressure to cut rates amid softening US economic data, including a downward revision of Q4 GDP to 0.5% and rising jobless claims.

From a technical perspective, the cluster of the 200-, 100- and 50-day moving averages near 1.1675 represents a crucial technical breach, opening the way for the pair to mark new highs. The daily RSI at 59, elevated above its recent baseline, signals building bullish momentum following the recovery from mid-March lows near 1.1415, but confirmation requires a sustained break above the 1.17 level to open the path toward the 1.1845 resistance zone.

The imminent release of US CPI data is the most consequential near-term catalyst, with any downside surprise likely to accelerate the narrowing of the rate differential and fuel a decisive move above resistance. Conversely, failure to clear the 1.17 cluster could see the pair retreat toward the 1.16 support.

USD / JPY

Source: Massive (polygon.io)

USD/JPY remains structurally supported by the wide interest rate differential between the Federal Reserve and the Bank of Japan, with the Fed maintaining a restrictive stance that continues to fuel carry trade activity and persistent yen selling pressure. However, the pair is caught between this fundamental tailwind and escalating geopolitical uncertainty stemming from a fragile Pakistan-brokered ceasefire between U.S.-Israeli forces and Iran, where accusations of violations and intermittent restrictions on Strait of Hormuz shipping have whipsawed sentiment and amplified volatility in oil markets - a critical factor given Japan's near-total dependence on imported crude. The outcome of negotiations set to begin Saturday in Islamabad, led on the U.S. side by Vice President JD Vance, will be a key near-term catalyst for directional conviction.

From a technical perspective, the pair closed precisely at its 20-day SMA of 159.23, which now serves as a pivotal level, with sellers defending the zone below the all-time high resistance at 160.41 and buyers finding support above 159.03. The daily RSI at 53 reflects diminished momentum, though the broader bullish structure remains intact with the 200-day SMA sitting far below at 154.33.

On the fundamental side, Japanese producer prices rising 2.6% year-over-year and robust bank lending growth of 4.8% suggest underlying economic momentum that could eventually support further BOJ normalisation, while the upcoming U.S. March CPI report has the potential to reshape Fed policy expectations and alter the rate differential calculus. The widely watched 160 level continues to act as a soft ceiling where Japanese intervention risk escalates meaningfully, creating a policy-influenced range that rewards dynamic positioning over a fixed directional stance.

GBP / USD

Source: Massive (polygon.io)

GBP/USD is trading in a cautiously constructive posture, having edged higher to settle near 1.3419 after breaching both the 50-day and 200-day SMAs around 1.34, which now serve as layered near-term support. The pair's recovery has been aided by oscillating risk sentiment tied to the fragile US-Iran ceasefire, which initially boosted safe-haven dollar demand before reversing course and allowing sterling to reclaim lost ground, underscoring the pound's acute sensitivity to shifts in global risk appetite.

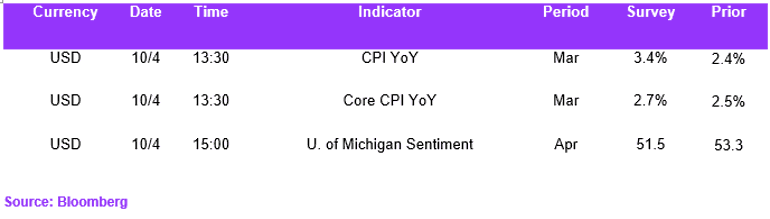

From a fundamental standpoint, the Bank of England's comparatively hawkish stance, anchored by persistent UK core inflation and elevated services sector costs, provides a modest interest rate differential tailwind for sterling, though domestic headwinds, including falling house prices, surging construction costs, and declining new orders, limit the pound's capacity to sustain purely rate-driven rallies. On the US side, the imminent March CPI report is shaping up as the dominant near-term catalyst, with economists forecasting the hottest monthly inflation print since mid-2022; a headline reading near 0.9% month-over-month could eliminate residual Fed rate-cut expectations and deliver firm dollar support, capping GBP/USD upside.

Technically, the bullish case requires consolidation above the converging moving averages and a push toward the 1.3496–1.3500 resistance zone, while a bearish rejection at this week's 1.3457 high could drag the pair back toward 1.3356 support. CFTC positioning data shows net long sterling bets have been building for several consecutive weeks but remain well below extreme levels, suggesting room for further directional moves without imminent crowded-trade reversal risk. The coming sessions will be defined by the CPI print and US-Iran diplomatic developments, with hotter inflation likely reinforcing dollar strength, while durable geopolitical de-escalation could erode the greenback's safe-haven premium to the pound's benefit.

Economic Calendar